Michael Smart

The government should temporarily reduce the GST rate to two per cent from five per cent to support the economy until the recovery is well underway. Research shows that sales tax cuts have been passed on to consumers in the past, and they do lead to a surge in consumer demand.

Finance Minister Chrystia Freeland has promised up to $100 billion in new fiscal stimulus beginning with the April 19 budget, which should help to support the economic recovery as the pandemic wanes later this year. But not all stimulus programs are equally effective and not many can be rolled out in a timely fashion. So how should new government support to the economy be delivered?

There is one simple measure that is “shovel ready” and would support consumer spending as the lockdowns and restrictions end. The government should temporarily reduce the GST rate to two per cent from five per cent and keep it there until the recovery is well underway.

Some commentators have in contrast recently called for an increase in the GST to help repay the debt accumulated during the pandemic. Right now, these commentators are simply wrong. As long as output remains substantially below potential, this is the time for fiscal stimulus, not restraint. As well, my research shows that sales tax cuts in the past have been passed on to consumers, and they do lead to a surge in consumer demand.

This recession is unlike any other because it has hit retail and service businesses the hardest, not manufacturing. We can’t rely on large infrastructure spending to boost aggregate demand as we did in the 2008-09 crisis, because construction and manufacturing employment has already recovered in most of the country. Meanwhile, household savings rates are at historic highs, but many Canadian families expect only modest growth in their spending this year, preferring to maintain precautionary savings instead.

A GST cut would encourage consumers back into stores and to take vacations, thus unlocking some of the extraordinary level of personal savings accumulated during the pandemic. That would make use of the “preloaded stimulus” that Ms. Freeland hopes to get from household savings.

A recession-era sales tax reduction is not a new idea. The U.K. government made a reduction in sales taxes a key part of its stimulus package after the 2008-09 financial crisis. The B.C. Liberal Party proposed temporarily eliminating the sales tax in the last provincial election. Several European countries have already implemented sales tax reductions to support their economies during the pandemic.

The GST cut in Canada should be temporary and time-limited. The reduction should take effect on Canada Day (by which time we hope many physical distancing restrictions will have been relaxed), with the normal rate being restored in early 2023.

In fact, the government might consider a temporary increase in the GST rate once the recovery is well underway in 2023 – say to seven per cent and for a limited time. That would give consumers even greater incentives to spend their savings now, as well as generating revenue later to help restore fiscal balance.

The fiscal impact would be substantial. My proposed three-point reduction in the GST would increase the deficit by more than $36 billion over 18 months, or about one-third of Ms. Freeland’s planned total stimulus. The effect could be even greater if provinces were spurred to decrease their rates in tandem with the federal cut.

Cynics will object that a GST cut would be ineffective – either because businesses would not pass on the tax cut to consumers in the form of lower prices,[1] or perhaps because a three-percentage-point tax cut would be seen as “too small” to affect spending. But, here too, the cynics are wrong. Sales tax cuts do get passed onto consumers, and they do lead to a surge in consumer demand.[2]

To show this, I examined the experience around the most recent sales tax cut in Canadian history. In October 2006, Saskatchewan reduced its provincial sales tax rate to five per cent from seven per cent.[3] I examine the impact on consumer prices of affected commodities, and on aggregate wholesale and retail sales in Saskatchewan.

To estimate the economic effects caused by the sales tax cut, we need to know how much prices and sales change after the reform, relative to what would have happened in Saskatchewan had the sales tax rate remain unchanged. I employ the synthetic control method, in effect using an optimally chosen average of the outcomes in other provinces to estimate this “counterfactual” outcome that Saskatchewan would have experienced, had it not cut its tax rate.

