Michael Smart

Federal emergency wage subsidies are poorly targeted, resulting in a fiscal cost of about $14,500 for each person-month of employment saved through the program, or $188,000 per job year. Reductions in subsidy rates which began in September had only small impacts on employment, while reducing the fiscal cost of the program substantially. More recently, the government has backed away from those reforms, freezing subsidy rates and extending the program in 2021. The decision to back away from the September reforms was a mistake and a gradual phaseout of subsidies should start again now.

In Monday’s mini-budget, Finance Minister Chrystia Freeland threw so many numbers at us – with so many zeroes after them – that Canadians might be forgiven for missing some important announcements, so here’s one number to bear in mind: $97.6 billion. That’s the new projected cost of the Canada Emergency Wage Subsidy (CEWS) through June of 2021. CEWS is now the largest component of Ottawa’s pandemic response, outstripping even the Canada Emergency Response Benefit (CERB) and its successors.[1] So, what is it buying us?

In this commentary, I present statistics on claims and payouts under the program from aggregate administrative data released by the Canada Revenue Agency. I focus on the impacts of reforms to the program in September that reduced subsidy rates substantially for many employers. Using evidence on the change in claims around the reform, I estimate the number of jobs saved by CEWS and the cost of each job saved.

Although claims have declined somewhat as the economy has improved since the early summer, CEWS spending and the number of assisted employees remains high. While the September reforms resulted in a substantial decline in the average subsidy per worker, there was no sharp drop in the number of firms applying or workers assisted. This evidence suggests the CEWS subsidy is not in fact saving many jobs and that the cost per job saved is therefore high.

The problem of incrementality

The federal government has taken decisive action this year to address the economic effects of the pandemic lockdowns. That was the right thing to do. A key part of that response, CEWS is a subsidy of up to 75% for eligible payroll expenses of virtually all Canadian businesses that have experienced a revenue decline since the beginning of 2020. The program has paid out over $50 billion to 350,000 different businesses so far, and current spending is running around $1.2 billion per week.

The idea behind CEWS could make sense. By lowering the cost of retaining workers for struggling businesses, the program should help to reduce unemployment and keep incomes flowing. But at what cost? The problem is that CEWS payments are paid for all workers at affected businesses, not just those facing the prospect of earnings losses. For this reason, CEWS is an expensive way of protecting vulnerable workers.

Most of the jobs funded by CEWS would still exist in the absence of the subsidy. An effective business subsidy directs funds only to activities that would not happen in its absence – a property known as incrementality. Because new jobs are not being targeted in CEWS, the program has low incrementality, and a high fiscal cost per job saved.

Perhaps recognizing the problems, in September Ottawa implemented reforms to reduce the subsidy rates and phase the program out over time. That change was controversial, leading to pushback from business lobby groups and stories in the media suggesting that the program was in serious decline. However, a closer look at the reforms leads to different conclusions.

Jobs saved through CEWS: Preliminary evidence from the September reform

The government has not yet released detailed data on CEWS claims made by individual employers which would facilitate a detailed study of the program’s impact on employment. But we can develop preliminary evidence by examining how aggregate claims changed following the September reforms that reduced the subsidy rates for many employers. If the subsidies play a significant role in preventing job loss, then the September cuts should have led to an increase in layoffs at assisted firms, and a resulting decline in the number of workers supported by the program beginning in September. But that is not what the aggregate data suggest.

CEWS was introduced on March 15 as a 75% subsidy to eligible payroll expenses of Canadian businesses that had experienced a revenue decline of 15% or more. Eligible payroll expense is capped at $1129 per employee per week, for each four-week period of the program. The threshold revenue decline for eligibility was increased to 30% for April through June (Periods 2-4).

