Michael Smart and Sobia Hasan Jafry

The current capital gains tax preferences cost $35 billion annually – with high-income families accruing most of the benefit. The recent passage of Bill C-208 exacerbates these issues. To fix these problems, the inclusion rate for capital gains should rise to 80 per cent from the current 50 per cent.

Capital gains are part of the taxpayer’s comprehensive income and – in a fair and efficient tax system – they should be subject to taxation just like other income. But in Canada today, only 50 per cent of realized capital gains are included in taxable income — meaning the effective personal tax rate on these gains is only half that of other income.

As previously argued here at Finances of the Nation, the current system is inequitable, because capital gains income is unequally distributed. But just how unequal? In new research to appear in the Canadian Tax Journal, we examined administrative tax data[1] and found that 82 per cent of all gains went to families in the top 10 per cent of the Canadian income distribution (those with incomes of more than $196,000), and that 57 per cent were received by families in the top one per cent (those with incomes of more than $511,000).

Commentators at the C. D. Howe and Fraser institutes have argued that a substantial fraction of capital gains go to families of limited means who declare extraordinary capital gains in a single year, driving their total incomes higher than normal. In this view, capital gains realizations should be seen as “once-in-a-lifetime” events that make families appear artificially wealthy in the data.

It is true that most taxpayers outside the top one per cent of incomes declare capital gains income infrequently, so that annual measures of income and gains can be deceptive. On the other hand, taxpayers may take gains in years when other income is abnormally low – for example, after they retire or are otherwise separated from their jobs. (Indeed, 22.5 per cent of all net gains in recent years were declared in the year of the death of a taxpayer in the family – an event that is likely to reduce other income of the family.)

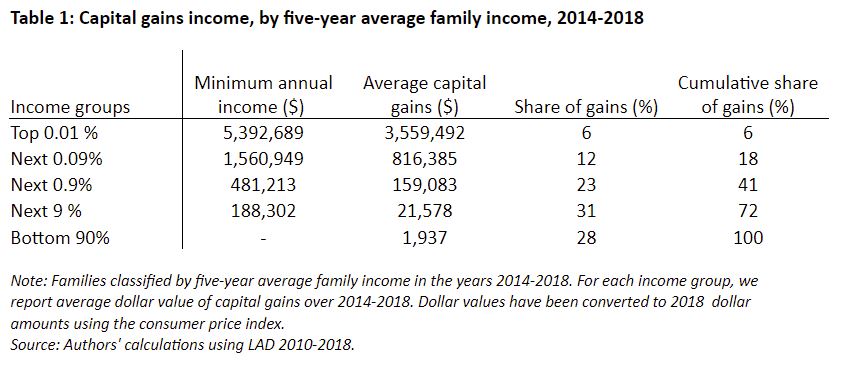

To understand the distribution of capital gains, it is therefore better to take a long-term perspective. We computed families’ average annual capital gains income over the 2014-18 period, and tabulated it by average family income in the preceding five years. Averaging over five years gives a more accurate measure of families’ permanent income and ultimately their wealth.

The results of these calculations are reported in Table 1. By this measure, capital gains income is somewhat less unequally distributed than on an annual basis – but it remains highly unequal. We find that 72 per cent of gains went to families in the top 10 per cent of the long-run income distribution, and 41 per cent to those in the top one per cent.

The top 0.01 per cent of represents the richest 420 families in Canada. In this group, families declared $3.6 million in capital gains on average each year in the 2014-18 period, or six per cent of the total – and at least $17.7 million in capital gains over their lifetimes. The tax savings that flow to these families from the fact that only 50 per cent of this is included in taxable income are therefore substantial.

These calculations should also put to rest the notion that capital gains income is received in any significant measure by the middle class, or that the tax preference given to capital gains have any egalitarian component.