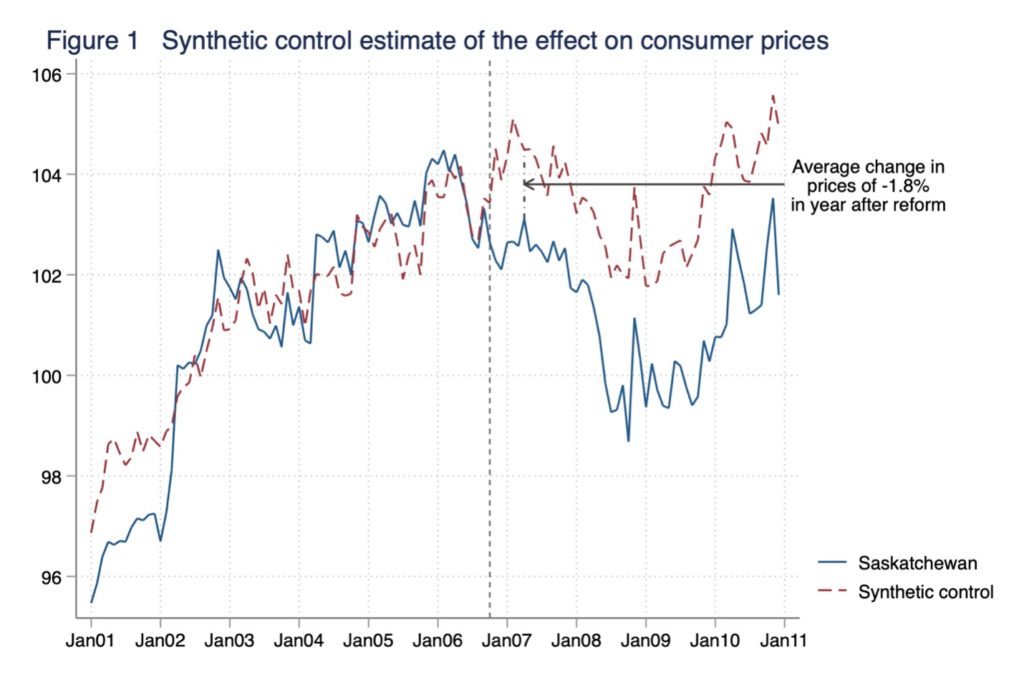

Figure 1 illustrates this method – and shows the first key result on how the tax cut was passed through to consumer prices. The solid blue line in the figure depicts the monthly average consumer price of taxable commodities in Saskatchewan for the 2001-2010 period.[4] The dashed red line depicts the evolution of the same prices in “synthetic” Saskatchewan, a weighted average of prices in other provinces that most closely match the Saskatchewan series and its predictors in the pre-reform period.[5]

The figure shows that prices fell in both Saskatchewan and control provinces in mid-2006, presumably as a result of the federal GST cut implemented in July that year. But prices fell again in Saskatchewan in October with the PST cut, and remained consistently below the synthetic control for the rest of the decade.

On average, Saskatchewan prices were 1.8 per cent lower than synthetic Saskatchewan in the year after the reform. I therefore conclude that essentially all of the two-percentage-point PST cut was passed through to consumers in Saskatchewan.

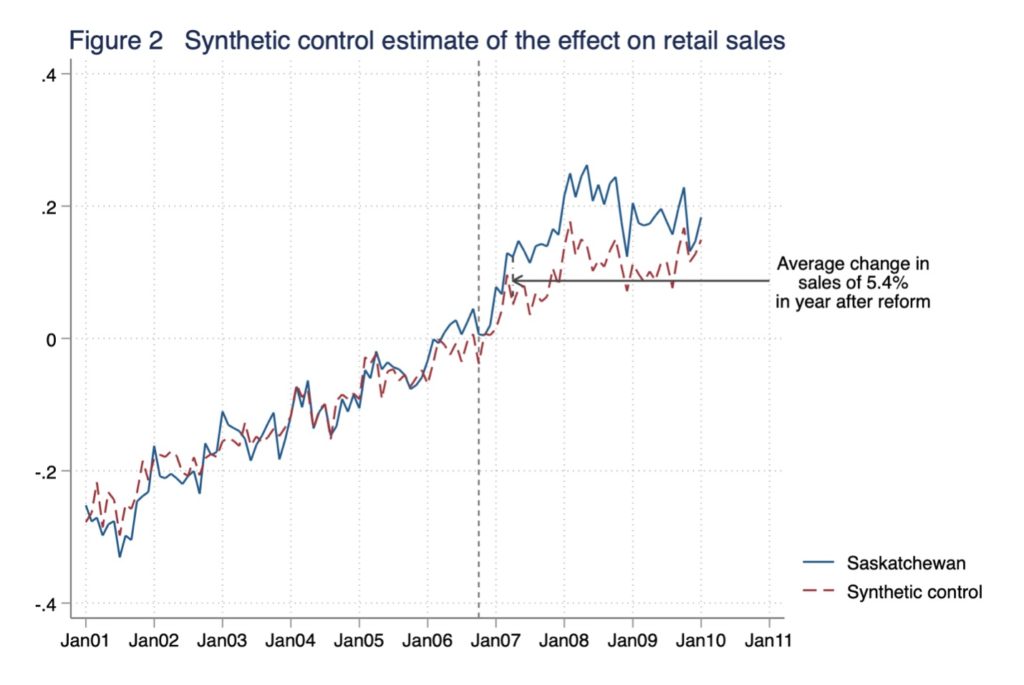

Next, I examine how the PST cut affected consumer behaviour. Figure 2 depicts the logarithm of monthly per capita retail sales in Saskatchewan, again relative to the synthetic control average of other provinces.[6]

The retail series are volatile, but the two series follow each other closely up to March 2006, when the PST cut was announced, and retail sales in Saskatchewan began to rise. On average, sales were 5.4 per cent higher in Saskatchewan than the synthetic control group in the year after the reform.