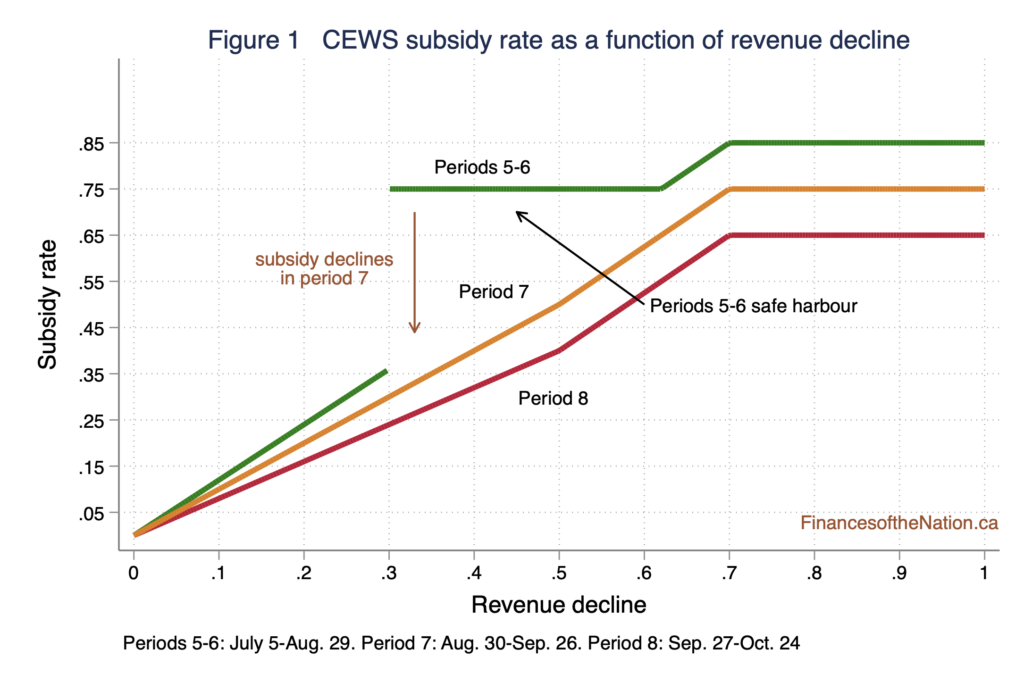

For Periods 5 and 6 (July and August), the program was expanded. All employers experiencing revenue declines were eligible for a base subsidy rate equal to 120% of the percentage revenue decline, with slightly higher top-up subsidy rates for revenue declines over 50%.[2] But firms whose subsidy rate under this formula would have fallen compared to Period 4 were eligible for a “safe harbour” provision entitling them to the 75% subsidy rate they would have received under the old formula. The government announced the safe harbour provision would end in September, and that base subsidy rates would decline gradually in Periods 7 through 10 (September to December).

Figure 1 shows CEWS subsidy rates as a function of each applicant’s revenue decline for reporting periods from July through October (Periods 5-8). The safe harbour provision kept the subsidy rate at 75% in July and August for those with revenue declines over 30%. Beginning in September, the subsidy rate declined for all applicants, with the sharpest drop for those in the middle range of revenue declines, where the safe harbour applied.[3]

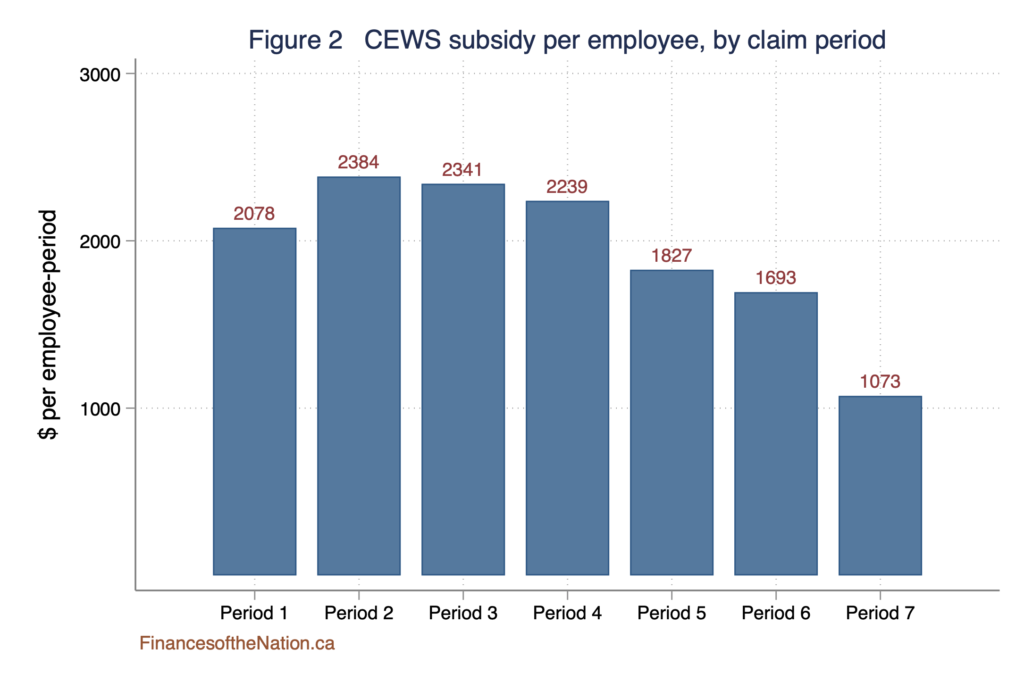

The reform had a substantial impact on program costs. Figure 2 shows the average subsidy paid per employee supported for each claim period (month) through August, the most recent available in the public CRA data. The average subsidy paid reflects the average wage of those who are supported, as well as the impact of the subsidy changes, but it is a good measure of the impact of the reform. The average subsidy dropped from $1,693 in July to $1,073 in August, a decline of about 46%. By way of comparison, the subsidy rate decline shown in Figure 1 for employers in the safe harbour range was between 15% and 60%.

