The Canada Pension Plan is an important source of retirement income for many Canadians. Interest in a separate provincial plan for Alberta is growing, and the provincial government launched a public engagement on the idea. To help inform this conversation, Finances of the Nation is launching a new tool to help make sense of a separate Alberta Pension Plan.

A separate pension plan for Alberta is an old idea. Indeed, some Members of Parliament speculated about it during the original debate over the Canada Pension Plan legislation in 1965. Starting in the late 1990s, interest in the idea increased among some in Alberta. And following the 2020 report of Alberta’s Fair Deal Panel, the provincial government committed to explore the idea. Most recently, the government started a public engagement in September 2023. It centers on LifeWorks’ analysis, which predicts potentially significant benefits from a separate plan. This has prompted debate (here, here, here, here, and more!).

Given the complexities involved, and the countless uncertainties, Finances of the Nation is launching a new tool to help make sense of it all: an Alberta Pension Plan Simulator!

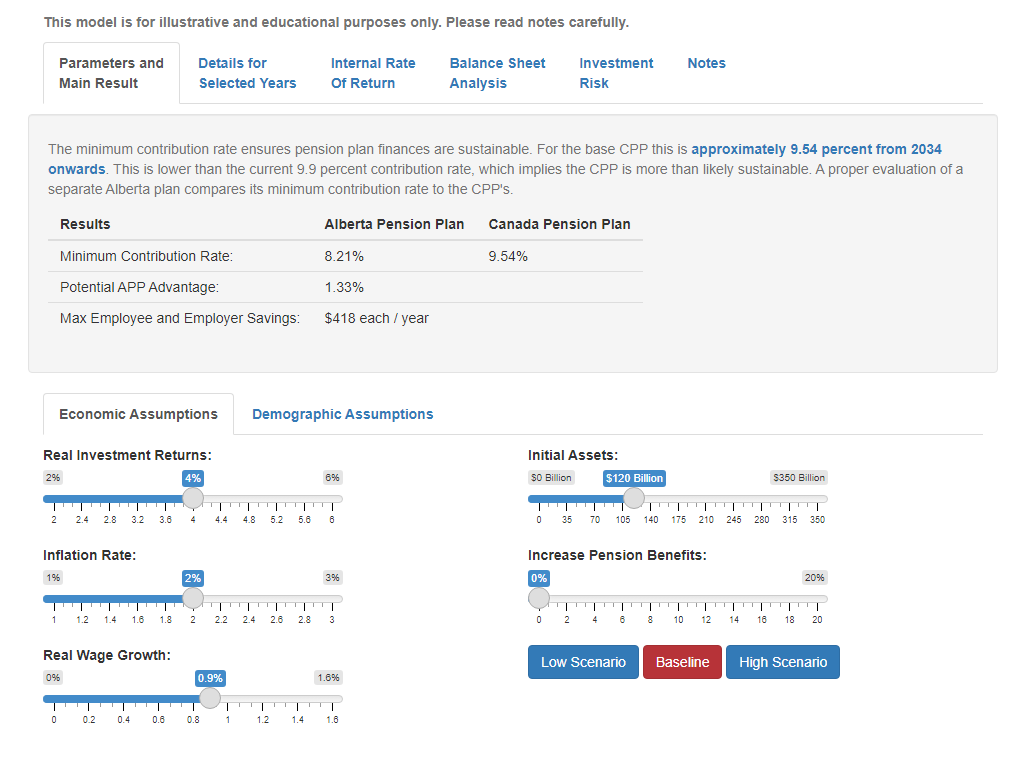

When you first access the simulator, you will be presented with a default set of assumptions. You can change many of them and see the effect immediately. The main outcome is the required contribution rate necessary to ensure the plan’s long-run sustainability. If a separate plan can sustain a lower contribution rate, then there are potential financial benefits for employers and employees. But these benefits may come with additional risk, which the simulator also reveals.

