Bev Dahlby and Ergete Ferede

Proponents focus on the average fiscal cost of program spending when the interest rate on government debt is less than the economy’s growth rate. They ignore the potentially large marginal fiscal cost of deficit-financed increases in spending that arise when a higher public debt increases interest rates on government debt and lowers growth rates.

Persistently low interest rates on government debt over past decades have prompted some leading economists to question the wisdom of fiscal policies that restrict the use of deficits to finance government spending. See Blanchard (2022), Eichengreen et al (2021), Furman and Summers (2020). This position is based on a simple model of public debt dynamics which means that when the interest rate on public debt is less than the growth rate of the economy, the ratio of the government debt to GDP can be stabilized, even if the government has a primary deficit, i.e., current revenues are less than program expenditures. Mian, Straub and Sufi (2022) argue that under these conditions, “the fiscal cost of increased debt may be zero or even negative” (Page 2) and that higher deficits are a “free lunch” in the sense that “permanent increases in deficits do not require tax increases going forward, even if they lead to permanently greater (non-explosive) debt levels.” (Page 13)

In our recent paper for the Fraser Institute, we argue that fiscal policies based on the current favourable differential between the interest rate on government debt and the growth rate of the economy can mislead policymakers into believing that debt-financed spending has low or no fiscal cost. Econometric studies indicate that higher public sector debt levels can lead to higher real interest rates and lower economic growth rates. In other words, the differential between the interest rate on government debt and the growth rate of the economy increases as the ratio of debt-to-GDP increases. This means that with a deficit-financed increase in program spending, a government must run a smaller primary deficit (or larger primary surplus) to stabilize its debt ratio. Therefore, the average fiscal cost of program spending — defined as the ratio of the taxes to program spending — will increase. As every first-year student of economics knows, when average cost increases, marginal cost is greater than average cost. In other words, the marginal fiscal cost of debt-financed spending is greater than the average fiscal cost and under certain conditions, which we describe below, the marginal fiscal cost can be greater than one. In other words, the increase in taxes needed to stabilize the debt ratio can exceed the increase in deficit-financed spending. Thus, debt-financed increased government spending can have a high fiscal cost, even if the interest rate on government debt is less than the economy’s growth rate.

Public debt, interest rates and growth rates

Blanchard et al (2021) note that there are two channels through which government deficits and debt can raise interest rates on public debt. The first is crowding out private sector investment “which raises the marginal product of capital, and by implication increases all interest rates, risky or safe, in some proportion.” (Page 9) The second “is the increase in the supply of sovereign bonds of a particular country relative to the total supply of sovereign bonds. Even in the absence of default risk, sovereign bonds from different member countries are not perfect substitutes, because of either liquidity or price-risk differences.” Econometric studies have indicate that a one-percentage-point increase in the U.S. government debt-to-GDP ratio is associated with a two-to five-basis-point increase in the real interest rate on government debt. However, because changes in U.S. deficits and debt levels can have a major impact on global financial markets, the more relevant studies from a Canadian perspective are studies of the effects of higher debt levels on interest rates in OECD countries. Studies based on panel data from OECD countries have found that a one-percentage-point increase in the debt ratio increased interest rates on government debt by between three and 10 basis points. See Ardagna, Caselli and Lane (2004), Kinoshita (2006), Grande, Masciantonio and Tiseno (2013), and Jiang et al (2022).

Since the publication of Reinhart and Rogoff’s book, This Time Is Different, many empirical studies have investigated the impact of public debt levels on economic growth rates. There are a variety of mechanisms by which higher public debt levels can reduce investment and hence economic growth. Higher public debt levels can mean higher taxes to finance higher interest payments — and that erodes incentives to save and invest. It can also result from reductions in infrastructure investment by governments. In our Fraser Institute paper, we provide an overview of econometric studies of the linkage between public debt, lower investment and economic growth rates. The most comprehensive of these studies is by Woo and Kumar (2015) which concluded that a 10-percentage-point increase in an advanced economy’s debt ratio reduces the annual economic growth rate by 0.15 percentage points.