The question is: Did the subsidy rate cuts in September cause layoffs among CEWS-eligible employers? This is a difficult question to answer for two reasons. First, employment levels at CEWS applicant businesses may be rising over time due to the effects of the economic recovery, unrelated to the reform itself. If so, then my comparisons will underestimate the number of layoffs caused by the CEWS reforms. To minimize the bias, I compare only August and September data, when other effects on employment should be small.

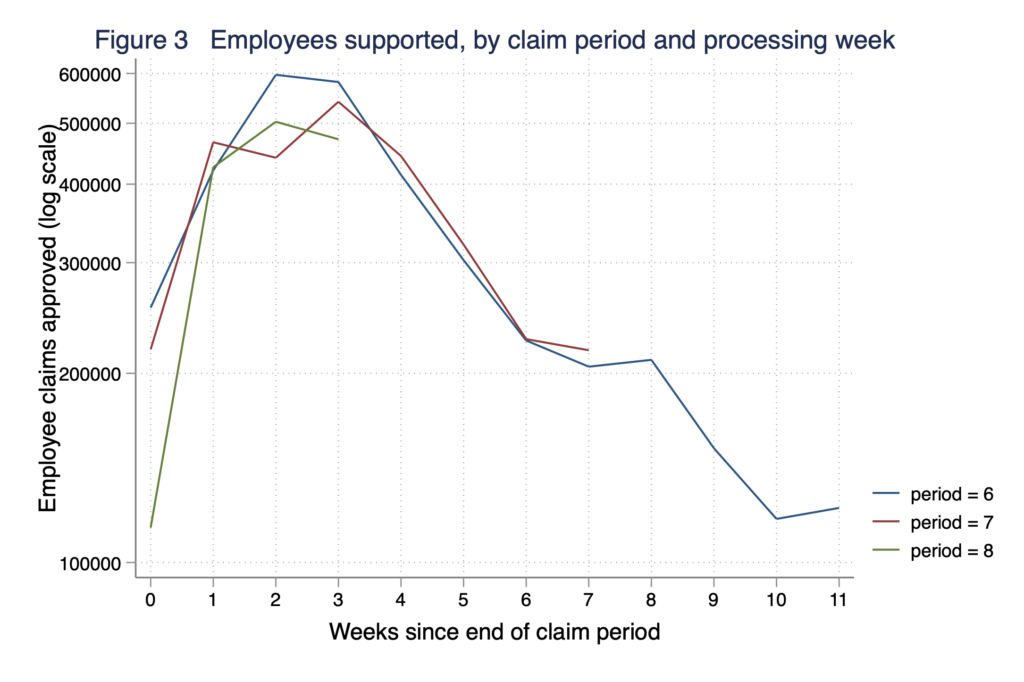

Second, employers apply retrospectively for the subsidies after the end of each period, and there is no deadline for applications in respect of prior periods. So data on applications for each claim period accumulate only gradually, and a larger percentage of the final total has now been received for earlier than later claim periods. At the time of writing, only four weeks of claims history for Period 8 had been reported by CRA, eight reporting weeks for Period 7, and 12 for Period 6. To deal with reporting lags, I will compare total claims in Periods 7 and 8 to claims in Period 6 after the same number of reporting weeks. Thus I compare Period 7 claims on November 28 to Period 6 claims on October 25, the same number of weeks after reporting began.

Figure 3 shows the number of employees supported in each week after reporting starts, for Periods 6 to 8. Claims follow the same pattern closely in all three periods. This suggests that total claims in the eighth reporting week are a good predictor of what ultimate total claims will be. But employee claims were somewhat lower in Periods 7 and 8 than the pre-reform period, particularly in the data released in the third and fourth weeks after reporting began.

In all, the total number of employees supported by reporting week 8 of Period 7 was 2,874,710, compared to 3,000,790 at the same point in Period 6. Thus, employment in assisted firms declined by 4.2% in the month following the reform. Since the subsidy rate declined by 45% over this period, and with again the caveat that other factors may have influenced employment, this suggests that a 10 percent increase in the subsidy rate leads to just a 1.1 percent increase in employment at affected firms.

