Christine Neill and Saul Schwartz

The NDP and the Liberals have both announced promises to set a zero interest rate on student loan debt. The idea is to help former students who are struggling to repay their loans. But this will not help those most in need — borrowers in the Repayment Assistance Program (RAP) who already pay zero interest, as well as borrowers in default who are at risk of financial penalties.

Jagmeet Singh made a splash recently with a tweet saying the Trudeau government was profiting from student loans, and that an NDP government would set the interest rate on federal student loan debt to zero. The controversy over the first assertion has distracted from the proposal itself, which was unfortunate because it was the most substantive proposal on financial aid to post-secondary students in the campaign at that time. The Liberal platform, just released, makes the same commitment.

So, what would the change mean for students? Who would benefit, by how much and is it a good way to improve affordability and access to post-secondary education?

The short answer is that a zero-interest-policy would do little to encourage lower-income students to go to university or college, and would benefit only a relatively small number of people struggling with student debt. There are alternative policies – including further expansion of the existing program that helps those on lower incomes, as well as more debt forgiveness more quickly — that would be better-targeted at those most in need.

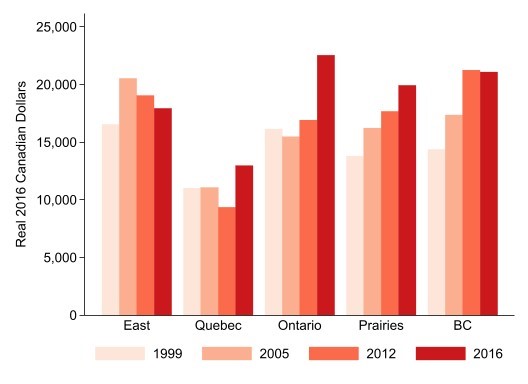

Figure 1. Student loan debt in real terms for households with student loan debt, by broad region and year

Source: Survey of Financial Security, 1999, 2005, 2012, 2016

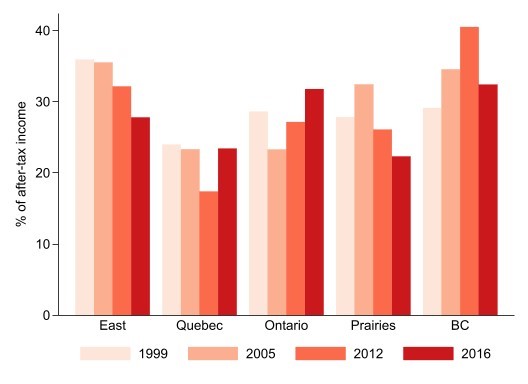

Figure 2. Student loan debt as a percentage of after-tax income for households with student loan debt, by region and year

Source: Survey of Financial Security, 1999, 2005, 2012, 2016

Background: how much student loan debt do Canadians have?

Total student loan debt owed by Canadian households stood at around $37 billion in 2016, according to the Survey of Financial Security. Overall, about 12 per cent of Canadian households carried student debt – a figure that has been stable for the past two decades. For that 12 per cent of households, total debt has risen somewhat in real terms across much of Canada since 1999 (Figure 1), but rising household incomes means that it has been mostly stable or even decreasing as a percentage of after-tax income for those households (Figure 2).

Not all this debt is owed to the federal government, however, because student loan programs are a joint federal-provincial program (although Quebec runs its own system, with some funding from the federal government). In 2019-20, the federal government was owed slightly more than $20 billion by 1.8 million borrowers, for an average loan balance of $11,400.

The average debt owed to the federal government at the time of leaving school for those who took out federal student loans – roughly half of all college and university students – was $13,549. For students who borrowed for certificate or diploma programs, the figure was $10,053, while for those who borrowed for bachelor’s degree programs, it was $16,345. Borrowing was substantially higher for MA and PhD programs. Fifteen per cent of school leavers with student loans had a federal loan balance of more than $25,000.

