Wei Cui

The federal government is right to extend its fiscal programs supporting businesses and workers through the pandemic. One major reason is that they have been helpful to part-time and temporary employees — not just the original target of the self-employed and workers in the gig economy.

In the 2021 budget released on April 19, the federal government announced extensions of the major fiscal programs supporting Canadian businesses and workers through the COVID-19 pandemic. These include:

- the Canada Emergency Wage Subsidy (CEWS), now extended from June to September 2021 although the subsidy rate will be gradually reduced starting in July;

- enhanced Employment Insurance (EI), although “future, long-term reforms to EI” are left to “targeted consultations” in the next two years;

- the Canada Recovery Benefit (CRB), extended by 12 weeks to a maximum of 50 weeks. It will be phased out by September 2021. Lower rates will be paid in some cases, particularly after July.

While calibrating these programs to a faster-than-expected economic recovery, the budget preserves the course set out in the fall economic statement. There are many reasons why staying that course is wise.

One such reason is that policy-makers, like many commentators, still seem to hold a partial, even inaccurate, picture of “flexible work” in Canada. For example, In anticipating the examination of “the main systemic gaps exposed by COVID-19” in the EI program, the budget continues to emphasize “the need for income support for self-employed and gig workers.”

In reality, the bulk of flexible work now takes place in the formal employment sector in terms of part-time and temporary workers. The pandemic revealed the vulnerability of these people just as much, and possibly more, than it did that of the self-employed and gig workers.

Moreover, CEWS and CRB may have been particularly effective at delivering benefits to part-time and temporary employees. In addition to the consultations announced in the budget on the future of EI and other measures, the government should carefully study CEWS’ and CRB’s actual impact during the pandemic.

Data from the Labour Force Survey (LFS) shows the portion of unincorporated self-employed workers (i.e., self-employed individuals who do not own the corporations for which they work) was 8.5 per cent of all Canadian workers in 2020, just slightly above the average of 8.4 per cent since 2011. In contrast, the fastest-growing category of “non-standard” work in recent years has been temporary employment (full- or part-time). The proportion of such workers to all Canadian workers reached a peak of 11.7 per cent in 2017. Even after suffering the most severe contractions in 2020, that figure still stood higher than unincorporated self-employment — at 9.8 per cent of all workers.

If we define non-standard workers as a combination of the unincorporated self-employed, temporary employees and permanent part-time employees, then the most notable change in recent years has not been an overall expansion. The ratio of non-standard workers to total workers in Canada has remained at around 30 per cent since 1997. Instead, it is the increasing share of employees — part-time and temporary — within the category of non-standard workers, which rose from 64.8 per cent in 1998 to 73.4 per cent in 2017.[1]

The sizeable flexible employee population raises two types of challenges for redesigning income-assistance and labor-market interventions.

First, even flexible employees who are EI-eligible may be inadequately protected by EI, while they are more adversely affected by the pandemic (or other similar shocks in the future) than both full-time employees and the self-employed.

Second, it may be that when “standard” employees (i.e., those who hold permanent full-time positions) are subject to an adverse economic shock, both the initial deterioration of their circumstances and their paths of recovery go through non-standard employment. That is, “standard” employees no longer face just two states of the world — permanent full-time employment or unemployment — but also a third, in-between state of “flexible employment.” Any insurance scheme or other new government program must address this third state as well.

