This commentary examines the economic effects of the taxation of dividends and capital gains collected via the personal income tax, applied to the supply side of the capital market. I show that taxable dividends and capital gains are highly concentrated at the top of the income distribution, much more so than is labour income. I also argue that, while the evidence is somewhat inconclusive, aggregate savings is relatively insensitive to changes in after-tax returns. This is the first commentary in a three-part series considering reforms to Canada’s approach to taxing capital income.

The twin pillars of public finance that economists employ to evaluate tax policy are the notions of efficiency and equity. Efficiency involves the distortionary impact of taxes on behaviour, which generates real costs by reducing economic activity and eliminating potential gains from trade. Equity concerns the distribution of the burden of taxes among various groups, typically (but not exclusively) on the basis of income or wealth.

It is usually understood that to pursue a more equitable distribution of (say) income one must incur efficiency costs. In other words, there is a trade-off between the goals of equity and efficiency. Indeed, the essence, and the art, of policy making is often framed (in the eyes of economists at any rate) in terms of this equity-efficiency trade-off.

In a series of three commentaries I examine the equity-efficiency trade-off in the context of the taxation of capital income. I argue that we can undertake reforms to the taxation of capital income in Canada that are attractive in terms of this equity-efficiency trade-off.[1]

In this first commentary I discuss the taxation of capital income at the personal level, under the personal income tax (PIT). This is the supply side of the capital market, as it is ultimately personal taxpayers who supply the funds for capital investment to firms through their savings, and receive dividends and capital gains in return. In a subsequent commentary I consider the corporate income tax (CIT), which is applied to the demand side of the capital market, on the profits earned by the firms which employ the funds to undertake capital investments. In the third commentary, I bring the two sides of the market together and discuss reforms to the capital tax system in Canada that I think are attractive in terms of the equity-efficiency trade-off.

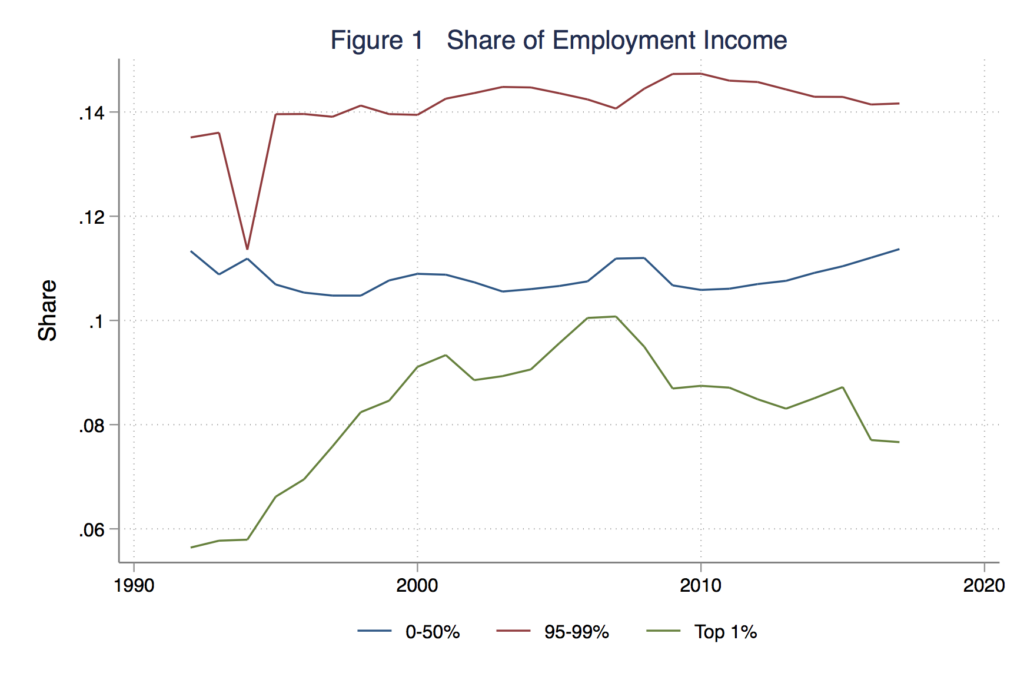

To begin I look at the distribution of personal income from labour and capital in Canada, using the FoN Personal Income Statistics database. Figure 1 shows the share of income from employment earned by three groups. As is widely known, labour income is skewed quite significantly toward the top of the income distribution.

For 2017 we see that:

- The top 1% of the employment income distribution earned 7.7% of employment income.

- The next 5% (95-99th) earned 14.2% of employment income.

- The bottom 50% of the distribution earned just 11.4% of employment income.