One reason that governments run student loan programs is that private lenders might not lend to young people with limited financial resources who have no physical asset that can be sold or repossessed in the event of a failure to repay. Governments can step in and, if they choose, can potentially make money on the loans by charging interest on student loans, as long as not too many students default.

While this could mean that a student loan program could bring in more revenue than it costs to make the loans, that is not the case for the Canada Student Loan Program (CSLP). In 2018-19, interest revenue was $852 million, but the costs of borrowing were $687 million, and the write-off of debts that were deemed unrecoverable was $300 million. In addition, the administrative costs were $137 million, and payments to provinces (mostly to Quebec for running their own student loan program) were $500 million.

Overall then, even without considering the $1.5 billion in federal grants to students, the CSLP runs at a net cost to government coffers. It can be seen as moving money around in time – giving money up front to students while they are studying and most in need of funds, with repayments later after they have left school, albeit not quite enough to cover the outlays.

How does repayment work and who would benefit from a zero interest rate on federal student loan debt?

But the repayment program also moves money around from those with higher lifetime incomes to those with lower lifetime incomes. This is partly because federal student loans are available only to those with relatively low family incomes while studying. But it is also because of the way the repayment system works.

There are two ways to repay student loans: through a mortgage-style system, with fixed monthly repayments over a 10- or 15-year term, or through the Repayment Assistance Plan (RAP), a program that sets payments at an affordable level for those with lower incomes.

Under RAP, the monthly payment is zero for a single person with an income below $40,000 (higher for those in larger families), and repayments cannot be more than 10 per cent of income.

Around 30 per cent of borrowers use RAP in the first year after leaving school, and about 20 per cent of all borrowers who have left school are in the system at a single point in time. Of these, more than 85 per cent are on zero payments, with no interest accruing. So, a reduction of interest rates to zero would not change anything for this group. The 15 per cent of RAP borrowers who are making affordable payments pay interest first, though if the payment is lower than the interest charge, the government pays the rest. Reducing the interest rate to zero would mean that their monthly payments would go entirely to reducing their principal. That would be one positive result.

A whole other group of borrowers — more than 200,000 at last count — are in default, meaning that more than 270 days has passed since they last made a payment. Meanwhile, interest is still accumulating on their loans. Their credit ratings will have deteriorated and if they ever file a tax return, any refunds can be taken by the CRA and given to the CSLP. Defaulters are not eligible for RAP but can enrol in it if they first “rehabilitate” their loan by making two regular monthly payments and either paying the accumulated interest or adding it to the amount they owe.

Borrowers must apply for RAP — enrolment is not automatic — and if accepted must reapply every six months. For borrowers who have been in RAP for 60 months, the federal government will start paying the principal and interest on the loans, ensuring that the loan is repaid in full after 15 years. The government also starts paying off the loans of borrowers who have been repaying their loans for 10 years after leaving school.

Loans can be discharged in bankruptcy if more than seven years has passed since the borrowers were in school. In addition, borrowers can apply to the court system for a discharge on the grounds of “undue hardship” if more than five years has passed since they left school. This is quite rare, but useful for those in extreme financial difficulty.

Finally, interest for all borrowers in repayment is currently suspended through to the end of March 2023, a temporary response to the labour market disruptions due to the COVID-19 pandemic.

Recent changes to the repayment program

In recent years, RAP has become more generous and more easily accessible. Substantial improvements were announced in the federal budget in 2021, including an increase to $40,000 from $25,000 in the income threshold below which no repayments are expected, and a reduction in the cap on the percentage of income that can go to student loan repayments to 10 per cent from 20 per cent.

Currently, interest rates on floating rate loans are set at prime (currently 2.45 per cent) and for fixed rates at prime plus two percentage points (so currently 4.45 per cent). These were cut in the 2019 budget from prime plus 2.5 percentage points and prime plus five percentage points respectively. That budget also eliminated interest for the first six months after graduation, and made it easier to rehabilitate debt, and thus be eligible for RAP, by not requiring accumulated interest to be fully repaid prior to rehabilitation.

