Trevor Tombe

A new tool from Finances of the Nation helps make sense of the long-term fiscal sustainability of Canada’s federal government. Under several reasonable scenarios, the government’s finances are sound. But under others, concerns around long-run sustainability may mount.

Early in April, the federal government released its budget for the upcoming 2022/23 fiscal year. While there is much to unpack, the federal financial trajectory and its overall fiscal sustainability is an important metric to understand.

Following the more than $352 billion in total COVID-related financial support provided in recent years (and detailed thoroughly in the budget’s appendix), some people are concerned about whether the future trajectory of the federal debt is sound.

Perhaps anticipating such concerns, the government included several long-run fiscal projections that span a wide variety of scenarios. While previous budgets have included long-run debt projections, the 2022 budget was — to my knowledge — the most-detailed ever in this regard.

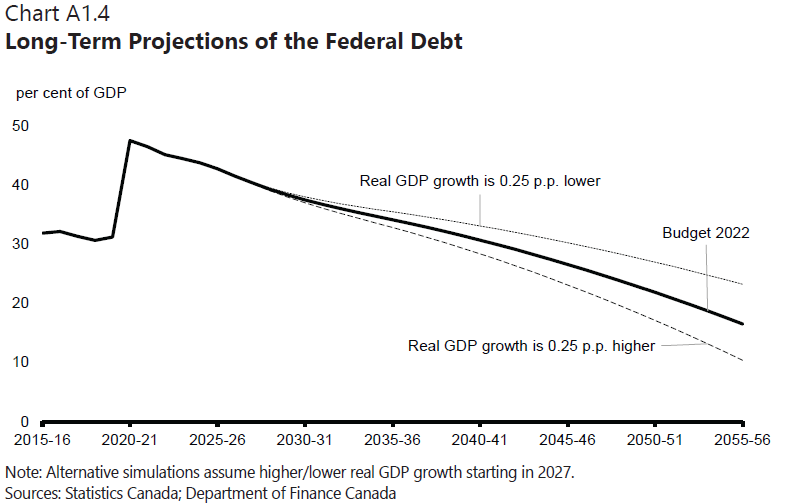

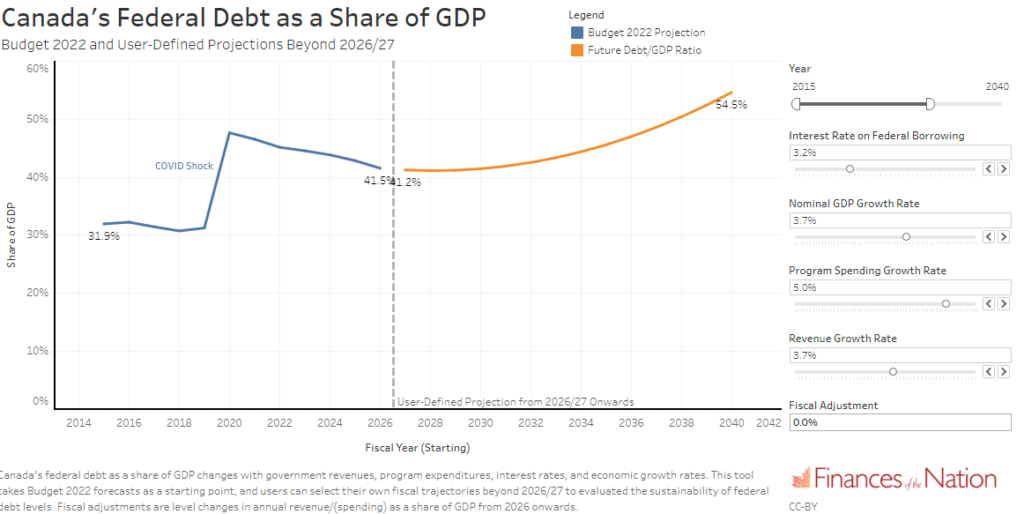

The government’s projections showed a clear decline in the debt trajectory. In their baseline scenario, Canada is on track to unwind COVID-related debt by the late 2030s.