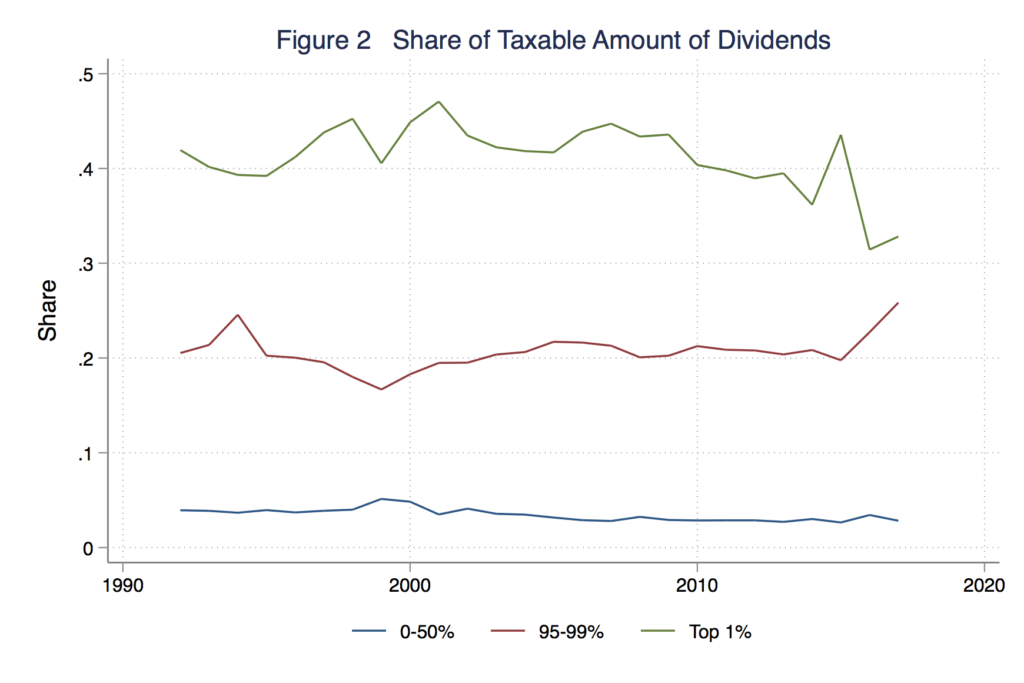

However, the distribution of capital income is skewed toward the top even more. Figure 2 shows the distribution of the taxable amount of dividends in Canada.

For 2017 we see that:

- The top 1% earned 32.8% of taxable dividends.

- The next 5% earned 25.8% of taxable dividends.

- The bottom 50% earned just 2.8% of taxable dividends.

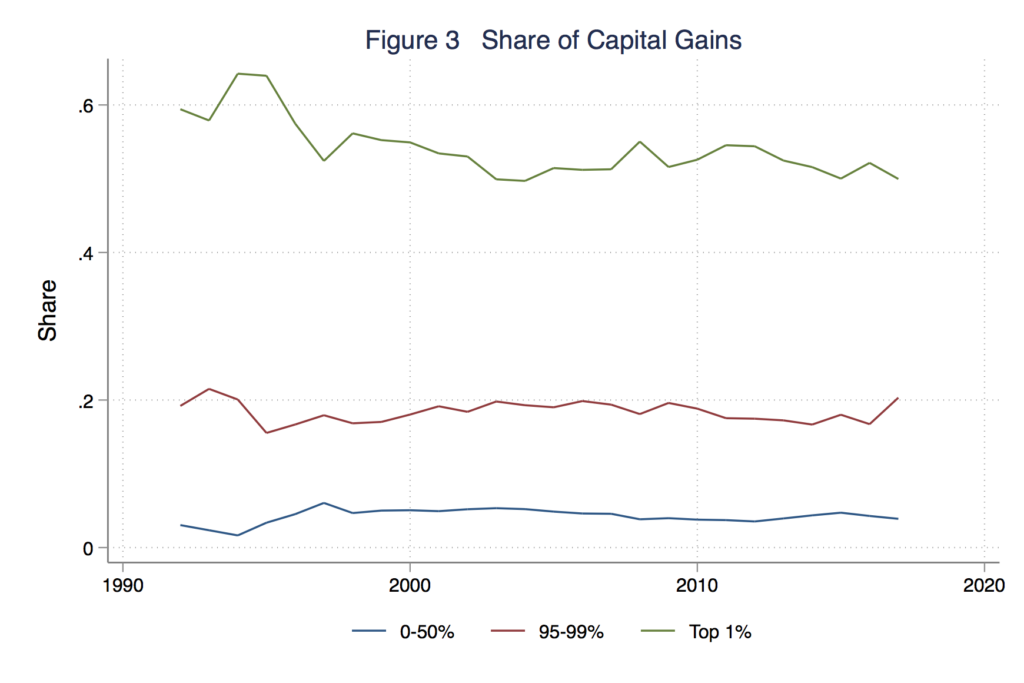

Figure 3 shows the shares for taxable capital gains, which is skewed even more to the top.