Turner and Spinelli (2012) and recent IMF working papers by Lian, Presbitero and Wiriadinata (2020) and the European Central Bank by Checherita-Westphal and Domingues Semeano (2020), hereafter CWDS, have focused on the impact of higher government debt ratios on the differential between the interest rate and the growth rate because it is a key determinant of fiscal sustainability. The latter study contains the most comprehensive econometric analysis of the impact of public debt and other factors on the interest rate-growth rate differential, using panel data from euro area (EA) countries and other advanced OECD countries over periods from 1985 to 2017 and using a wide range of panel econometric techniques. Here we focus on their main results for 12 EA countries where they concluded that a one-percentage-point increase in the debt ratio increased the differential between the nominal interest rate on government debt and the growth rate of nominal GDP by four to six basis points. Below, we use this range of estimates to determine the marginal fiscal cost of deficit-financed spending among these EA 12 countries.

The marginal fiscal cost of deficit-financed spending

Those who argue that the fiscal cost of debt-financed spending is low focus on the average fiscal cost (AFC) which is the ratio of the taxes to program spending that is required to stabilize the debt ratio. It can be shown that the AFC = 1 + v(b/γ) where v is the difference between interest rate on government debt and the growth rate of the economy, b is the debt ratio and γ is the ratio of program spending to GDP. When the interest rate is less than the growth rate and v is negative, the debt ratio can be stabilized with a primary deficit and the AFC is less than one. In the absence of a need for fiscal expansion due to deficient demand, optimal government spending is determined by “the marginal benefits of spending, the marginal costs of taxation and of debt.” Blanchard (2022, Chapter 7, Page 4). The marginal fiscal cost (MFC) is the additional taxes that must be imposed to stabilize the debt ratio for a debt-financed increase in program spending. It is the cost of debt financing. It can be shown that MFC = 1 + v + b(dv/db) where dv/db is the rate at which the interest rate-growth differential increases as the debt ratio increases. The MFC will be higher the higher the debt ratio, the interest rate-growth rate differential and the rate of increase in the differential as the debt ratio increases. The MFC will be greater than one, and the increase in taxes needed to stabilize the debt ratio will exceed the increase in deficit financed spending, if v + b(dv/db) > 0. The MFC can be greater than one even if the growth rate exceeds the interest rate on government debt if b(dv/db) is sufficiently large, i.e., exceeds -v.[1]

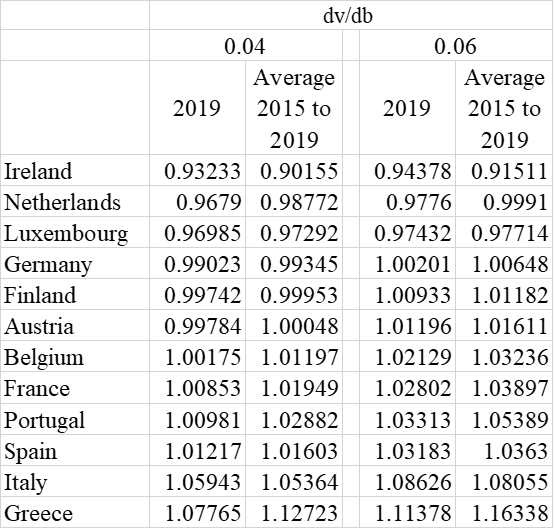

The MFCs for EA12 countries

As noted above, a large body of econometric studies indicate that growth rates decline and/or interest rates increase with an increase in the public debt. These results studies imply that dv/db is positive. Here we use the range of estimates for dv/db of 0.04 to 0.06 from the CWDS (2020) study to calculate the MFCs for the EA12 countries. The other variables used in the calculations — debt ratios and interest rate-growth rate differentials — are based on the AMECO database, which is the source of the data used in the CWDS study.

Authors’ calculations.

Table 1 shows that in 2019 the MFC was greater than one for six of the EA12 countries if the dv/db is 0.04. With dv/db of 0.06, nine countries had MFCs greater than one. Calculations of the average MFCs from 2015-19 yield very similar estimates for the MFCs.

Authors’ calculations.