I reproduce the main result below:

A stable or declining debt-to-GDP ratio is a strong indicator of fiscal sustainability. Indeed, it is the primary metric used by forecasters — including the Parliamentary Budget Officer, the International Monetary Fund, and academic analysis for Finances of the Nation.

But how reliable are these projections? How sensitive are they to changes in underlying assumptions? The government explored some alternative scenarios, all of which show finances are fiscally sustainable. But countless plausible scenarios show the reverse and reveal risks we should consider.

A new tool

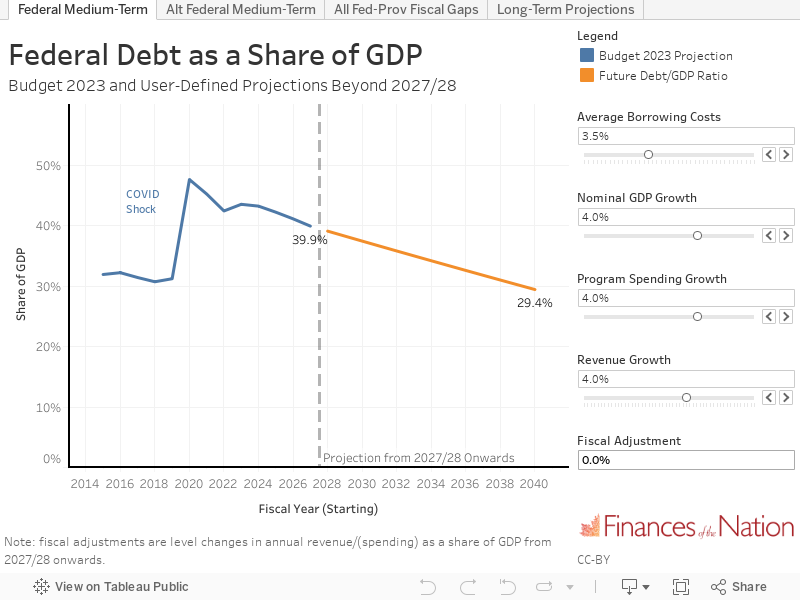

This new tool from Finances of the Nation will help make sense of federal fiscal sustainability. Users can change economic growth rates, interest rates, program spending growth rates or revenue growth rates to determine the impact of alternate scenarios. In addition, users can change the overall level of federal revenue and spending.

You can access the new tool within our Debt Sustainability Simulator and I link to it directly here:

Based on reasonable assumptions beyond 2026, it does appear that Canada’s COVID-related debt will unwind in a reasonable timeframe. Users can even select later years out to 2055 if desired.

The real value of the tool is in exploring alternative scenarios. I’ll illustrate some alternatives below.

