Robin Boadway and Katherine Cuff

Our proposal represents an incremental step in the direction of a basic income guarantee. Harmonizing the main income tax credits, making the base and tax-back rate suitably progressive, and ensuring they are all refundable would form the basis for a modest basic income.

The Canadian income tax system is complex, but some of these complexities are avoidable. A case in point is the system of personal income tax credits. This consists of an array of refundable tax credits (RTCs), non-refundable tax credits (NRTCs) and income-tested transfers that rely on the income tax system and are delivered mostly by the Canada Revenue Agency (CRA). This approach evolved over many years in piecemeal fashion and has resulted in a system that contains inconsistencies and redundancies, and that compromises its fairness and efficiency.

The last major reform of the tax credit system occurred 40 years ago when tax credits replaced most tax deductions to make the system more equitable. Since then, the number and variety of tax credits has grown with little attempt at rationalization. In 2016, Finance Canada undertook a review of all income, sales and excise tax expenditures, including RTCs and NRTCs, with a view to streamlining the system. Few concrete measures came out of that review. Reforming the entire swath of tax expenditures is a major task and one that is fraught with difficulties. Focusing reform on tax credits alone is more manageable and arguably less controversial. Our intent is to propose a path to reform of RTCs and NRTCs to make them more coherent. The reform would entail retaining most tax credits but harmonizing them to make the system fairer and more efficient, as well as less complex and more transparent.

Our proposal would apply to tax credits aimed at enhancing the equity of the tax system and not to those intended to influence individual behaviour. For the former to be harmonized, a three-step procedure would apply. First, for each tax credit, a base amount would be defined that could be conditioned on family size, age, employment, disability or other characteristics that are already reported to the CRA. These base amounts would then be aggregated for each taxpayer. In the second step, the actual amount of the credit to which a given taxpayer is entitled would be calculated by applying a benefit-reduction — or tax-back — rate to a measure of the individual’s income. The tax-back rate would apply only once to the aggregate of all tax credits, and the rate itself could be contingent on income. We propose that this tax-back should depend on family net (i.e., taxable) income, though others may argue in favour of individual net income. Unlike the present system, the same tax-back rate would apply to all tax credits. In the third step, aggregate tax credits would be set against the individual’s tax liabilities and would be fully refundable if tax credits exceed tax liabilities. Any tax credits not included in our scheme would continue to apply.

This system of harmonized tax credits should be distinguished from a universal tax credit approach where individual tax credits are replaced with a single RTC. The U.K. universal credit is an example of such an approach, although in a context involving welfare and unemployment benefits as opposed to NRTCs and RTCs. In the Canadian setting, Simpson and Stevens (2015) have explored making NRTCs refundable but without harmonizing tax-back rates to avoid some of the problems we discuss below. Stevens and Simpson (2017) and Boadway, Cuff and Koebel (2018) have explored transforming most NRTCs and RTCs, as well as provincial social assistance, into a single refundable tax credit that serves as a basic income. Our proposal for harmonizing most federal income tax credits and making them income-tested and refundable can be viewed as a modest first step toward implementing a basic income guarantee.

Some common features of tax credit administration

The system of NRTCs, RTCs and income-tested transfers like OAS and GIS have some administrative characteristics in common. The credit amount is based on information reported by the taxpayer to the CRA, and thus is contingent on the individual filing income tax returns. Eligibility for tax credits is based on self-assessment that can be verified only by audit ex-post, referred to as trust-and-verify by Robson (2020). Benefit reduction or tax-back also depends on different income measures reported to the CRA. Unlike employment insurance (EI), they do not rely on employment data, changes in employment status or changes in income within the tax year. Thus, the critiques of Robson and the BC Expert Panel on Basic Income (2020) about the limitations of the CRA in administering transfers do not apply.

Another important feature of RTCs, which may be regarded as a serious limitation, is that the amount of tax credit for which a taxpayer is eligible is based on the previous year’s tax data. There is no attempt to update the size of the credit during the tax year. An exception is the Canada child benefit (CCB) for which eligibility can be updated for childbirth, but the amount for which the parent is eligible still depends on the previous year’s tax data. While this restricts the ability of tax credits to respond to changes in circumstances, it also achieves administrative efficiency. For example, in the case of RTCs, it avoids the need to estimate incomes at the same time as the credit is being paid out, and therefore avoids the need to recover any overpayments. Note that determining the size of the tax credit based on the previous year’s tax information does not preclude making payments quarterly or monthly.

