We use data on the distribution of capital gains income across and within income groups to simulate the impact of reforms to increase capital gains tax rates. Readers can use our online tool to explore different possible reforms. A reform that targeted only the highest capital gains income amounts would affect very few families, while raising substantial revenue and increasing fairness in the tax system.

There has been much concern about wealth inequality in recent years, and attention to the issue has grown since the COVID-19 crisis. There have been carefully reasoned proposals for new taxes on wealth, both abroad and in Canada.

But first we should fix the existing tax system. In Canada today, only 50 per cent of realized capital gains is included in income and subject to tax. Professor Kevin Milligan has shown that low taxes on capital gains substantially reduce effective tax rates on high-income individuals, who disproportionately receive their income in the form of gains. As we have previously argued, taxes on capital gains in Canada are lower than for interest income and dividend income, which creates inefficiency in our tax system. Taxing capital gains at the same rate as dividends and interest would fix that loophole and raise substantial revenues.

Some people think that capital gains income goes to middle-class families who receive gains occasionally or as a once-in-a-lifetime event — for example, from the sale of a business or liquidation of a retirement investment portfolio. According to this view, increasing capital gains taxes could be unfair, and it could face substantial pushback from the electorate. In response, economist Rhys Kesselman has recently proposed a reform that would target tax increases only to those with the highest levels of annual capital gains.

A two-rate capital gains tax

Under one version of the Kesselman proposal, the capital gains inclusion rate would rise, but taxpayers would receive an exemption from the new tax for annual gains up to some limit. (Kesselman considers an exemption level of $20,000 in particular.) Gains below the exemption level would remain subject to the current 50-per-cent inclusion rate — that is, they would continue to taxed at one-half the taxpayer’s ordinary tax rate. Only annual gains above this limit for each taxpayer would face a higher rate.

This is a novel proposal worthy of consideration by governments. We have simulated the effects of this reform for tax revenues and the distribution of family income in Canada. (The data for the interactive simulation model presented here come from the longitudinal administrative databank, a 20-per-cent sample of all tax returns in Canada. The construction of the simulation sample is described in more detail in our recent article in the Canadian Tax Journal.

Our interactive simulation model, displayed below, permits the user to experiment with different threshold and tax rates for the reform. It also shows the impacts on all income groups in the population, from the bottom 10 per cent to the top 0.01 per cent. To deal with the concern that receiving capital gains is a rare event that pushes up incomes temporarily, we classify families by their average income over the previous five years — a better indication than annual income of their relative well-being over their lifetimes. This is a “static” simulation model, which assumes that taxpayer behaviour would not change if tax rates were to change. That is probably the right model for capital gains taxes, which may affect the timing of capital gains, but probably don’t much affect how much gains income is realized over the long run.

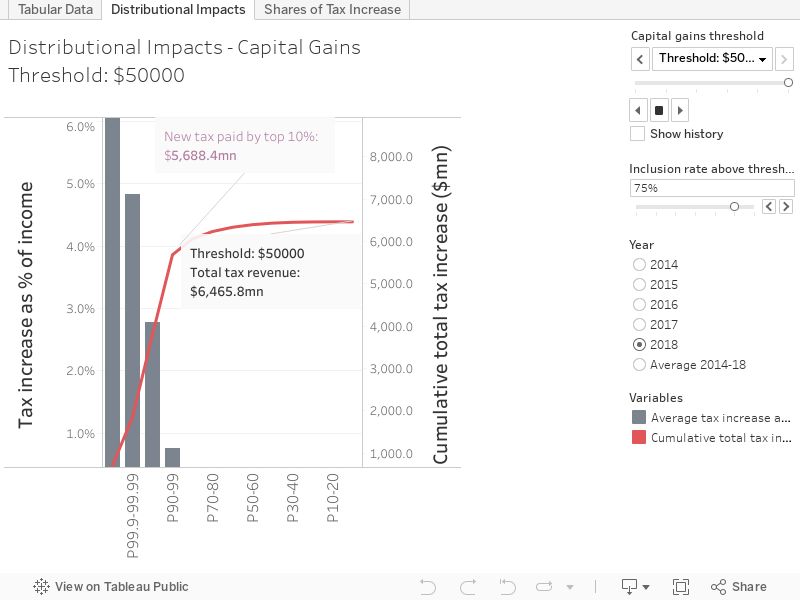

Figure 1

Figure 1 from the simulator shows the impact of any chosen reform parameters on the total increase in tax revenues paid by each income group from the top to the bottom. Milligan showed that average tax rates at the very top in Canada were lower than would be expected given our progressive rate structure, because top-income families receive much of their income in lightly taxed capital gains. The figure also shows how the reform would affect the average tax rate in each group, increasing overall tax progressivity.

Figure 1 shows that the Kesselman reform would raise substantial revenue, even with a relatively high annual threshold. For example, a 75-per-cent inclusion rate applied to all positive capital gains would have increased federal and provincial personal income tax revenues by $8.5 billion in 2018. But under this scenario, 17.4 per cent of Canadian families (those with positive gains) would have paid more tax. In contrast, with an exemption threshold of $50,000 per taxpayer, the reform would have raised a still substantial $6.5 billion in new revenues, and only 1.8 per cent of Canadian families would pay more in tax. In the bottom half of the income distribution, only about 0.3 per cent of families would pay any additional tax. (To animate the impact of the changing threshold, click on the triangular “play” button in the upper right corner of the figure.)