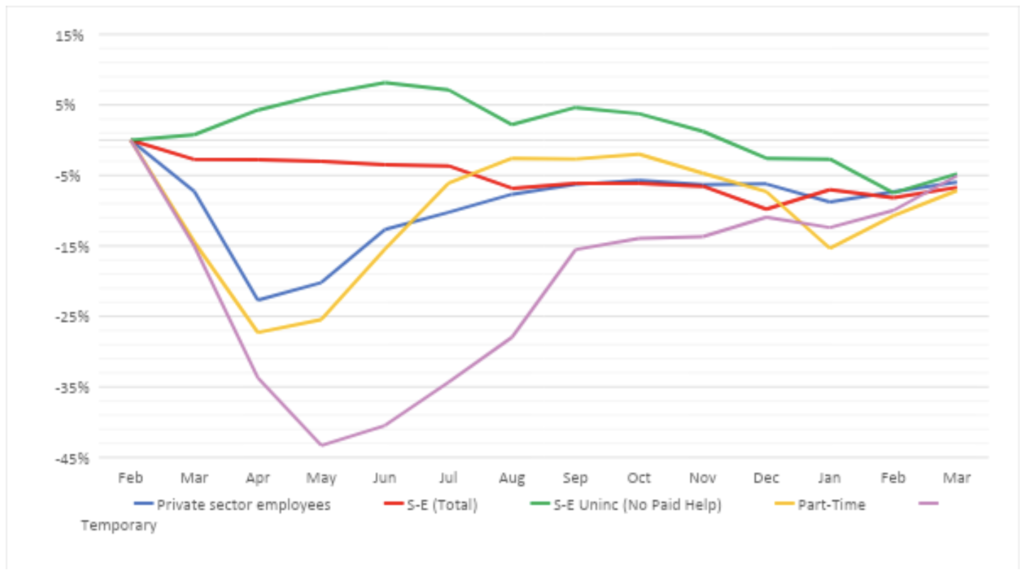

Figure 1: COVID-19 Impact on Non-Standard Work Positions

Figure 1 illustrates the pandemic’s extensive margin impact — on the total number of positions — for three types of work: temporary employment, part-time work, and self-employment.[2] (The type of self-employment that is most important in terms of the number of individuals involved, unincorporated self-employment, is displayed separately for clarity.)

The graph shows that in 2020 by far the most negatively affected portion of the workforce was temporary employment. By May 2020, close to 45 per cent of temporary jobs had been lost, compared to about 20 per cent for all private sector employees. Recovery of temporary jobs also lagged behind the recovery of private sector employment in general, and was less complete by February 2021.

Figure 1 also shows that during the early months of the pandemic, the job loss for part-time positions was also worse than the average for all private sector employment. Although part-time work recovered more during the second half of 2020, it again dipped below the private sector employment average beginning in December 2020. By contrast, unincorporated self-employment rose relative to February for most of 2020, likely driven by job losses in the formal employment sector.

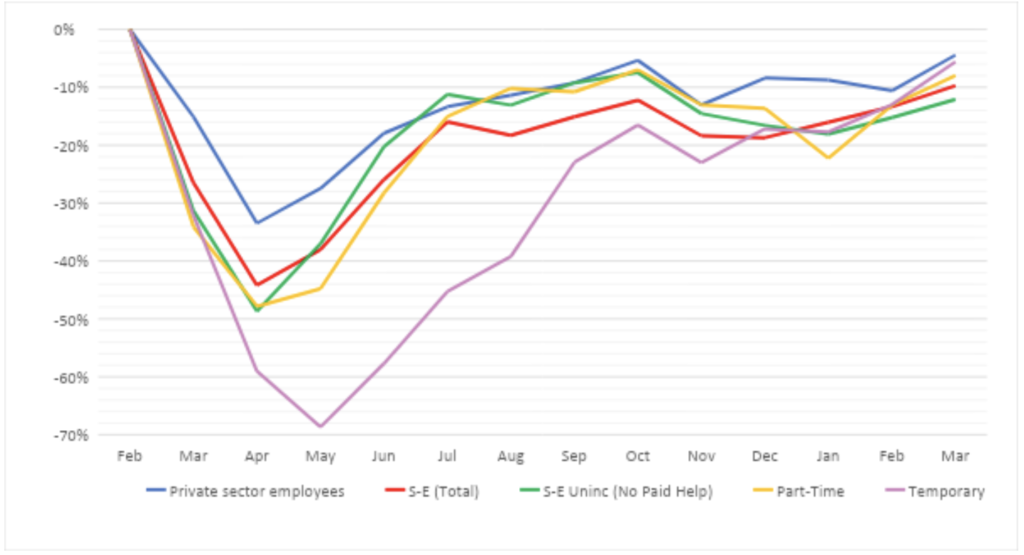

Figure 2: COVID-19 Impact on Aggregate Hours Worked by Non-Standard Workers

Figure 2 looks at the pandemic’s intensive margin impact — in terms of aggregate hours worked — on the same three types of work. For all types of work, the intensive margin impact of COVID is more severe than the extensive margin impact. Notably, during most months, the private employment sector as a whole suffered smaller losses than the self-employed sector — the reverse of the pattern observed on the extensive margin. But the greater losses for “flexible employees” are the same as on the extensive margin. The greatest loss again accrued to temporary employment — aggregate work reduction reached close to 70 per cent in May 2020. The recovery of hours among part-time employees followed a largely similar path as the unincorporated self-employed, generally below private sector average.

Figures 1 and 2 indicate that part-time and temporary employees were more vulnerable to the pandemic’s adverse effects than both self-employed and full-time workers. At least in the aggregate, there is no evidence of part-time work substituting for full-time work, the way there is evidence of self-employment substituting for full-time work.