The system is also flexible enough to allow most provinces to implement their own individual supplements to federal tax credits. This is facilitated by the bilateral federal-provincial personal income tax agreements that all provinces except Quebec have signed, which allow provincial income tax systems to be administered by the CRA. All the problems of fairness and efficiency discussed below also apply to provincial RTCs and NRTCs. Ideally, our proposal would be taken up by both levels of government.

Recently, the CRA was called upon to administer temporary measures meant to respond to the COVID-19 pandemic, (Robson, 2020). These differ in important ways from existing refundable and non-refundable tax credits. Eligibility is based on changes in income and employment, and they are taxed back ex-post so some recovery of overpayment may be required. While these programs were timely and met a short-term need, making them permanent would raise the implementation problems stressed by Robson. They would also challenge the administrative capacity of the CRA.

Problems with existing tax credits

There are several problems with the existing system of tax credits. It is complex and consists of many different credits. A small number are refundable, such as the GST credit and the Canada workers benefit (CWB), while the others are not. Tax-back rates and benefit structures differ, and the bases used to calculate them do as well. Some credits are conditioned on individual net income and others on family net income. Family size is usually not considered, with the exception of spousal and dependant credits and the CCB. Some credits — so-called boutique credits — target quite narrow characteristics or activities, while others, such as the basic personal amount, are universal.

Main Refundable and Non-Refundable Federal Tax Credits

|

Cost |

Eligibility |

Tax-Back Rate |

|

|

Refundable credits |

|

||

|

Canada child benefit |

$27.3 B |

Families with children under 18 years of age. |

7-23 per cent of adjusted family net income between $31,711 and $68,708; and 3.2-9.5 per cent of adjusted family net income greater than $68,708. |

|

Canada worker benefit |

$1.6 B |

Individuals with employment income not attending school full time. |

12 per cent of adjusted family net income above threshold. |

|

GST credit |

$10.5 B |

5 per cent of adjusted family net income over $40,500. |

|

|

Non-refundable credits |

|

|

|

|

Age amount |

$3.9 B |

Taxpayers aged 65 and over. |

15 per cent of net income in excess of $38,500. |

|

Basic personal amount |

$43.3 B |

All taxpayers |

Gradually reduced for taxable incomes above $150,478. |

|

Spousal or common law partner amount |

$1.8 B |

Taxpayers with spouses |

Reduced dollar-for-dollar by net income of spouse. |

|

Amount for an eligible dependent |

$1.2 B |

Taxpayers living with an eligible dependent relative. |

Reduced dollar-for-dollar by net income of dependent. |

|

Canada employment amount |

$2.7 B |

Taxpayers with employment income. |

Not taxed back |

|

Disability tax credit |

$1.3 B |

Taxpayers certified by a qualified medical practitioner as having a severe and prolonged disability. |

Not taxed back |

|

Pension income amount |

$1.3 B |

Taxpayers receiving eligible pension income. |

Not taxed back |

|

* Costs are the projected 2020 calendar year projections of tax expenditure. Source: Department of Finance Canada. (2021). Report on Federal Tax Expenditures – Concepts, Estimates and Evaluations 2021. |

|||

The table (above) shows the total cost of the credit in 2020, the eligibility criteria and the tax-back mechanism that applies for the main federal refundable and non-refundable tax credits.

Some complexity is understandable, given the diversity of objectives of individual credits, but some is unnecessary, given various redundancies among credits. For example, the employment amount and the CWB both target employed workers. The age amount and the pension income amount seem unnecessary given OAS/GIS transfers, as well as pension income-splitting. Some of the smaller credits have complex compliance requirements relative to the populations or behaviours being targeted, and the effectiveness of some credits is questionable (e.g., transit credit, first-time homebuyers credit).