Because the estimated impact of the subsidy on employment is small, most jobs subsidized through CEWS would still exist if the subsidy rate were reduced further. Thus the policy has low incrementality. To save a single job with an increase in the subsidy rate, it is necessary to subsidize many more jobs that were not at risk. Based on this estimate, I calculate[4] that CEWS subsidies cost the government about $14,500 for each job saved over a four-week period, or about $188,000 per job per year.

Even by the standards of past job creation programs, that is far from a good deal. This should not be a surprise. Past economic research tells us that employment is not very responsive to wage costs in the short run.

If CEWS funds are not saving many jobs, that means they end up in business profits. That could help the hardest-hit businesses weather the storm of the COVID crisis. But, here too, CEWS does not effectively target those most in need. Last week, we learned of one large retailer that in effect used its CEWS payments to fund a special dividend to shareholders this year. Reflecting the importance of this issue, some other countries have banned extraordinary payouts to managers and shareholders by companies taking the wage supports.

Other issues

While the September reforms appear to have been successful at reducing program costs, they did create a new class of problems. Employers’ wage subsidy rates now automatically fall as business revenues recover towards their pre-pandemic levels. This “clawback” of subsidies from growing businesses has exactly the same effect as a tax on gross revenues. It creates a disincentive to grow business operations during the recovery, and it could force businesses to increase retail prices to cover costs.

And the tax effect is substantial. For a typical retail business, payroll costs are 40 percent of gross revenues on average. Under the CEWS clawback rules for Period 8 and beyond, that means a $1,000 increase in revenues will result in a $320 reduction in CEWS payments. That’s a 32 percent marginal tax rate on revenues that struggling businesses must pay, in addition to their normal business taxes.

Of course, a 32 percent gross revenue tax is bad policy, whether in good times or in the course of a fragile economic recovery. But Ottawa has slipped one into its wage subsidy program, apparently without much discussion.

The way forward

CEWS is an expensive and ineffective policy, because it was not targeted to the jobs that were most at risk during the lockdown. A conservative back-of-the-envelope calculation tells us that CEWS has been paying businesses $14,500 per month for each job saved by the program. There are far better ways to assist the recovery.

Other countries have recognized the problems with wage subsidies this year and have since made reforms. The United States offered similar support in the spring through the Paycheck Protection Program, albeit only to smaller businesses. Researchers found it had virtually no impact on employment, and it has since been wound down.

Ireland and Australia also operated similar wage subsidies in the early months of the pandemic. Both countries reduced subsidies and tightened eligibility in September and, unlike Canada, they have stuck to the plan. The result is more cost-effective programs, better targeted to the hardest-hit businesses.

Most European countries do not offer general wage subsidies to businesses at all. Instead, they offer “job retention” schemes that encourage employers to put workers on short hours instead of laying them off. That targets assistance to the jobs that are most at risk, exactly as Canada should be doing.

A few weeks ago, Finance Minister Freeland praised the European approach, calling it “something that Canada should be paying a lot of attention to.” Will something like it be coming to Canada soon?

[1] The fiscal cost of the Canada Emergency Response Benefit (CERB) was $81.6 billion. Including the cost of temporary expansion of Employment Insurance, the total for direct benefits to unemployed workers will be $91.1 billion.

[2] For quarterly revenue declines more than 50%, the marginal increase in the subsidy was 125% of the revenue decline, and the maximum subsidy rate 85%.

[3] The top-up subsidy rates are based on average revenue declines in the prior three months, not just the current month. The rates shown in the figure assume that the revenue decline is constant over time.

[4] Using the standard formula for marginal excess burden of a subsidy, net government expenditure per job saved is approximately

ΔG / ΔL = sw (Δs/s) / (ΔL/L) – (b – sw)

where s is the subsidy rate, b the unemployment benefit, w is the average wage, L the number of assisted workers, and ΔL is the change in employment resulting from a change in the subsidy rate of Δ s. The first term in the expression is the direct fiscal cost of the subsidy, and the second term is the “fiscal externality”: the impact of increased employment on CEWS subsidies, net of the CERB and EI benefits saved by reducing unemployment. To perform the calculation, I set the initial subsidy rate to sw = 1693, and the elasticity term (ΔL/L)/(Δs/s) to 0.11, as implied by the Period 7 data. Note that I assume that laid off workers are entitled to a benefit of $500 per week under enhanced EI, so that the net fiscal cost per month is b-sw = 307.