For 2017 we see that:

- The top 1% earned 50% of taxable capital gains.

- The next 5% earned 20.3%.

- The bottom 50% earned just 3.9%.

So we see that the distribution of taxable capital income in the form dividends and capital gains at the personal level is significantly more skewed to the top of the distribution than is employment income.[2]

It is important to stress that the income from dividends and capital gains referred to above is taxable income as reported in tax returns. This is not the same as total capital income.

The distribution of taxable capital income is skewed to the top for two reasons. The first, of course, is that higher income earners simply save and invest more than lower income earners, and therefore earn more dividends and capital gains income. The second is that for many taxpayers’ capital income is simply not taxed at all, in large part because of tax shelters like Registered Retirement Savings Plans (RRSP) and Tax Free Savings Accounts (TFSA), which effectively exempt capital income from taxation (albeit in different ways). The vast bulk of Canadians are not at the limit of their RRSP and TFSA contributions, and therefore do not report taxable dividends and capital gains at all.[3] Thus, for the most part, taxes on income from dividends and capital gains are paid by higher income taxpayers who have exhausted their RRSP or TFSA room.

A key metric to determine the distortionary and efficiency implications of taxes on savings is the sensitivity of savings to changes in the after-tax rate of return. The more sensitive are savings the more distortionary is the tax, and the higher are the efficiency costs associated with taxing savings. This sensitivity is measured by estimating the elasticity of savings, which is the percentage change in savings associated with a percentage change in the after-tax rate of return.

As a matter of theory, savings can either rise or fall in response to an increase in the after-tax rate of return.[4] The empirical evidence is, however, frustratingly inconclusive. As a general statement, my (perhaps selective) read of the empirical literature is that there is little evidence that tax policy affects aggregate savings in a substantial way.[5] I now turn to the taxation of dividends and capital gains in particular.

Both dividends and capital gains in Canada are taxed on a residence basis, on the dividends and capital gains received by Canadians on both domestic and foreign investments. Tax policy as it relates to dividends in Canada has been driven in large part by the view that the corporate income tax acts as a withholding tax on domestic dividends. Dividend income is taxed first at the corporate level under the CIT, and then again at the personal level under the PIT. The idea is that when paying taxes on dividends at the personal level, so as to avoid “double taxation” credit should be given for the taxes paid on the investors’ behalf at the corporate level. In other words, the system should integrate corporate and personal taxes paid on dividends. The desire to integrate the personal and corporate taxes is the rationale behind the dividend tax credit (DTC). I will not go into the details of how the DTC works in Canada; see Michael Smart’s FoN article on dividend taxation in Canada.[6] Suffice it to say that for the most part, and with some small deviations over the years, the DTC has resulted in very close to full integration for the dividends paid by small Canadian Controlled Private Corporations (CCPCs) which are subject to the lower tax rates levied on small businesses.

Prior to 2006 the DTC for dividends received from both small and large corporations in Canada was the same. Since large corporations are subject to a higher statutory CIT than small corporations, this meant that the dividends received from large corporations were under-integrated, and taxed at a higher combined corporate and personal rate than dividends from small corporations. In 2006 the enhanced DTC was introduced, designed to fully integrate dividends paid by large corporations.[7] This means that in the current system dividends received from both small and large corporations in Canada are now (approximately) fully integrated.

With regard to the sensitivity of personal savings to dividend taxes levied on the supply side of the market, both the theory and empirical evidence is somewhat inconclusive. Again, Michael Smart discusses some of this in an earlier FoN article, and I won’t rehash that discussion here.[8] My reading of the research is that it tilts toward the conclusion that there is little evidence that supply side taxes imposed on dividends have a substantial negative impact on aggregate savings or investment.

What about capital gains? The fundamental issue with capital gains is that it is difficult to tax them as they accrue, which is why we tax them on realization, when the shares are sold. Indeed, if we could tax capital gains as they accrue the withholding rationale for the CIT would largely disappear. While some proposals for accrual equivalent taxation of capital gains have been suggested, to my knowledge no jurisdiction has implemented them.[9]

Currently, in Canada 50 percent of capital gains are taxed on realization, effectively cutting the personal tax rate on capital gains in half. This has not always been the case. The inclusion rate was 50 percent from 1972 to 1988, increased to 66.67 percent from 1988 to 1990, further increased to 75 percent from 1990 to 2000, and then fell back to 50 percent from 2000 onward.