The existing system also compromises fairness or equity in various ways. Some tax credits that serve equity purposes are not refundable, which precludes benefits from being realized by the lowest income groups. The most obvious is the basic personal amount which as an NRTC is of value only to those with positive tax liabilities. No doubt this is because of the piecemeal manner in which these credits evolved. The basic personal amount was a deduction before 1981, then was converted to a credit to improve its fairness. That was before the advent of RTCs, beginning with the GST credit in 1991, and is a good example of path dependency of tax reform. The non-refundability of tax credits effectively creates a first tax bracket with a zero marginal tax rate. This is contrary to standard optimal income-tax analysis, which typically calls for relatively high marginal tax rates at lower incomes with refundability to provide fair incomes for those earning the least. Refundability also leads to participation subsides at the bottom, thus encouraging labour supply. In addition to the anomaly of non-refundability, tax-back rates differ among tax credits and are typically low enough so that credits are obtained by persons with above-average incomes. The basic personal amount is an extreme example of this. It has a zero benefit-reduction rate for all except the highest income groups, and a low reduction rate even for the latter.

The various credits also treat family circumstances very differently. Two approaches can be distinguished. First, the amount of some credits depends on family size. Examples include the CCB, the spousal credit and the dependent credit. Second, benefit reduction for some tax credits is conditional on family income. This is the case for the CCB and the GST credit, among others. In fact, it is mainly through the treatment of tax credits and deductions that family circumstances are considered in the tax system. Otherwise, the tax system is based on individual, rather than family, income and the individual is the taxpaying unit.

