By Michael Smart

Photo from Jonthankslim, Wikimedia

The federal debt is rising fast and is likely to reach at least 63 percent of GDP by 2025, a level not seen since the fiscal crisis of the 1990s. But the current low level of interest rates (if continued in the future) mean that the debt-to-GDP ratio is sustainable and will likely decline gradually over time, without the need for any sharp fiscal consolidation in the coming years.

In the dire economic situation following the pandemic lockdowns, Ottawa had to act. And act it did, borrowing massively to fund new measures to insure families and firms against declines in income. And so federal debt is rising sharply, and some commentators are sounding the alarm. Should we worry about the debt?

Federal debt: How high will it go?

In his last economic statement, former Finance Minister Bill Morneau predicted net debt would rise to 50 percent of GDP this year, compared to 31 percent last year. But that reflects only the fiscal measures announced as of July. As CERB is extended and replaced by other measures, the debt will surely come rise more. It seems likely that federal net debt will reach at least 55 percent of GDP by the end of this fiscal year.

While there are encouraging signs of economic recovery in Canada, there is a real likelihood of a prolonged recession ahead of us. The current emergency measures should be unwound as the crisis ends, but the red ink will continue to flow for a few years to come.

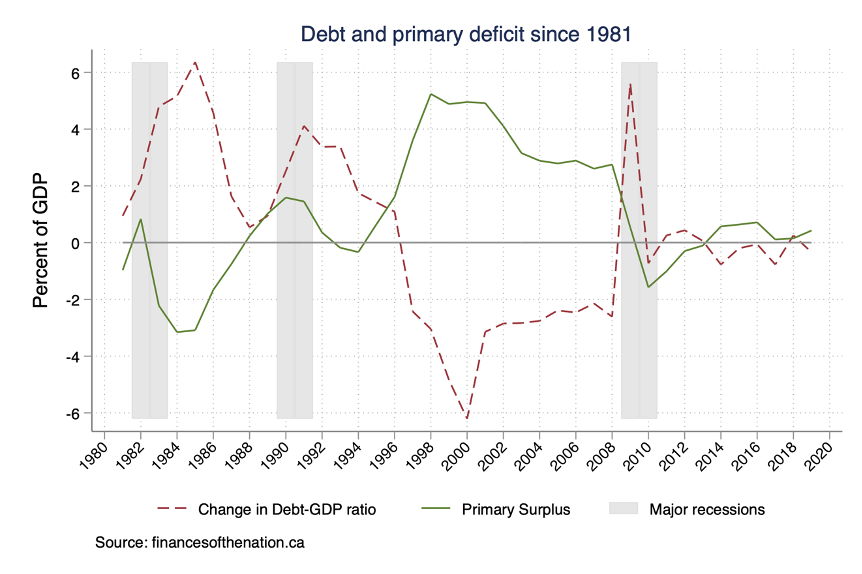

Figure 1 shows Canada’s experience with recessions, deficits, and debt. In the past three major recessions in Canada, the primary deficit[1] rose sharply and remained above trend for five years after the previous peak, contributing an additional 10 percent of GDP to the debt on average. If the current recession is prolonged, we can expect a similar response in 2021 and beyond. Based on these rough forecasts, it therefore seems likely that the federal net debt will reach at least 63 percent of GDP by 2025.

The debt last hit that level in 1996, after Ottawa’s long struggle with recurring deficits and mounting debt following the 1982 and 1990 recessions. Then, following the fiscal consolidations of the Chrétien-Martin years, the debt fell to just 22 percent of GDP by 2008 – a remarkable achievement for the government by any standard, but one that was not without cost for Canadians.

Should we worry?

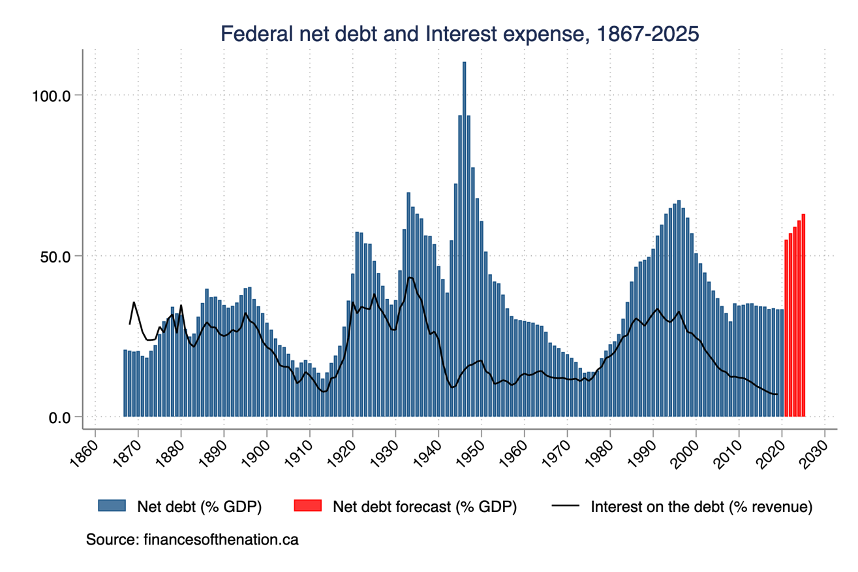

To understand the rise in the debt-to-GDP ratio and what it could mean for the future, it is useful to look at the history of the federal debt in Canada. Figure 2 shows estimated federal net debt as a percentage of GDP from Confederation to today (the data are available here), together with my forecast for net debt to 2025.