This reflects the extreme inequality in capital gains income, even within income groups, with a small number of taxpayers realizing very large gains, while most taxpayers outside the top-income groups receive little or no gains income at all.

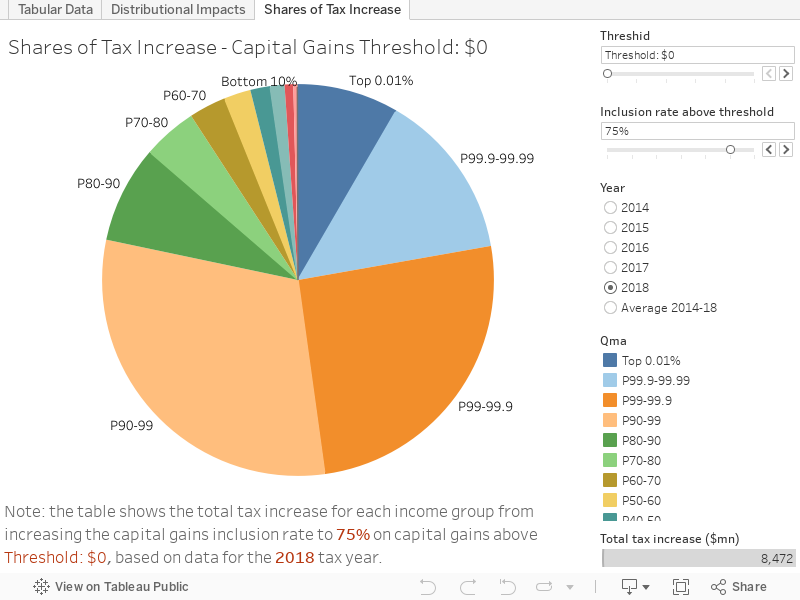

Figure 2

The Kesselman reforms would impose new taxes mainly on families in the top-income groups, particularly if they were implemented with a high annual threshold. This is apparent in Figure 1 from the shape of the curve depicting cumulative tax revenues generated by top-income groups. The curve becomes “flat” below the top 10 per cent of the distribution, especially for high thresholds, indicating that 90 per cent of all families would pay comparatively little tax in the reform.

The same information is even more apparent in Figure 2, which depicts the total tax increase of each income group in a pie chart. With an annual threshold of $20,000 as proposed by Kesselman, about 54.5 per cent of the additional $7.2 billion in tax revenues in 2018 would have been paid by families in the top one per cent of incomes, and 84.6 per cent by those in the top 10 per cent.

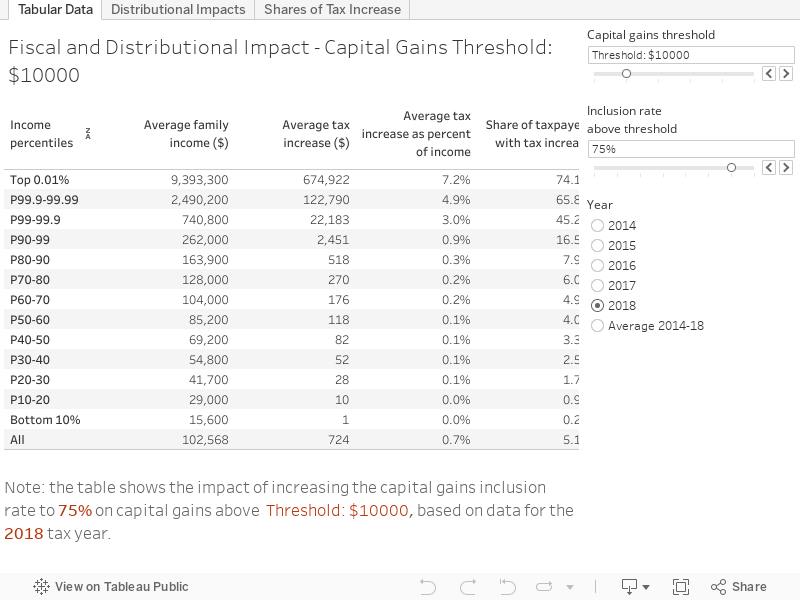

Figure 3

The simulator reports its results in visual form and as tables of key impacts for each income group and in the aggregate. The full database is available for download by interested researchers and policymakers.

Concluding Remarks

The Kesselman proposal considered here is just one way that capital gains tax increases could be targeted to the wealthiest families. Certain issues — such as the treatment of gains realized by corporations, the treatment of capital losses and the potential for tax arbitrage — remain to be worked out. The interested reader should consult the full Kesselman report for Finances of the Nation, which lays out the key issues and considers alternative reform proposals as well. The simulation model presented here offers a way of visualizing the impacts of such a reform. The key message that emerges is that capital gains income is highly unequally distributed, both across and within income groups. That means that the current tax advantages for gains are highly inequitable, and that reforms to increase gains tax rates could be targeted to a small group of taxpayers who benefit disproportionately from the current tax preference.