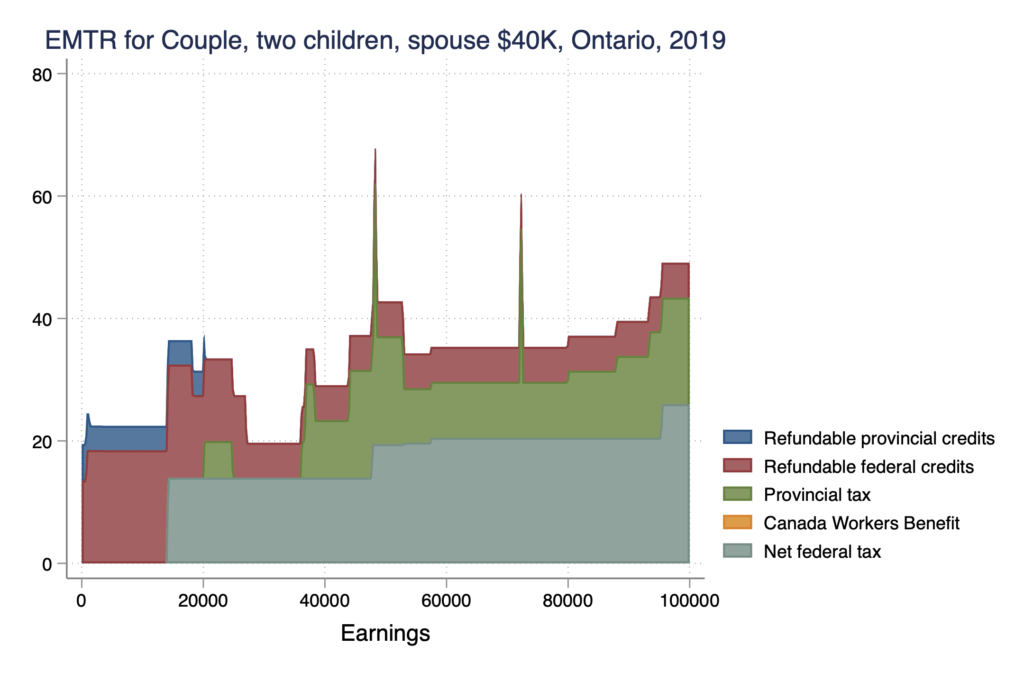

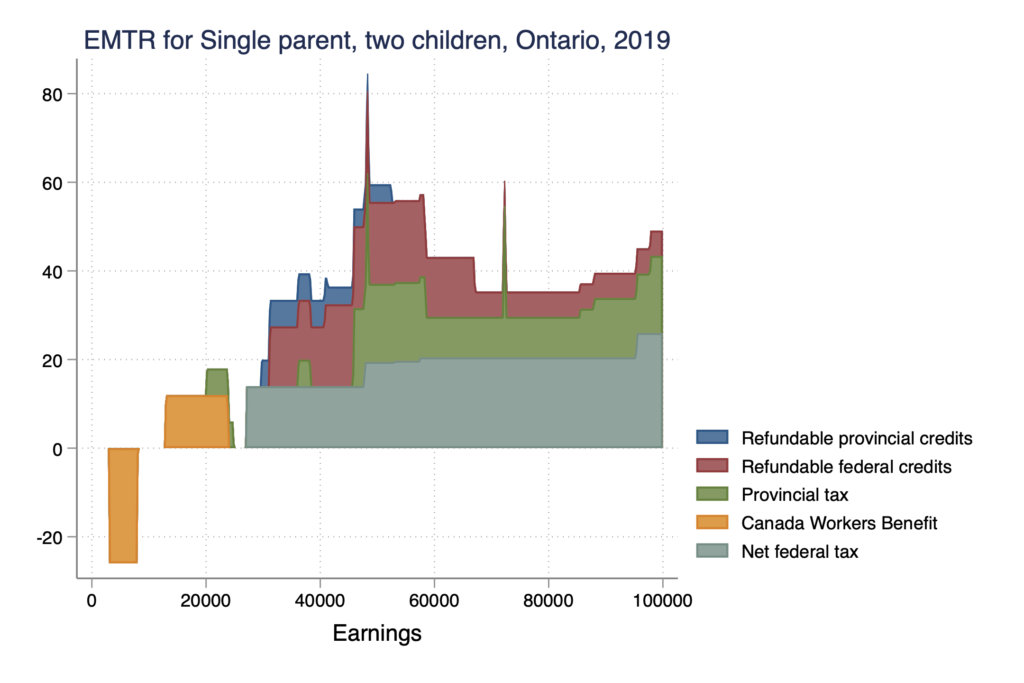

A final problem with the tax credit system, and one that affects economic efficiency, concerns the cascading of tax-back rates. Under the current system, each tax credit faces its own tax-back calculation. If a taxpayer is eligible for two tax credits and the amount of each credit is reduced with taxable income, each additional dollar of income effectively faces three tax rates: the standard income tax rate and the two tax-back rates. The effective marginal tax rate (EMTR) is the sum of the three effective tax rates. The pattern of EMTRs facing a given taxpayer depends on the number of tax credits for which they are eligible and the tax-back rate associated with each. Since tax credits are phased out as income rises, EMTRs can be particularly high at low income levels. The following graphs depict patterns of EMTRs resulting from federal and provincial refundable tax credits on top of prescribed federal and provincial income tax rates in 2019. Two representative cases from Ontario are shown — couples with two children where the taxpayer’s spouse earns $40,000 and single parents with two children.

The graphs illustrate both the extent of cascading and how the consequences of cascading for EMTRs are especially pronounced at lower income levels. The largest spikes are the result of the Ontario health premium tax.

The cascading of marginal tax rates adds complexity and compromises fairness in the tax system because the tax-back rate applicable to increases in income depends on the number of credits. It also compromises economic efficiency. High EMTRs can adversely affect labour supply decisions in two different ways. For one, they discourage individuals from earning more income to the extent that they have discretion over the amount they work. For another, they can discourage individuals from taking a job. This can be particularly important for secondary earners whose partners earn higher incomes. The latter incentive effect is captured by participation tax rates which measure the net increase in tax liabilities (taxes incurred less transfers foregone) due to taking a job paying a standard income.

The fact that some tax credits are taxed back depending on family income raises a further complication. An increase in the income of one family member reduces not only the tax credits of that member, but also the tax credits of other family members, thus giving rise to a form of multiple taxation. In the case of a two-adult family, an increase in earnings by one family member increases family income, which is taxed back from the credits of both adults. The result is a tax-back rate of two times the stated tax-back rate. To the extent that a family member values credits going to other family members, this may be viewed as being unfair as well as potentially inefficient to the extent that the incentive to earn income is influenced by the total effective tax rate on incremental income increases.