The Minimum Contribution Rate

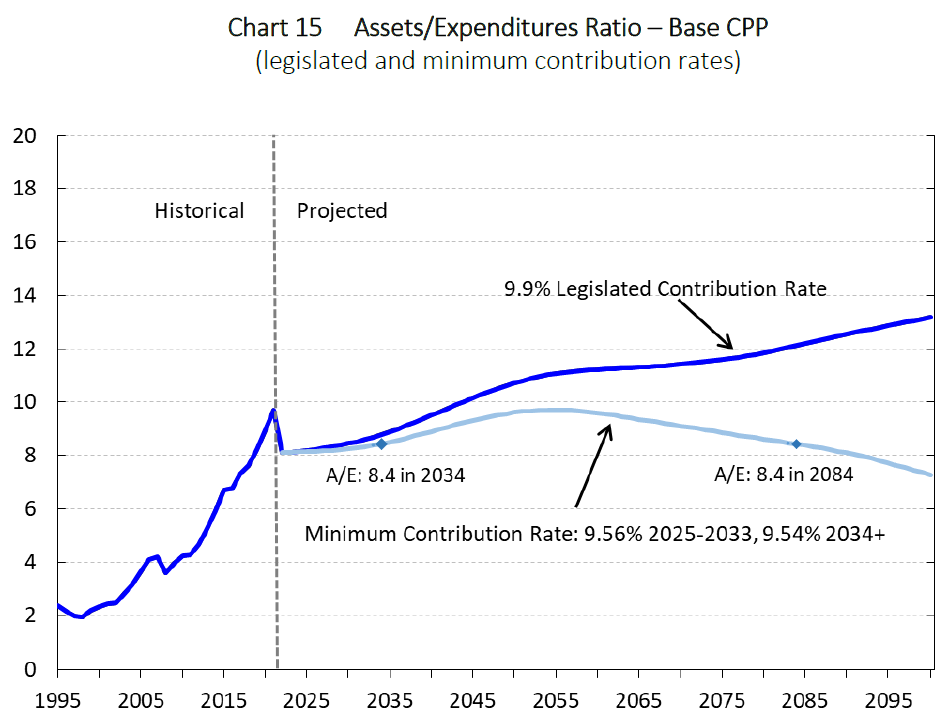

Before illustrating the effect of different assumptions, it is important to understand what the “minimum contribution rate” is. Simply put, this is the fraction of pensionable earnings that must be contributed to ensure the plan’s assets grow with expenditures. The Canada Pension Plan, for example, has a minimum contribution rate of 9.54% from 2034 to 2084. This means the ratio of CPP assets to expenditures is projected to be the same in 2084 as in 2034. This is illustrated well in Chart 15 of the 31st Actuarial Report of the CPP. The current contribution rate of the plan (the rate that we actually pay) is 9.9%, which would result in assets growing slightly faster than plan expenditures over time, as indicated below.

An Alberta Pension Plan

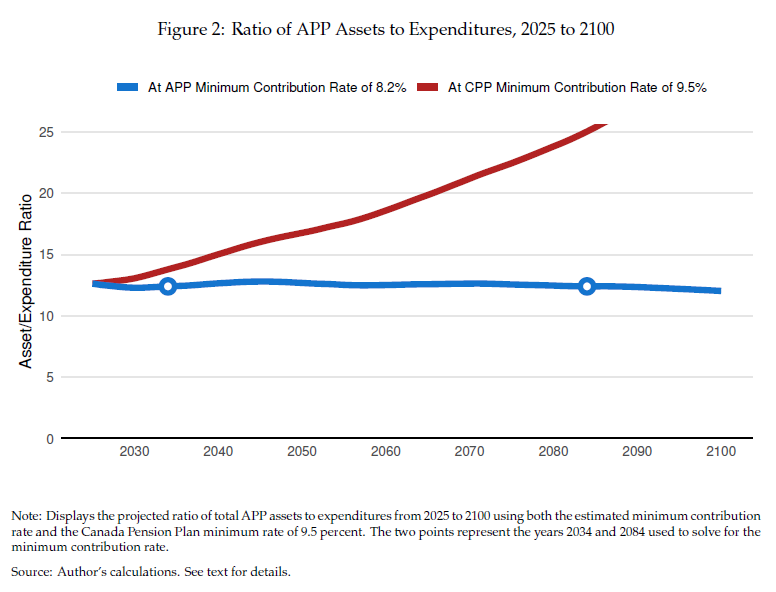

The Finances of the Nation simulator estimates the minimum contribution rate of a separate Alberta Pension Plan. It finds the contribution rate that ensures projected assets relative to expenditures are the same in 2084 as in 2034. This allows for a direct comparison to the CPP minimum contribution rate. In the baseline scenario, the minimum contribution rate is 8.2%. As shown in Figure 2 of Tombe (2023), the working paper on which the simulator is based, an Alberta plan with a 9.5% contribution rate would have assets growing significantly faster than expenditures.