What about the impact of Canada’s fiscal response on flexible employees? One can attempt some inferences here. Government statistics report that the cumulative number of unique applicants under CRB was 1.84 million individuals as of April 4, 2021. By the time of CRB’s inception in October 2020, aggregate reduction in hours worked relative to February 2020 for self-employed Canadians was 15 per cent. Because eligibility for CRB requires a worker to have experienced at least a 50 per cent income reduction, it is reasonable to infer that no more than 30 per cent of all self-employed individuals in Canada made CRB claims. There were 2.843 million self-employed Canadians at the end of 2019. This suggests that no more than 840,000 CRB claimants could have been self-employed workers. Therefore, the majority of CRB claims were made by employees — either temporary or part-time. In other words, despite the CRB being heralded as employment insurance for the self-employed, more CRB benefits are likely to have been delivered to part-time and temporary employees. Given the latter’s plight, that seems to be a good thing.[3]

Policy-makers’ views about flexible employment are likely to influence income assistance provided. For example, if one views part-time work as an abnormal outcome, one will be less willing to extend assistance to part-time workers. One might also withdraw benefits from workers who transition to part-time work from either full-time employment or unemployment.

To illustrate this last point, consider an employee whose hours were reduced by 50 per cent during the second half of 2020, and whose employer needed to decide what type of government support to tap into for her and similar employees. One option would have been to enter into a work-sharing agreement. Under such an agreement, the employer would continue to pay for the employee’s hours worked, while the government would pay the employee for the hours not worked at the regular EI rate. The maximum EI benefits the employee would receive is the product of $573 per week (55 per cent of maximal insurable earnings) times 50 per cent (the proportion of hours not worked) or a total of $286.50. If the employer claimed any CEWS benefit, the EI benefits claimable by the employee would be reduced dollar-for-dollar. By contrast, if the employee chose not to participate in work sharing, but to claim CRB benefits instead, she would receive payment from the government of $500 a week. The employer, at the same time, may claim CEWS benefits up to 75 per cent of wages paid.

This calculation makes work sharing look like a non-starter. In fact, the actual take-up rate for work sharing — 132,423 employees are estimated to have participated as of April 2021 — may now look high, instead of looking low. Why would anyone join work sharing, when CRB is in place and especially when the employer is eligible for CEWS?

Why should CEWS claims reduce government payouts to employees participating in work sharing? The only explanation that comes to mind is that policy-makers feared that CEWS subsidies would encourage employers to keep work-sharing arrangements longer than is necessary. In other words, even when pandemic recovery is still ongoing, the designers of work sharing viewed reduced hours worked as an abnormal and undesirable outcome.

More straightforward examples can be given to show that both EI and work sharing strongly disfavour flexible employment, relative to CRB/CERB and CEWS.[4]

Arguably, much of the policy debate about Canada’s pandemic fiscal response in 2020 missed these important facts. Both proponents and critics of the government’s policies emphasized self-employed individuals and the extensive margin of employment — how many jobs are retained — at the expense of neglecting adverse changes on the intensive margin of employment suffered by part-time and full-time employees. The generosity of the CRB/CERB and CEWS came miraculously, it seems, despite such neglect.[5] An important topic for future investigations, therefore, is the extent to which these programs actually helped the majority of Canada’s non-standard workers.

[1] See Wei Cui, “Non-Standard Employment and Canada’s Initial Pandemic Response” (2021) 69(2) Canadian Tax Journal.

[2] Figure 1 provides a more complete picture of COVID’s impact on flexible work than Chart 2.6 in the budget, which does not separate out temporary and part-time employment from permanent full-time employment.

[3] It is even clearer that the large majority of applicants for CERB benefits were dependent employees, rather than the self-employed. Government statistics indicates that as of October 2020, there were fewer than 1.4 million active EI beneficiaries. Yet the cumulative number of unique applicants for CERB and EI benefits during the COVID pandemic was 8.9 million individuals. Thus, the vast majority of the 8.9 million individuals received CERB as opposed to regular EI payments. It follows that even if all of Canada’s 2.8 million self-employed workers claimed CERB benefits, an even greater number of CERB claimants were employees.

[4] EI disfavours flexible employment mainly through its work-while-on claim rules. Work-sharing arrangements largely exclude part-time and temporary workers in the first place, so that not only the incentives but even the opportunity for such workers’ participation are absent.

[5] The budget’s proposal to double Canada Student Grant for two years, at the cost of $3.135 billion, also gives some help to some flexible employees.