As shown in the figure, we are witnessing the largest single-year change in debt’s share in GDP in our history. As the pandemic unfolds, it is likely to reach levels only seen in the aftermath of wars and major recessions in the past. Debt hawks have already taken note, and they are very worried.

But should they be? Figure 2 also shows annual interest payments on the federal debt as a percentage of federal revenue in the 1867/68-2018/19 period. While debt is peaking, the share of interest payments in the budget has never been lower. The reason of course is that long-term interest rates are at historically low levels. And that fact explains a lot about fiscal policy today and in the near-term future.

In the traditional view, government borrowing inevitably implies higher taxes at some point in the future, when debt is retired. Because higher taxes will create economic distortions, the debt-financed spending of 2020 is costly, and those costs will be borne by future generations, creating problems of intergenerational equity.

But what if we simply never pay it back? As the debt matures in future, it could simply be rolled over with new bond issues. The new debt now being issued would still have costs, since the bonds would pay interest forever. But in the current low-rate environment those costs are much smaller than before.

Dynamics of debt

Would such a policy be sustainable for Canada?[2] Letting d = D/Y denote the debt-to-GDP ratio, we can show that debt must evolve over short time horizons according to the rule

Δd = (r – g) d + x

where r is the interest rate on the debt, g is the growth rate of GDP, and x is the primary budget deficit as a percent of GDP. So the change in debt-to-GDP depends on the difference in interest and growth rates (r – g), and on how the government’s policy choices affect the primary deficit.

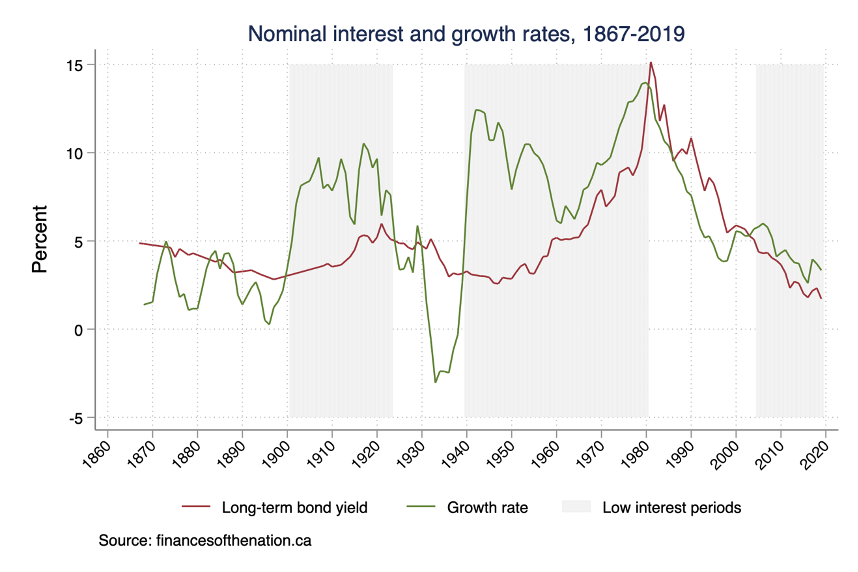

Long-term government bond yields are currently less than one percent, so that r<g surely holds in the short run. If Ottawa returns to primary balance by 2025, then the debt-to-GDP ratio would therefore fall gradually as long as r<g in future.

Figure 3 shows the yield on long-term Canada bonds and the rate of annual GDP growth since 1867.[3] Canada has experienced two sustained periods where r<g, following the major depressions of the 1890s and the 1930s. On average since Confederation, economic growth has exceeded the interest rate by about one percentage point on average. The current r<g episode, which began after the 2001-02 slowdown, is less dramatic than in the past, but annual growth has still exceeded interest rates by about 50 basis points (half a percent) in the current period. In contrast, during the fiscal crisis of the 1980s and 1990s, the inequality was reversed, and interest rates averaged 3 percentage points more than annual growth. That difference means that running substantial primary surpluses was required to “tackle the debt” in the 1990s, but it might not be required this time.

If r<g holds up (and of course it might not), then debt should begin to fall gradually as a percentage of GDP, even if Ottawa continues to run small deficits in future.

This idea is surely driving thinking about the deficit in Ottawa today. r<g is not a panacea for fiscal policy, and the resulting savings will not be large enough to finance large new permanent program spending without tax financing. It simply means that the current emergency measures are not leading to an unsustainable increase in the debt. And that fact might help Canadians of all political stripes to sleep at night.

[1] Primary deficit is the difference between revenue and expenditure, excluding interest on the debt.

[2] In this section, I draw heavily on Olivier Blanchard’s 2019 Presidential address to the American Economics Association, available here.

[3] The 1926-2020 data are from Statistics Canada sources. The earlier data come from a variety of sources to be described in a future FON Commentary. The GDP growth series has been smoothed by computing an 8-year moving average from the annual data.