Robin Boadway

Luc Godbout

Michael Smart

This Commentary presents calculations of effective marginal tax rates on earned income for recipients of the Canada Recovery Benefit.

The Canada Recovery Benefit (CRB) is the federal government’s new transfer program for self-employed and other workers ineligible for Employment Insurance who experience significant income loss during the Covid-19 pandemic. CRB offers benefits of $500 per week for a maximum of 26 weeks, to EI-ineligible workers who: (i) earned at least $5000 in 2019, (ii) experience an income decline of 50% or more due to Covid-19, and (iii) are available for and seeking work.

CRB is income-tested. Payments will be taxed back by 50 cents for each dollar that the recipient’s net income (excluding CRB)[1] exceeds $38,000. For a person receiving the maximum $13,000 in 2021, the CRB is fully taxed back when net income (excluding CRB) reaches $64,000. This high rate at which benefits are reduced with income, combined with the marginal tax rates inherent in existing tax, social contributions, and transfer programs, creates the potential for CRB to create disincentives to earn and report income for affected individuals.

In a previous FON Commentary, one of us (Boadway) discussed the incentive issues implied by CRB, based on effective marginal tax rates calculations created by another of us (Smart). Those calculations proved to be incorrect, as first pointed out by another of us (Godbout). This brief Commentary corrects the record, presenting effective marginal rates for CRB recipients in different family types for the province of Quebec.

CRB is a taxable benefit; thus it will be added to other income for the purposes of determining taxable income and so the recipient’s tax payable. As well, CRB received will be included in net income which is used in the determination of other existing measures, including the Canada Child Benefit, the Canada Worker Benefit, and other federal and provincial tax credits.

Thus, as a recipient earns more income above the $38,000 clawback threshold, CRB will be reduced, which in turn reduces the impact of earned income on the taxpayer’s net income, and so reduces the impact of the greater earned income on other taxes payable and other reductions in means-tested benefits. The interaction between the CRB clawback and other tax measures is therefore complicated in general.

Simulated effective marginal tax rates

To illustrate the effects, we simulate the impact of the new benefit on effective marginal tax rates (EMTRs) at each level of the CRB recipient’s earned income over the relevant range, for various different representative family types residing in the province of Quebec. Here, we consider an individual eligible for the maximum CRB that can be received in 2020, which is $7000 before clawbacks. (The maximum is lower than it will be in 2021, because the benefit was not introduced until September of this year.) In these simulations, the effective marginal tax rate is calculated as the change in the recipient’s net fiscal position due to a $1000 increase in earned income (multiplied by 0.1). Net fiscal position reflects not only CRB benefits net of clawback, but also federal and provincial income taxes, payroll taxes, and net benefits under the Canada Child Benefit, Canada Workers Benefit, and the non-refundable GST credit, as well as the Work Premium tax credit, Solidarity tax credit, and Family Allowance in Quebec.