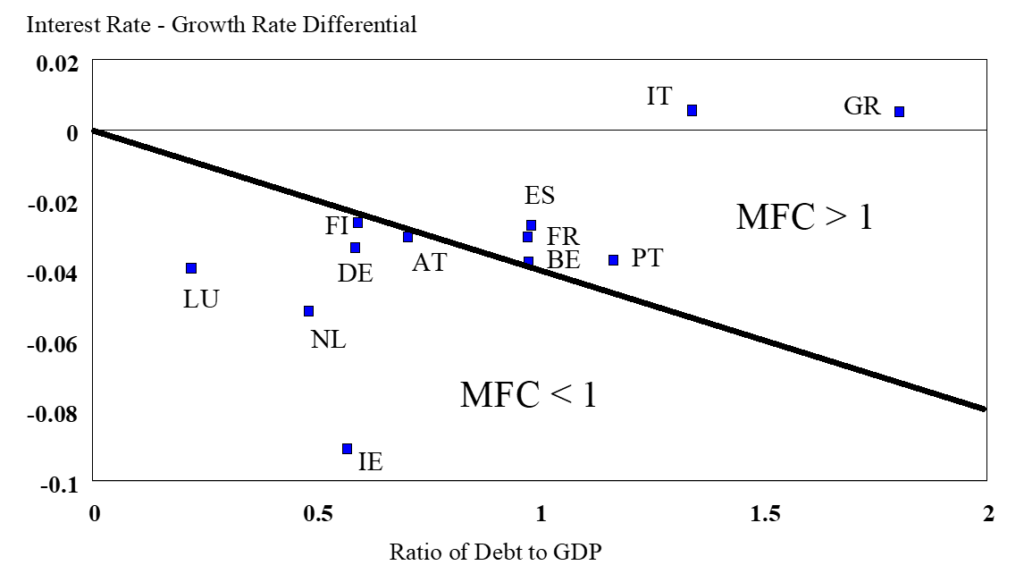

Figure 1 provides some insights into why the MFCs varies among the EA12 countries. The black line represents the combinations of the interest rate-growth rate differentials and the debt ratios such that the MFC is equal to one when dv/db is equal to 0.04. The MFC is greater than one in the region above this line and less than one in the region below the line. Consistent with the calculations in Table 1, six EA12 countries have a combination of interest rate-growth rate differentials and debt ratios that were above the MFC = 1 line in 2019. Note as well that Finland, Germany and Austria were just below the MFC = 1 line and that even small increases in their debt ratios or their interest rate-growth rate differentials would put them in a situation where their MFCs are greater than one

The MFC for Canadian governments

In the absence of other studies of the impact of public debt on interest rates and growth rates in Canada, we estimate a simple linear regression model — using annual data from 1991 to 2019 — of the interest rate-growth rate gap with the federal-provincial-territorial and local (FPTL) government debt ratios and the interest rate-growth rate differential in the U.S. as explanatory variables. The U.S. differential was included in the regression model to capture the international factors affecting the growth rate and interest rate in Canada. While the model is very simple, it captures the two key determinants of the interest rate-growth rate differential in Canada — international financial and economic conditions, and the Canadian public sector debt ratio. Both the debt ratio and the U.S. differential were statistically significant at the five-per-cent level. The coefficient estimate on the debt ratio, 0.0674, indicates that a one-percentage-point increase in the FPTL debt ratio raises the differential by 6.74 basis points, which is within the range of values in the CWDS (2020) study for the eurozone countries.

Table 2 The AFC and MFC of a debt-financed increase in program spending

| Increase in the debt ratio (percentage points) | Primary deficit (percentage of GDP) | Interest rate-growth rate differential (percentage points) | Average fiscal cost | Marginal fiscal cost |

| 1.00 | 0.976 | -1.375 | 0.974 | 1.032 |

| 2.00 | 0.944 | -1.311 | 0.974 | 1.067 |

| 3.00 | 0.910 | -1.246 | 0.975 | 1.104 |

| 4.00 | 0.874 | -1.181 | 0.976 | 1.144 |

| 5.00 | 0.837 | -1.117 | 0.977 | 1.187 |

Notes: In the initial situation, the real interest rate is 0.36 per cent, the growth rate is 1.80 per cent, the debt ratio is 70 per cent, and the primary deficit is 1.008 per cent of GDP. Program spending is 37 per cent of GDP.

In Table 2, we use this estimate of dv/db to calculate the marginal fiscal cost of a permanent debt-financed one-percentage-point increase in the program expenditure ratio by Canadian governments. The first row in the table shows that if a one-percentage-point increase in program spending results in a one-percentage-point increase in the debt ratio, a smaller primary deficit (0.976 per cent versus 1.008 per cent of GDP) is required to stabilize the debt ratio, given the 6.74-basis-point increase in the interest rate-growth rate differential. As a result, the average fiscal cost increases from 0.973 to 0.974. The marginal fiscal cost is 1.032. In other words, a tax increase that is 3.2-per-cent higher than the increase in program spending is required to stabilize the debt ratio when the debt ratio increases by one percentage point. Our ongoing research indicates that provincial governments are often slow to adjust their fiscal policies to increases in their deficits. Accordingly, the other rows in the Table 2 show the AFC and MFC of a one-percentage-point increase in program spending if the fiscal adjustment is delayed and the debt ratio increases by more than one percentage point. In particular, if the spending increase results in a five-percentage-point increase in the debt ratio, an additional $1 of program spending means that taxes have to increase by $1.187 to stabilize the debt ratio.