How much would a zero interest rate save borrowers?

Let’s consider how much would be saved in total interest payments over the life of a loan under the regular repayment program by cutting interest rates to zero for the average borrower from a BA program, graduating with $16,345 in federal debt (while noting there will be no changes for any provincial debt.)

Assuming the borrower chooses the regular repayment program at the current fixed rate, waits for six months after graduation to begin repayments, and repays over 15 years (the longest standard option), total interest saved would be $5,900, or $393 per year. For the default option of repayment over 10 years, saving would be slightly less than $3,750, or $375 per year. Under the current floating rate, assuming it lasts throughout, saving on a 10-year loan would be $2,000, or $200 per year. (You can run your own scenarios using this calculator).

There’s another wrinkle in estimating how much the affordability of college or university would change if interest rates are cut to zero. Tax credits for student loan interest payments available at the federal level and in all provinces except Ontario mean that a refund is effectively given for between 15 per cent (Ontario) and 30 per cent (Quebec) of all interest payments made. Each $1,000 reduction in interest payments, therefore, would actually mean only a net $850 back in the pockets of Ontario graduates, or $700 for Quebec graduates.

Those with more federal borrowing will save more. While that might seem to mean those who need the most help benefit the most, as noted earlier, borrowing is greater for university than college students, and greater for MA and PhD students than undergraduate students. But university graduates also tend to earn more than college graduates, and those with MAs and PhDs earn more than those with BAs. As a result, the types of students who borrow more also tend to have higher incomes after leaving school and are better able to repay the debt. Default rates for these groups tend to be lower than for groups that tend to borrow less.

A significant proportion of borrowers would not benefit at all, because they already have a zero interest rate – specifically, all students in the first six months after leaving studies (between three and five per cent of all borrowers in repayment) and all borrowers in RAP with zero repayments (roughly 20-25 per cent of borrowers in repayment). Further, because of the current moratorium on student loan interest, a permanent zero-interest-rate policy will save borrowers money only after March 2023.

Conclusion

If the goal of a zero-interest-policy is to target assistance to those struggling with repayments after leaving school, several other policy changes would be better.

First, RAP could be further improved, building on the changes in the federal budgets of 2019 and 2021. Most ambitiously, RAP could be made the default repayment plan for all borrowers, removing the need for those eligible to reapply every six months, as well as making repayments simpler and more predictable for students.

Second, allowing earlier debt reduction would help many of those struggling the most. The NDP has also said it would consider across-the-board debt reductions, while the Liberal platform mentions debt forgiveness for professionals working in rural areas. A change to RAP that allowed for phased-in debt relief for those with low incomes before they have spent 60 months on RAP or before they have been in repayment for 10 years since leaving school would more effective than such one-off debt forgiveness.

Third, making student loans dischargeable in bankruptcy would help those in the greatest financial trouble, even though it would affect relatively few borrowers.

The zero-interest-rate policy benefits people after they have left school. It will not give more people better access to post-secondary education. Money for student support is likely better distributed to students at the time it is most needed – while they are in school, not after leaving it. Nor will the zero-interest-policy go very far toward reassuring students that they will not face ruinous repayment demands after leaving school. A zero-interest-policy provides money when it is less needed, and given how Canada’s student loan repayment works, will disproportionately benefit those who are not struggling with repayment. The money the NDP and the Liberals want to spend on making student loans interest-free would be better spent in ways that help those most in need.

Christine Neill is an associate professor of Economics at Wilfrid Laurier University, specializing in education and post-secondary financial aid policies.

Christine Neill is an associate professor of Economics at Wilfrid Laurier University, specializing in education and post-secondary financial aid policies.

Saul Schwartz is a professor at the School of Public Policy & Administration at Carleton University, specializing in social policy, the economics of education and labour economics.

Saul Schwartz is a professor at the School of Public Policy & Administration at Carleton University, specializing in social policy, the economics of education and labour economics.