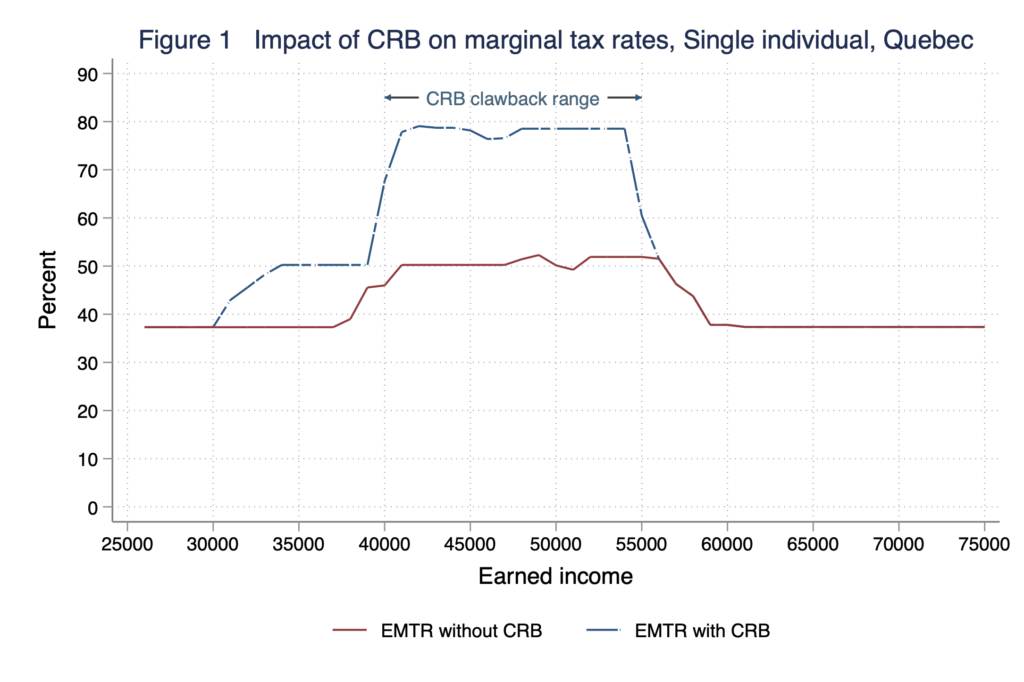

Figure 1 shows EMTRs before and after CRB for an unattached individual. The dashed line is the simulated EMTR schedule with CRB, whereas the solid line is the EMTR schedule in the status quo ante. Observe that the EMTR is higher under CRB at incomes below the clawback threshold, because it is added to net income, and therefore affects the earned income levels at which the recipient reaches higher tax brackets and clawback thresholds for other benefits. The EMTR then rises more sharply with earned incomes above the CRB’s own clawback threshold. Overall, the EMTR rises to as much as 78.5% for a single individual in Quebec.

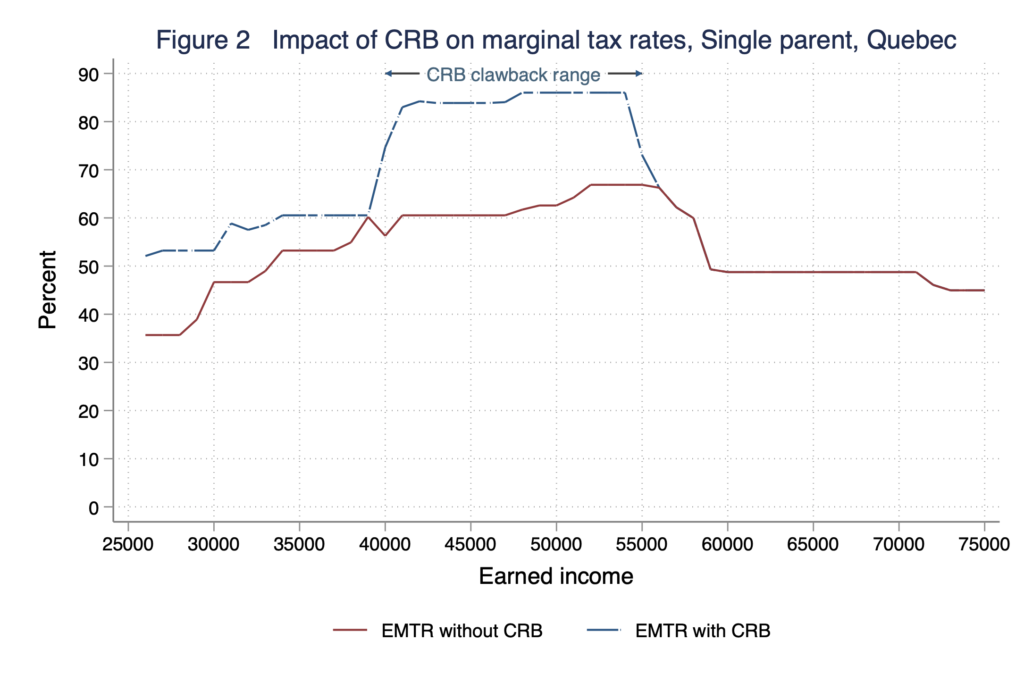

Figure 2 shows the same pattern of effects for a different representative family, consisting of a single parent with a child aged 4. For this family, the maximum EMTR of 86% is reached for earned incomes between $48,000 and $56,000. While the overall EMTR is higher in this case, the impact of CRB on the EMTR is in fact smaller, reflecting the greater impact of the CRB clawback on other benefits received by the family.