Conclusion

The widely held view that there is no, or only a low, fiscal cost from debt-financed increases in program spending can be very misleading. Proponents focus on the average fiscal cost of program spending when the interest rate on government debt is less than the economy’s growth rate. They ignore the potentially large marginal fiscal cost of deficit-financed increases in spending that arise when a higher public debt increases interest rates on government debt and lowers growth rates. Our calculations — based on impact of public debt on the interest rate-growth rate differentials in the euro area countries and Canada — indicate that the additional taxes required to stabilize debt ratios can exceed deficit-financed spending increases. An additional reason for exercising fiscal prudence is that international financial markets and economic conditions may quickly change and the current favourable gap between the interest rate and the growth rates could be reversed. Such a reversal would require a large fiscal adjustment to stabilize the public debt ratio at its current level.

Bev Dahlby is a senior fellow at the Fraser Institute.

Bev Dahlby is a senior fellow at the Fraser Institute.

Ergete Ferede is a senior fellow of the Fraser Institute and professor of economics at McEwan University.

Ergete Ferede is a senior fellow of the Fraser Institute and professor of economics at McEwan University.

References

Ardagna, Silvia, Francesco Caselli, and Timothy Lane (2004). “Fiscal Discipline and the Cost of Public Debt Service: Some Estimates for OECD Countries,” NBER Working Paper No. 10788 (Cambridge, Massachusetts: National Bureau of Economic Research)

Blanchard, Olivier (2022). Fiscal Policy Under Low Interest Rates. MIT Press.

Blanchard, Olivier, Álvaro Leandro, and Jeromin Zettelmeyer (2021). “Redesigning EU Fiscal Rules: From Rules to Standards” Peterson Institute for International Economics,” Working paper 21-1.

Checherita-Westphal, Cristina and João Domingues Semeano (2020). “Interest Rate-Growth Differentials On Government Debt: An Empirical Investigation For The Euro Area” Working paper No. 2486/ November, European Central Bank.

Dahlby, Bev, Ergete Ferede, and Jake Fuss. 2022. “The Fiscal Costs of Debt-Financed Government Spending” The Fraser Institute, Vancouver, B.C.

Eichengreen, Barry, Asmaa El-Ganainy, Rui Esteves, and Kris James Mitchener (2021). In Defense of Public Debt. Oxford University Press.

Furman, Jason and Lawrence Summers (2020). “A Reconsideration of Fiscal Policy in the Era of Low Interest Rates”, Discussion Draft.

Grande, Giuseppe, Sergio Masciantonio, and Andrea Tiseno (2013). “The Elasticity of Demand for Sovereign Debt. Evidence from OECD Countries (1995-2011)” unpublished research paper

Jiang, Zhengyang, Hanno Lustig, Stijn Van Nieuwerburgh, Mindy Z. Xiaolan (2022). “Bond Convenience Yields in the Eurozone Currency Union” working paper SSRN.

Kinoshita, Noriaki (2006). “Government Debt and Long-Term Interest Rates” IMF Working Paper, Fiscal Affairs Department.

Lian, Weicheng, Andrea F. Presbitero, and Ursula Wiriadinata (2020). “Public Debt and r – g at Risk.” IMF Working Paper.

Mian, Atif R., Ludwig Straub, and Amir Sufi (2022). “A Goldilocks Theory of Fiscal Deficits” National Bureau of Economic Research, Working Paper 29707,

Rogoff, Kenneth. S., & Reinhart, Carmen. (2009). This Time is Different. Princeton, NJ: Princeton University Press.

Turner, David and Francesca Spinelli (2012). “Interest-Rate-Growth Differentials and Government Debt Dynamics”, OECD Journal: Economic Studies, Vol. 2012/1.

Woo, Jaejoon and Manmohan S. Kumar (2015). “Public Debt and Growth” Economica 82 (October): 705-739.

[1] Equivalently, the MFC exceeds one if the elasticity of the interest rate-growth rate differential with respect to the debt ratio is less than -1 when the differential is negative.