Capital gains and surplus stripping

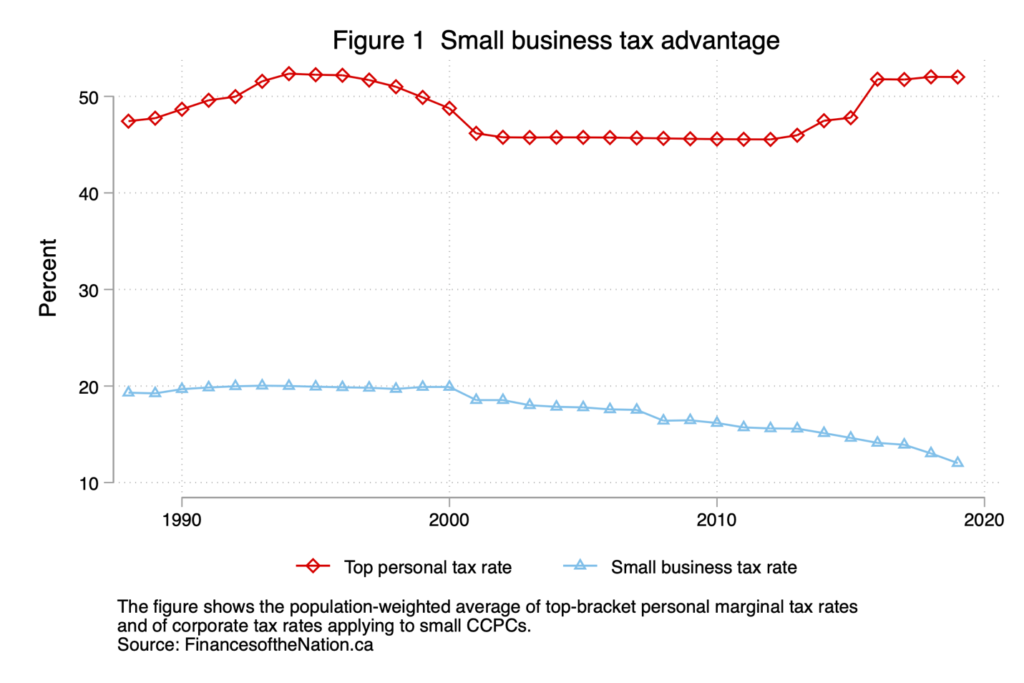

Canada imposes very low corporate tax rates on small businesses. On average across the provinces, the combined corporate tax rate for small Canadian-controlled private corporations (CCPCs) is now 12 per cent, compared to an average top personal tax rate of 52 per cent. As shown in Figure 1, the gap between corporate and personal rates has widened in recent years.

The low rate is intended to reduce the tax burden on small business investment and thereby facilitate growth. But there is a great potential for small businesses – particularly those owned by high-income professionals — simply to become tax shelters in which business owners shield income from high personal tax rates.

To make the system work as intended, corporate-personal tax integration must be designed carefully to ensure that that income earned in CCPCs is fully taxed – at business owners’ full personal tax rate – when corporate earnings are ultimately paid out to shareholders in the form of dividends or capital gains. While the system works well for dividends, it does not for capital gains. The effective tax rate on gains has fallen over time, beginning with the 2000 reform that reduced the capital gains inclusion rate to 50 per cent from 75 per cent, and continuing over time, as corporate tax rate reductions have made gains even more tax-advantaged. In Ontario for example, the effective tax rate for capital gains is now 12.6 percentage points below that on ordinary income for top-bracket investors in the province.

As a result, small business owners now have strong incentives to find ways to extract corporate profits as capital gains rather than dividends or wages, to get the benefit of lower taxes on gains. These “surplus stripping” transactions are financially sophisticated, but in one canonical example they involve a holding company established by the business owner that issues a promissory note to purchase shares of an operating company that has retained earnings, resulting in a taxable capital gain. Capitalization of the holding company may then be achieved by a tax-free intercorporate dividend or other such means, with the proceeds then used to discharge the promissory note held by the business owner, resulting in a cash distribution to the owner.

Surplus stripping by small business owners appears to have been comparatively rare in past years. Examining personal tax records for the 2016-18 period, we identified just 2,850 transactions in the average year that have the hallmarks of surplus stripping,[2] on which the average released capital gain was $64,300, and the total tax saved from the transactions (relative to dividend payouts) was just $36.6 million annually. While the revenue losses from surplus stripping from CCPCs have been small, they nevertheless raise issues of equity and efficiency in the tax system.

Surplus stripping since Bill C-208

However, Bill C-208, a private member’s bill recently enacted by Parliament, has made surplus stripping easier than ever before. Notwithstanding Section 84.1 of the Income Tax Act, Bill C-208 explicitly allows incorporated small business owners to claim proceeds from the sale of shares to an adult child or grandchild as capital gains, rather than as dividend payments.

The result is that capital gains generated from such transactions are now eligible for the lifetime capital gains exemption. While C-208 was ostensibly designed to allow tax-free transfers of active businesses across generations of a family, there is no mechanism in the act to exclude purely paper transactions that pay out accumulated surplus, even if there is no real transfer of control of the business to the owner’s descendants.