In addition to a lower tax rate on capital gains, a lifetime capital gains exemption was introduced in 1985, maxing out at $100,000 in 1987. A separate exemption for qualifying farm and small businesses maxed out at $500,000 in 1990. The general exemption was eliminated in 1994, but the exemption for farms and small businesses was retained; indexed for inflation it now stands at $866,912.

The “lock-in effect” dominates discussions of capital gains taxation. The idea here is that individuals may delay realizing capital gains (lock them in) in response to higher tax rates on those gains. A key metric in this regard is the elasticity of capital gains realizations with respect to the tax rate.

The empirical evidence on the lock-in effect is, again, somewhat variable and inconclusive. It is important to distinguish between the short run transitory effects and long run persistent effects; the latter is more important for efficiency. Most of the empirical studies are for the U.S., where the evidence suggests that while there are sizable transitory effects, the long run effects are relatively small.

For example, a recent Goldman Sachs report anticipating the impact of an increase in capital gains taxes in the U.S. under a Biden administration projects an increase in realizations in the short run as investors un-lock capital gains prior to a possible tax increase, followed by a return to the pre-change realization rates over time.[10] This view is informed by the 2013 increase in the capital gains tax in the U.S., which precipitated short term selling, followed by those at the top of the income distribution actually buying back more stocks than they held prior to the change. The academic research is, as indicated, variable and inconclusive, with long run elasticity estimates ranging from 0 to -1.7.[11] Thus, a 10 percent increase in the capital gains rate is associated with a response ranging from zero to a 17 percent decrease in realizations in the long run; a very wide range to be sure. More recent evidence tilts toward the lower end of the range. For example, a recent NBER study suggests quite low responses at the state level, with elasticities ranging between -0.3 and -0.55.[12]

There have been few Canadian studies. A recent preliminary and unpublished study examines the elimination of the general lifetime exemption in 1994 is consistent with much of the U.S. literature, and concludes that aside from large immediate tax planning effects as investors took advantage of the exemption before it expired, it had only a small impact on realizations in the medium and long term.[13]

While somewhat inconclusive, my read of the evidence on taxation and capital gains, with an emphasis on more recent studies, is that while there does seem to be an effect on portfolio and realization decisions in the short run, in the long run the effect is relatively modest.

To conclude, there are two key take-aways from this commentary. The first is that the allocation of capital income in the form of dividends and capital gains at the personal level is highly concentrated at the top of the income distribution, much more so than is labour income. Secondly, while the evidence is somewhat inconclusive, aggregate savings (the supply side of the capital market) seems to be relatively insensitive to changes in after-tax returns.

The implications of this for tax policy will be discussed in the third commentary in this series, but first I turn to a discussion of the demand side of the capital market and the corporate income tax in the second commentary.

[1] It bears emphasizing that the ideas presented in this series of commentaries are by no means unique to me. Others have made similar arguments, most particularly Boadway (2015, 2019). Of course I bear full responsibility for any misinterpretations on my part.

[2] This is generally consistent with the analysis of the distribution of the tax expenditure of the dividend tax credit discussed in Smart (2017). He calculates that about 40% of the benefit of the dividend tax credit in Canada accrues to the top 1%.

[3] Milligan (2012) and Dept of Finance (2013), which suggests that 90 percent of taxpayers can shelter all of their capital income through RRSPs and TFSAs.

[4] This, of course, is because of offsetting substitution and income effects.

[5] See, for example, Bernheim (2002), Beznoska and Ochmann (2013), Boadway and Wildasin (1994). There is, however, evidence that taxes can impact the composition of savings, for example Bovenberg (1989).

[6] Smart (2017).

[7] Dividends eligible for what I call the enhanced DTC are referred to more correctly as “eligible dividends”.

[8] Smart (2017).

[9] See Auerbach (1991).

[10] As reported in businessinsider.com, October 18,2020; https://markets.businessinsider.com/news/stocks/stock-market-impact-biden-capital-gains-tax-selling-pressure-gs-2020-10-1029691129.

[11] Burman and Randolph (1994), Auerbach and Siegel (2000), Dowd et al. (2012); Agersnap and Zidar (2020). See Milligan, Mintz and Wilson (1999) for a now somewhat dated survey with a discussion of Canada.

[12] Agersnap and Zidar (2020).

[13] Levecchia and Tazhitdinova (2020).