Exploring fiscal sustainability

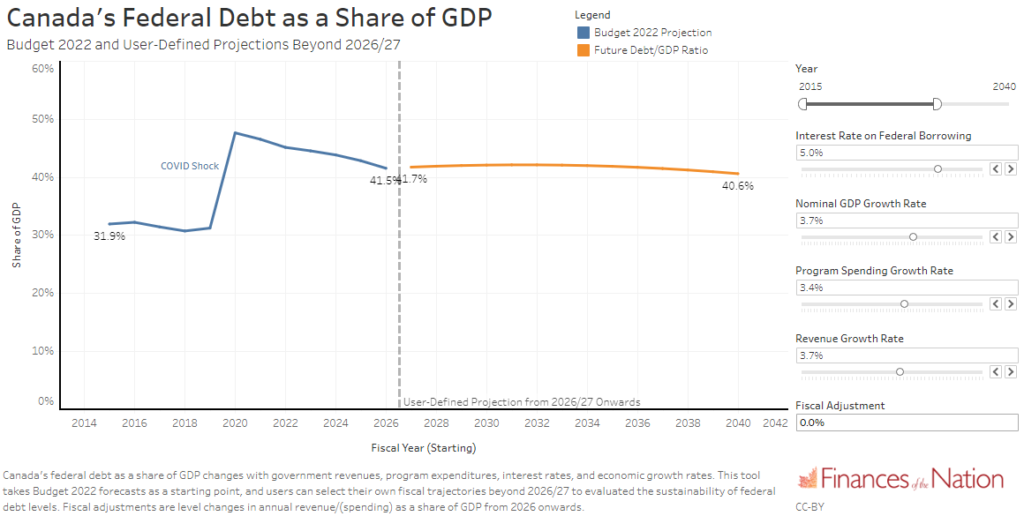

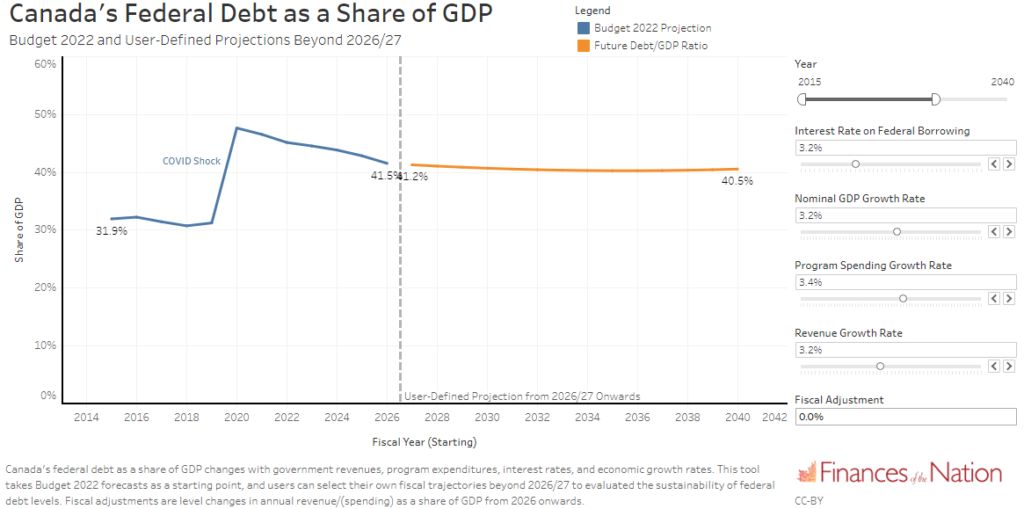

The baseline projections shows debt as a portion of GDP at approximately 31 per cent by 2040. But if interest rates go higher — to four per cent, for example — then debt is 35 per cent of GDP by 2040. If interest rates rise to five per cent, then debt ratios do not decline at all! This reveals how high interest rates must go for there to be some real concerns. That is, while a stable debt-to-GDP ratio is sustainable, interest rates beyond this level would feature rising debt ratios and therefore be unsustainable.

What if interest rates remain relatively low but economic growth slows? A similar result occurs. Consider, for example, economic growth and revenue growth rates of 3.2 per cent instead of the baseline assumption of 3.7 per cent. In this case, debt also does not decline relative to Canada’s economy.

Government spending decisions matter as well. Between 2015-16 and 2026-27, the average growth rate in program spending is more than five per cent per year. If that pace continues beyond 2026, then debt levels not only fail to decline but also begin to rise unsustainably. By 2040, the simulator suggests debt reaches nearly 55 per cent of GDP.

Of course, higher spending is sustainable if revenues also increase. For example, federal debt falls to pre-COVID levels by 2040 with program spending growth of four per cent per year if revenues rise by 0.7 per cent of GDP. This is large (approximately two GST points). You can explore these and other changes in the tool! Many scenarios are more positive than the baseline projection displayed by default. Several others, however, are less so.

Conclusion

Exploring these simulations provides important information about long-term financial pressures and risks facing the federal government. Many (perhaps most) reasonable scenarios feature sustainable finances and largely agree with the analysis put forward in the 2022 budget. But spending growth needs to be more restrained. Even excluding COVID-related spending, future increases must be lower than the post-2015-16 period. If higher spending is the goal, however, raising taxes will need to be a part of the conversation.

Whatever the goal, understanding the long-run path that current fiscal policy choices puts us on is key. This tool may help.

Trevor Tombe is a professor of economics at the University of Calgary, research fellow at the School of Public Policy, and co-director of Finances of the Nation.

Trevor Tombe is a professor of economics at the University of Calgary, research fellow at the School of Public Policy, and co-director of Finances of the Nation.

Image Credit: Shubham Sharan, Unsplash.