Joshua Gans and Michael Smart

A vaccine tax is less coercive and more socially efficient than a vaccine mandate. We estimate that a tax of $1,500 per vaccination or booster per year is needed to effectively encourage opponents to get their shots. This amount is large enough to be salient to vaccine-hesitant, yet small compared to penalties imposed on daily smokers and heavy drinkers – where the economic case for penalties is far weaker than it is for COVID-19.

Around 88 per cent of the Canadian population above the age of 12 have received two doses of a COVID-19 vaccine. Around 35 per cent have received a third dose. On a worldwide basis, these are relatively high vaccination rates. Nonetheless, during the Omicron wave, despite the fact it causes generally milder cases, it appears that the total number of deaths will reach the number of previous waves because it is so much more infectious. (A smaller percentage of a much larger number still creates a large number of cases.) Total hospitalizations are more than double previous peaks, with the number of people in intensive care reaching the same levels seen in previous waves. In other words, the public health risk from COVID-19 has not abated.

Covid-19 is a highly infectious disease. Vaccines – with third-dose boosters – not only reduce the risk of infection to the vaccinated. They also reduce the transmission of the virus to others. In the wake of Omicron, governments worldwide are considering financial incentives to encourage vaccination – and, now most importantly, third-dose boosters. Quebec Premier François Legault’s recent musings about a “significant” financial penalty for the unvaccinated has led to predictable cries of outrage from those who consider it an infringement on liberty or who doubt its effectiveness.

The case for a vaccine tax

From an economic perspective, a vaccine tax – or another financial incentive – makes perfect sense. When individuals choose whether to be vaccinated, they presumably compare their perceived private benefits (risk-reduction from the vaccine) and their perception of its potential costs. For some fraction of the population, those private benefits are perceived to be lower than their private costs, so they remain unvaccinated.

But, in making this choice, the unvaccinated disregard the broader benefits to society that flow from their individual choice. These broader benefits are two-fold:

- First, COVID-19 is highly infectious, so vaccines that reduce infections also reduce the transmission of the virus to other susceptible individuals. (Yet, these spillover effects of vaccines create a vicious cycle of behaviour: If a high-enough portion of the population is expected to be vaccinated, then the risk of infection is low, and some of the vaccine-hesitant may choose to “free-ride” on herd immunity instead of being vaccinated themselves.[1])

- Second, in comparing private benefits and private costs of vaccination, individuals may disregard some of the costs their infection would create. This is especially clear in a publicly funded health-care system such as Canada’s, where it is likely that the unvaccinated disregard the costs of hospitalization they will incur if infected.

In other words, vaccination creates external benefits to society, which are disregarded in individual choices. An efficient solution to this problem is to impose a corrective (or “Pigouvian”) tax on the unvaccinated, inducing them to consider (or “internalize”) the costs they impose on others. In a nutshell, that is the economic case for a vaccine tax.

Unlike a vaccination mandate, a vaccine tax respects individual choices. Canadians would be free to remain unvaccinated so long as they are willing to pay the true cost, as reflected in the vaccine tax. And no one would be denied medical treatment or asked to pay for it, regardless of vaccination status, respecting the principles of the Canada Health Act.

Vaccine hesitancy may reflect historical distrust, misinformation, community pressure, free-riding incentives, or other personal reasons. While not all these reasons appear rational to most of us, it is a reasonable societal goal to mitigate such behaviour in the least coercive ways possible. A vaccine tax does this, achieving the risk-mitigation for the population at minimum social costs, allowing those with the highest perceived personal costs to remain unvaccinated. This is particularly true because – unless the efficacy of vaccines is very low – we probably do not require 100-per-cent vaccination rates to achieve herd immunity.

How high should the ‘vax tax’ be?

The foregoing tells us that the correct financial incentive for vaccination is set at the dollar value of social benefits flowing from vaccination that the individual does not internalize. While the principle is clear, it is somewhat difficult to quantify. Conceptually, the social benefit of an additional individual choosing vaccination equals the number of infections prevented in the long run from that vaccination (including secondary infections, tertiary infections, and so on) multiplied by the economic harms of an infection. In symbols,

In turn, the optimal vaccine tax rate equals that portion of the marginal social benefit that is not internalized by the person choosing vaccination, which may be less than the full marginal social benefit if the unvaccinated consider the risks to their health in making decisions.

To get a sense of the scale of the optimal vaccine tax, we simulated a stylized SIR (“Susceptible-Infected-Removed”) mathematical model of the spread of the Omicron wave. We calibrated the model to plausible parameter values describing Omicron and the average economic harms of infection. Of these parameters, economic-harm calculations are relatively straightforward:

- Symptomatic cases lose time due to illness and the mandate for self-isolation following diagnosis. Assuming five days of lost time at the average industrial wage, this cost is $1,100 per new infection.