The proposal we present below is designed to simplify the system of tax credits, enhance its fairness and eliminate cascading of marginal income tax rates.

Harmonized tax credits

Our proposal would be to harmonize those RTCs and NRTCs that serve equity purposes, and to eliminate those that are redundant or ineffectual. Currently, each credit i consists of a basic amount bi and a tax-back rate ti based on some income measure. bi can be based on age, employment status, family size and family income, while ti can be nonlinear, differs by credit, is based on some measure of individual or family net income and can be adjusted for various factors. Entitlements are calculated independently for each tax credit, and refundability may or may not apply.

Under our proposal, the bases of all credits would be aggregated to get a cumulative tax credit base, b=∑bi Each bi could be based on separate factors as in the current system, but other factors could be included. For example, an equivalence scale such as the square root rule used by the OECD could address family size. That is, if bi is the credit base for an individual, a family with n adults would be entitled to √n times bi. A single tax-back rate t, which could be piecewise linear, would be based on some taxable income measure y and would apply only once to the cumulative tax credit b. If t were linear, an individual’s tax credit would be c = b – ty for c ≥ 0, and zero otherwise, and c would be refundable. The costs of refundability could be mitigated by adopting a higher tax-back rate than now applies to most NRTCs and RTCs. Such a system would avoid the cascading of tax-back rates but would do so at the cost of choosing a common tax-back rate to be applied to a common net income measure..

A number of issues would have to be addressed in establishing the details of the harmonized tax credits, including the following:

Seniors: In principle, OAS/GIS at current rates could be included in a harmonized credit system and subject to the common tax-back rate. That would be problematic because the OAS/GIS tax-back rate is very low, so middle-income seniors would be serious losers under harmonization.

Children: A similar problem would apply here. The CCB could be harmonized but would be subject to the harmonized tax-back rate. Since the current tax-back rate for the CCB is relatively low, some middle-income families would be worse off. Though this may foster equity, it might also invite opposition. A second-best option would be to exclude seniors and children from harmonized scheme, and retain CCB and OAS/GIS.

Tax-back rates: Some current tax-back provisions are designed to achieve specific purposes. The CWB is a case in point because it incorporates a participation subsidy (negative tax-back rate) at low income levels. One could build a participation subsidy into the common tax-back rate to apply to the cumulative base b, although that would increase the cost. Eligibility for the CWB requires that working (employment and self-employed) income be at least $3,000. However, the tax-back is based on net family income. so would be compatible with our harmonized scheme.

Family vs individual net income: The income tax system bases tax rates on individual income, which might suggest using individual net income for taxing back credits for consistency. However, a case can be made on equity grounds for basing tax-back of credits on family net income because at least some credits target families. As well, many low-income individuals come from families with a high-income adult member. Designing tax credits using family characteristics involves two dimensions. First, as mentioned, the basic credit could be conditioned on family size using a family equivalence scale such as the square-root rule. Second, tax-back should be based on family income in a way that avoids double tax-back problems.[1] If the tax-back is based simply on family income, a $1,000 increase in income by one member of a two-person family reduces the tax credit for both family members by t x $1,000, so the family tax-back rate is 2t. This would be a disincentive to work if the family member cared about the income of other members, and it would arguably be unfair. To avoid this, family income could be aggregated for the purpose of tax-back, and equal shares assigned to each family member. Then, if a family member earns $1,000 more, $500 of that is attributed to each family member, and the amount each is taxed back is t x $500. The total tax-back of both is t x $1,000, and the marginal tax-back rate is t.

Our proposal is aimed first at the federal government. Ideally, however, provincial tax credits should be harmonized with those of the federal government. This should not be an insurmountable problem, but it would involve federal-provincial negotiations to revise the tax collection agreements.

As mentioned above, our proposal represents an incremental step in the direction of a basic income guarantee. Harmonizing the main income tax credits, making the base and tax-back rate suitably progressive, and ensuring they are all refundable would form the basis for a modest basic income.

[1] Boessenkool and Davies (1998) also recommended basing tax credits used for social purposes on family income and adopting family equivalence scales to adjust for family size. They suggested that basing taxation on the family rather than the individual would also be fair, but it would be politically difficult to implement.