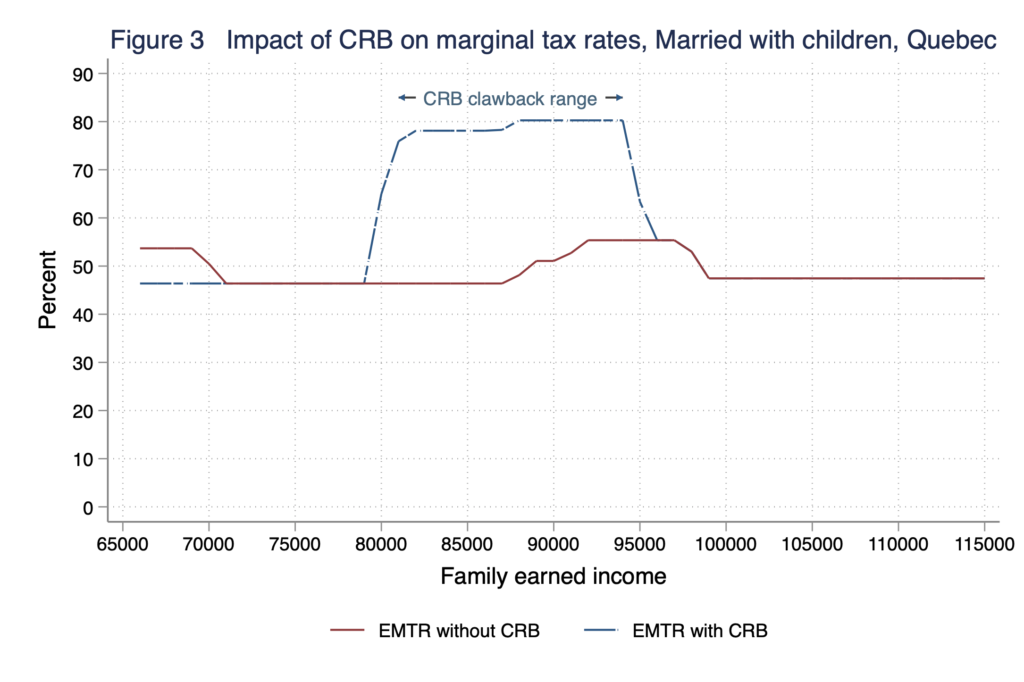

Figure 3 presents simulations for a two-parent family with two children, aged 4 and 6. In this case, we assume that the hypothetical CRB recipient is married to a spouse with $40,000 of employment income, and we present EMTRs on the recipient’s own self-employment income, as a function of the family’s combined earned income. In this case, the maximum EMTR is 80.3%, which is reached for family incomes between $88,000 and $94,000.

Concluding Remarks

The analysis shows that EMTRs will rise substantially for self-employed individuals who receive CRB and report incomes in the relevant income ranges, reaching maximums of 75% to 85%, depending on the family’s characteristics. It seems likely that these high EMTRs could affect the marginal incentives to work and report income for the affected individuals. These incentive effects could be mitigated by reducing the taxback rate of CRB benefits, and possibly adjusting the income ranges at which taxback occurs. Reducing the clawback rate, without complementary reductions in the threshold at which taxback begins, would create new CRB beneficiaries and increase the cost to government. Since this is a temporary program, the government must ask the question: would this additional cost help those who need it most?

[1] More precisely, the CRB taxback calculation will be a function of Net Income Before Adjustments, Line 23400 on the T1 tax form.