- Administrative data show the cost of the average Covid hospital stay was $23,000 in 2021. Based on current Ontario data reflecting the early Omicron wave, there are about 14 hospital admissions for every 1,000 new infections. So, the expected hospitalization cost is $322 for each new infection.

- The Ontario data suggest a case fatality rate for Omicron of about 2.5 deaths per 1,000 infections. Using $6 million as a standard (but conservative) estimate of the value of a statistical life, the expected mortality cost of each new infection is $15,000.

Together, the estimated economic harm of an additional COVID infection during Omicron is $16,422. This is a conservative estimate because it ignores certain broader social costs of infection. A fuller calculation would include as costs the value of medical procedures postponed or cancelled (less their fiscal costs) due to pandemic capacity restrictions in hospitals, the individual costs of cases of “long COVID” and so on. Arguably, the economic harms resulting from infections also include the lost output of healthy individuals that result from lockdowns intended to control the spread of the virus. In the early stages of the pandemic, widespread lockdowns were estimated to cost nearly 25 per cent of GDP. While lockdowns in the Omicron wave have been more targeted, and the economy has largely recovered to pre-pandemic levels, such costs remain substantial.

More complex is estimating the number of infections prevented through an additional vaccination. This depends on the efficacy of vaccines in preventing infection and transmission of the virus, the dynamics of the virus itself, which are governed by both the underlying virological growth processes, and the rate of vaccination and other behavioural responses to infection risk. To estimate the number of infections prevented through vaccination, we adopt a version of the “short-run” model of disease dynamics proposed by Goodkin-Gold, Kremer, Snyder and Williams (2021), which allows us to simulate the fraction of the population infected over a single wave of the virus in a fixed population of susceptibles, up to the “steady-state” point at which the virus ultimately dies out, as herd immunity occurs through vaccination and recovery from infection. We simulate the model to calculate the proportion of the population ultimately infected and the spillover effect of a new infection on secondary and subsequent infections [2]. In symbols, the model allows us to calculate

We assume a fraction of the population is vaccinated at a single date and then simulate infections over the following year. The rate of spread of the virus in the effectively unvaccinated population depends on its basic reproductive rate R0, which measures the number of secondary infections caused in a population of maximum susceptibility – that is, when no one is vaccinated and no one has acquired immunity through infection. In the baseline simulation, we assume that R0 = 3. Over the subsequent year, the spread of the virus peaks and gradually dies out due to herd immunity effects, leaving a steady-state fraction S of the population that is unvaccinated but uninfected. In this steady-state, a slight reduction in the vaccination rate leads to new infections, each of which leads to R0 S secondary infections, which in turn lead to (R0 S)2 tertiary infections, and so on, implying external infections per case are equal to

Recent studies have suggested that three doses of existing vaccines reduce symptomatic infections during Omicron by about one-half or as much as two-thirds, but less is known about asymptomatic infections. In the baseline simulation, therefore, we assume the vaccine is effective at preventing infection and transmission in 50 per cent of cases, but investigate sensitivity to lower and higher vaccine efficacies. We then compute external infections prevented in a period of one year after individuals choose vaccination, for various hypothetical population vaccination rates.

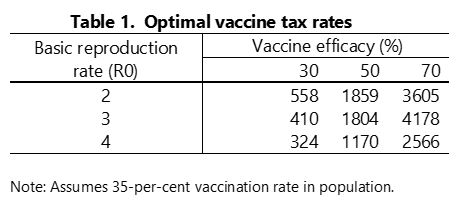

Table 1 shows the marginal external benefit of vaccination – and hence the optimal annual vaccine tax rate – for various parameter values, assuming 35 per cent of the population is vaccinated with three doses, as it is currently in Canada. In the baseline simulation, with R0 = 3 and 50-per-cent vaccine efficacy, the tax is $1,804. The tax rate varies with parameter values – but probably all the tax rates in the table would be regarded as “significant” in the sense of Premier Legault. Not surprisingly, higher vaccine efficacy implies a higher marginal benefit and a higher optimal tax rate. When the reproductive rate of the virus is larger, a smaller fraction of the unvaccinated population remains uninfected in the steady state, which reduces the external benefit of vaccinations and hence the optimal tax rate.

These calculations represent the social benefit of vaccination at current rates of vaccination. When the population vaccination rate is low, the risk of infection among the unvaccinated is high, as is the virus’s effective reproduction rate. Both factors result in a large number of external infections prevented, even when vaccine efficacy is relatively low. As the share of people who are vaccinated rises, the susceptible population grows smaller. The external benefit of vaccination may grow smaller with the vaccination rate but, because vaccines are only partially effective against Omicron, the external benefit remains relatively high, even at high vaccination rates. (Indeed, as Goodkind-Gold et al. show, the external benefit of vaccination may even rise with the vaccination rate with partial efficacy.)