This has the potential to open a floodgate of surplus stripping transactions, with concomitantly larger revenue losses to federal and provincial governments. The Department of Finance announced in July its intention to limit tax avoidance under Bill C-208 but, at the time of writing, still had not introduced legislation to do so.

Until the new legislation is enacted, the government has left the C-208 loophole wide open for businesses to exploit. The government has also made it clear that it any future attempt to close the loophole in C-208 will still nevertheless allow for permanently lower taxes on intergenerational transfers of businesses.

The Office of the Parliamentary Budget Officer previously evaluated a similar proposal (Bill C-274, defeated on second reading in 2017) that would also have made business transfers between family members eligible for the capital gains exemption, and estimated a revenue loss of $279 million for 2018. Revenue loss estimates for Bill C-208 have not been released.

Capital gains and inflation

Another common argument in favour of reduced tax rates on capital gains is that, in an inflationary environment, some portion of realized capital gains represents compensation for inflation, which should be excluded from the tax base.

In our view, this does not mean that capital gains income should be taxed less than ordinary income. Instead, the taxation of nominal gains should be regarded as a rough-and-ready corrective device to address the deferral advantage that investors receive in our realization-based tax system.

In a comprehensive income tax system, investors would be taxed on accrued gains on an annual basis. The current failure to do so affords investors the opportunity to accumulate assets that generate capital gains at the pre-tax rate of return.

In contrast, other assets that pay interest or dividends are taxed annually and accumulate at the after-tax rate of return. This non-neutrality in the tax system favours assets generating capital gains, which is both inequitable and inefficient.

To reduce tax rates on capital gains because of inflation would simply be to perpetuate the inequitable and inefficient deferral advantage from realization-based taxation.

The change our system needs

Reduced tax rates on capital gains are inequitable, and they encourage tax-sheltering activity that serves no productive purpose. This is especially clear when considering the small business tax planning opportunities presented by Bill C-208.

So, capital gains tax rates should increase, but by how much? One possible solution is to focus on the failures in corporate-personal tax integration and choose inclusion rates that equalize the effective tax rates on dividends and capital gains. This would achieve neutrality for different forms of corporate distributions, and eliminate the incentives for the kinds of tax-motivated share repurchases and surplus stripping described above.

While the distribution-neutral inclusion rate differs for large corporate shares and small CCPCs, a separate inclusion rate for qualified small business shares would create complexity and could create new avoidance opportunities. A better approach, then, is to raise the inclusion rate to 80 per cent for all gains on shares, which would achieve approximate neutrality for both large and small corporations.

The focus on neutrality for dividends and capital gains raises the issue of how to treat other non-corporate assets, such as personal use property including works of art and vacation homes. Here again, the arguments for higher inclusion are strong. The return on holding such assets is not generally subject to corporate incomes taxes, so that reduced tax rates are not required in these cases to achieve corporate-personal tax integration. There is a strong case for taxing them fully.

Raising the inclusion rate would increase income tax revenue substantially. If the inclusion rate were 80 per cent, we estimate that federal and provincial personal income tax revenue would have been $9.4 billion higher in 2017. To eliminate tax avoidance opportunities, the inclusion rate should also rise to 80 per cent for capital gains realized by corporations, which would raise the revenue impact to an estimated $19.0 billion annually – or 5.7 per cent of all federal and provincial income tax revenues.

A capital gains tax increase would be a form of annual “wealth tax” that would be very simple to implement within our current system, would cost no more to collect (and probably less), while reducing the economic costs of tax avoidance behaviour. The Parliamentary Budget Officer recently evaluated one proposal for such a tax, a one per cent tax on individual wealth portfolios in excess of $20 million, estimating that it would raise far less revenue than our proposal. A wealth tax would have significant administrative costs and enforcement problems, and arguably it would exacerbate inter-asset tax distortions, harming productivity.

In contrast, the case for an increase in capital gains taxation seems clear.

[1] The data are drawn from the longitudinal administrative databank (LAD), a 20 per cent sample of all personal tax returns provided by Statistics Canada.

[2] These are all transactions by CCPC owners generating a capital gain of at least $10,000, for which the lifetime capital gain exemption was not claimed, despite the taxpayer having room to do so. For further details, see our article in Canadian Tax Journal.

Michael Smart is an economics professor at the University of Toronto and co-director of Finances of the Nation.

Michael Smart is an economics professor at the University of Toronto and co-director of Finances of the Nation.

Sobia Hasan Jafry is a PhD student in the department of economics at the University of Toronto.

Sobia Hasan Jafry is a PhD student in the department of economics at the University of Toronto.