Alternative Scenarios

The simulator allows users to pick their own values for many of the critical components required to evaluate a separate plan. These include both economic and demographic assumptions. In particular,

- Investment returns

- Inflation

- Real wage growth

- Initial assets in the plan

- Increased benefits in the plan relative to the CPP

- Fertility

- Migration

- Mortality rates

Each of these results in different estimates for the estimated minimum contribution rate for the plan. If real inflation-adjusted investment returns are 4.5%, for example, then an Alberta plan may require a contribution rate of 7.6%. This is lower than the 8.2% estimated when real investment returns are 4%. As another example, if Alberta’s net migration rates decline to 0.6% (similar to Ontario’s), then the minimum contribution rate rises to 8.5%.

The simulator can also replicate the results of the Government of Alberta’s preferred scenario. Simply press the “GoA Scenario” button, which yields the 5.9% minimum contribution rate emphasized by the Pension Engagement Panel.

Other Results

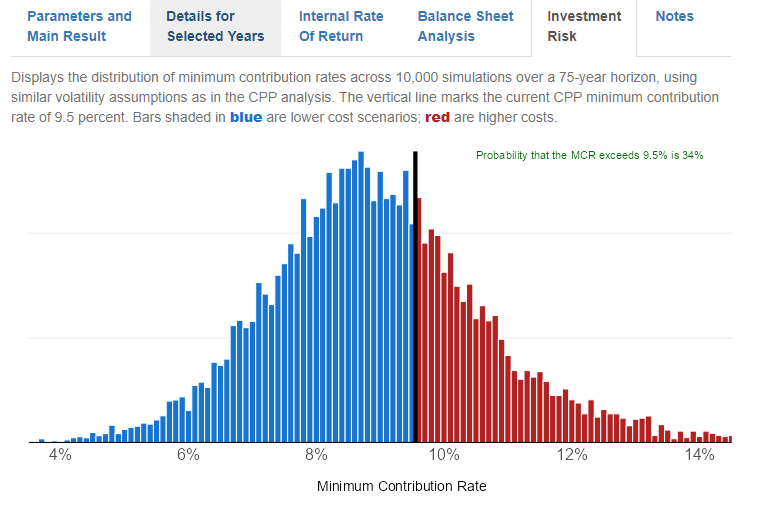

The simulator also provides other useful ways in which one can evaluate a separate pension plan. It reports the internal rates of return for a hypothetical worker earning the maximum pensionable amount, the present value of future obligations and contributions, and the potential investment risks that a separate plan would face.

All pension plans face investment risks when assets are invested in anything but risk-free government bonds. Based on the same volatility assumptions used to evaluate the Canada Pension Plan, the simulator displays the potential distribution of minimum contribution rates for Alberta. It also reports the probability that a separate plan may have a contribution rate in excess of 9.5%. In the baseline scenario, for example, this probability is relatively high, at roughly a one-in-three chance.

Conclusion and Caveats

This simulator is for illustrative and educational purposes only. It aims to provide robust quantitative insight into the potential features of a separate provincial plan. It is not a substitute for more detailed actuarial assessments, which—to be clear—are not yet possible. The underlying model behind the simulator is a recently released academic working paper: Tombe (2023), “The Alberta Pension Advantage? A Quantitative Analysis of a Separate Provincial Plan”. To be clear, it is currently under review and may be subject to change. The simulator will be updated as well, if necessary.

This simulator will hopefully provide Albertans, and all Canadians, with a tool to better understand what various future scenarios may mean for a separate Alberta Pension Plan.