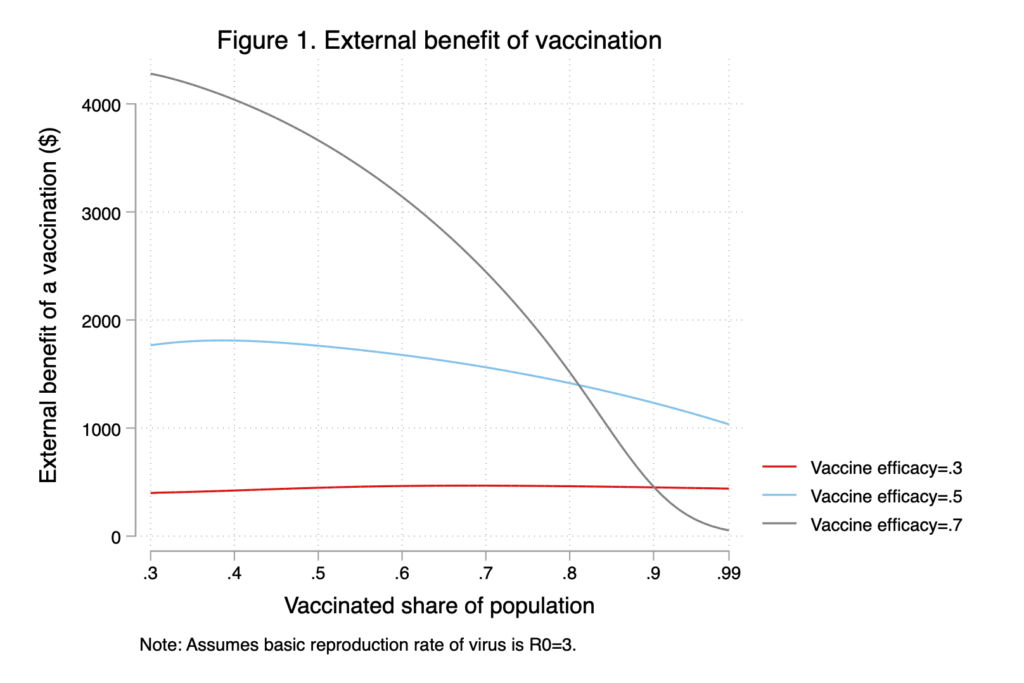

To illustrate this point, Figure 1 shows the optimal vaccine tax rate for vaccination rates between 30 and 100 per cent. At efficacy rates of 50 per cent and below, the marginal benefit of an additional vaccination is fairly constant as vaccination rates rise in the population. Given efficacy of 50 per cent and a population vaccination rate of 75 per cent, our estimated optimal vaccine tax rate is $1,493, for example, just slightly lower than the $1,803 reported for a 35-per-cent vaccination rate. Indeed, it may be that a third dose of current vaccines is more effective against Omicron and future variants than in 50 per cent of cases. As shown in Figure 1, at 70-per-cent efficacy, the marginal benefit of vaccination is large, even at vaccination rates well in excess of what we are likely to see in Canada. These findings offer some reassurance that a relatively large vaccine tax is a robustly desirable policy, now and in the future.

Fairness and effectiveness of financial incentives

In the preceding sections, we made the economic case for creating financial incentives for vaccination, and we estimate the appropriate level of such incentives to be about $1,500 per vaccination (or booster) per year. Several commentators have, however, raised broader issues and questions about the idea of a tax on the unvaccinated, which we address in this section.

Would the unvaccinated really respond to financial incentives?

Some critics have suggested that those who have chosen not to be vaccinated – despite its (to most of us) compelling risk-reduction benefits – would be unlikely to respond to an additional financial incentive. In some sense, whether or not a corrective tax actually increases pro-social behaviour is irrelevant. The “vax tax” should be set at the appropriate rate (which we estimate to be $1,500) representing the cost to society of remaining unvaccinated. Then, individuals who believe that their private costs of vaccination are higher than its social benefit should be free to pay the tax and remain unvaccinated. In this sense, a financial incentive is preferable to a vaccine mandate, which requires compliance from everyone.

Of course, this logic applies only if the unvaccinated are well-informed about the true benefits and (very small) health risks of vaccination, and if the vax tax is salient – i.e., it is known to the unvaccinated and it affects their choices. Some smart commentators have suggested that a levy payable only once per year at tax time would be less salient and less likely to affect choices than a recurring penalty (such as being refused access to liquor stores and other such public services). But an annual levy on the unvaccinated would be large and public awareness would be high. Indeed, there is some evidence that vaccination rates in Quebec have already responded to Premier Legault’s comments on the vax tax.

Aren’t vaccine mandates more effective?

As noted, we do not require full vaccination of the population to achieve herd immunity – unless vaccine efficacy is very low. Full compliance with mandates is in any case unlikely – so that a mandate still involves a choice to remain unvaccinated and pay the associated fines or penalties. In other countries, those penalties are large – much larger than the $1,500 annual tax on the unvaccinated that we are proposing. As well, there is reason to believe that vaccine mandates will be less effective in encouraging vaccine rates over the long term when community prevalence (the dominant driver of vaccine demand) is low, so that the risk of future outbreaks is mitigated (Gans, 2021).

Wouldn’t a tax be unfair and unethical?

There is evidence that vaccine hesitancy is more common among Black Canadians and among low-income populations. The Canadian Civil Liberties Association (CCLA) among other critics has suggested that a vaccine tax would be an inequitable “measure that will end up punishing and alienating those who may be most in need.” In this regard, a vaccine tax is hardly unprecedented. For example, daily cigarette smokers in Canada pay more than $3,000 in taxes annually,[3] higher than our proposed vaccine tax, despite significantly lower-than-average incomes.

As economist Jonathan Gruber has argued in the context of smoking, corrective taxes on harmful behaviours may be less regressive than they appear. If low-income individuals are induced to accept vaccination, then they will not experience any fiscal burden from the tax, and they will receive the personal health benefits of vaccination. Indeed, in a recent Angus Reid Institute poll, a higher proportion of low-income Canadians indicated that financial incentives would induce them to accept vaccination. Correcting the “internality” among those induced to accept vaccination may therefore more than offset the financial burden placed on low-income non-compliers who remain unvaccinated. While this perspective is inherently paternalistic – in that it values the personal health benefits that the unvaccinated should value but apparently do not – it may be reassuring to those concerned about equity.

Likewise, the CCLA called the proposed vaccine tax a “deeply troubling … restriction on constitutionally protected rights.” But vaccination remains voluntary under the tax regime, suggesting to us that the infringement on rights is less than under a universal vaccine mandate. Moreover, this perspective ignores the external benefits of vaccination to society which, as we have argued, seem to more than justify any implied restriction on Charter rights.

Conclusion

COVID-19 has been a devastating pandemic, now extending into its third year. As long as a significant share of the population remains unvaccinated, it continues to be an ongoing catastrophic risk to both public health and the economy. New variants and waning immunity suggest that adherence to a continued vaccination program will be essential in the years to come. A vax tax puts the costs of being unvaccinated front and centre in the minds of Canadians. It is not a long-term new tax but an intervention designed to reduce risk in our lives from the ongoing threat of COVID-19.

Our analysis of the costs of COVID-19 infections and the epidemiological benefits of vaccination suggest that each additional vaccination would create external social benefits of around $1,500 annually. An annual tax on the unvaccinated of this amount would encourage pro-social behaviour, while preserving individual rights in a way that a universal vaccine mandate would not.

[1] Oster (2018) argues that the most consistent driver of vaccine demand is the current prevalence of the disease. The difficulty is that by the time the current prevalence is high, the benefits of vaccination are mitigated in terms of preventing that prevalence (Gans, 2021).

[2] Thus, the vaccine tax is chosen to reduce the total number of infections that occur over time. In contrast, many public health interventions used so far during the COVID-19 pandemic seem designed to limit the rate of growth (or effective reproduction rate) of infections (Budish, 2020; Gans, 2021).

[3] At the current tax rate of 49.5 cents per cigarette in British Columbia, for example, a pack-a-day smoker pays $3,605 in taxes each year.

Joshua Gans is the Jeffrey S. Skoll Chair in Technical Innovation and Entrepreneurship and a professor of strategic management at the University of Toronto; vice-president (economics) of the CDL Rapid Screening Consortium: and the author of The Pandemic Information Gap: The Brutal Economics of COVID-19 and The Pandemic Information Solution: Overcoming the Brutal Economics of COVID-19 and also a regular newsletter on the pandemic. The views expressed here are his own.

Joshua Gans is the Jeffrey S. Skoll Chair in Technical Innovation and Entrepreneurship and a professor of strategic management at the University of Toronto; vice-president (economics) of the CDL Rapid Screening Consortium: and the author of The Pandemic Information Gap: The Brutal Economics of COVID-19 and The Pandemic Information Solution: Overcoming the Brutal Economics of COVID-19 and also a regular newsletter on the pandemic. The views expressed here are his own.

Michael Smart is an economics professor at the University of Toronto and co-director of Finances of the Nation.

Michael Smart is an economics professor at the University of Toronto and co-director of Finances of the Nation.