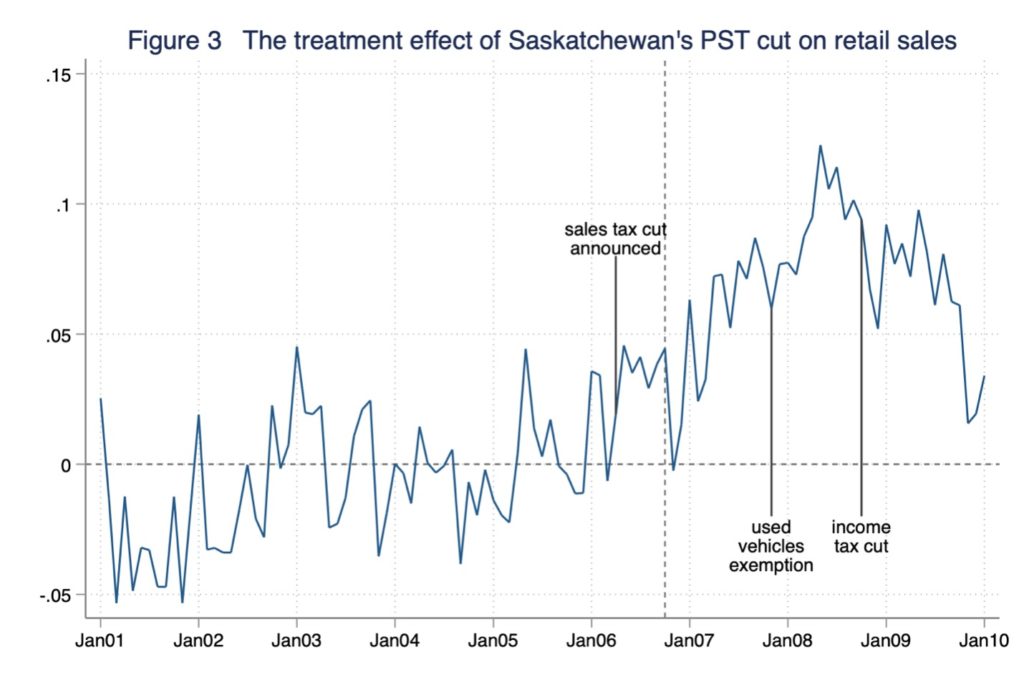

The estimated effect is large, and the estimation method I employ may not control adequately for other economic factors at play in Saskatchewan in the aftermath of the tax cut. The provincial economy boomed in the post-reform period, and these broader economic changes likely began to exert an independent effect on sales soon after the tax cut. Indeed, the provincial government subsequently implemented other tax changes that likely affected consumer spending. In particular, in November 2007, sales tax was removed from sales of used motor vehicles. In 2008, the province instituted a large increase in income tax exemptions and credits that increased after-tax incomes substantially.

Figure 3 depicts the difference between the logarithm of per capita sales in Saskatchewan and the control group over time, noting the major policy changes over this time. This difference represents the estimated “treatment effect” of the reform: the amount by which sales increased due to the tax cut. Note that sales began to increase relative to the control immediately after the announcement in the 2006 provincial budget, rising to 4.4 log points in October and continuing to rise through 2007-08.

The estimated effect beginning in March might reflect anticipation of the reform, if retailers lowered prices in advance of the tax cut (although such price reductions are not visible in the data reported in Figure 1). Certainly, the increase in Saskatchewan sales in late 2007 and 2008 is far too large to be plausibly attributed to the PST cut, and likely reflects other economic factors and policy changes in the province. Nevertheless, the rise in retail sales in the immediate wake of the PST cut announcement is striking.

The Saskatchewan case study is suggestive. Retailers did pass through the sales tax cut to consumers, and consumer purchasers did rise with the tax cut. A reduction in the federal GST rate this year is likely to have similar effects on consumer prices, and it could induce a similar boost to consumer expenditure to help spur the economic recovery.

[1] For example, Benzarti and Carloni (2019) find that a sales tax cut in France led to higher business margins rather than lower consumer prices. Benzarti et al. (2020) find that sales tax cuts in Finland have a smaller impact on prices than sales tax increases. But these findings are relevant to European countries, where consumer prices are almost invariably quoted inclusive of sales taxes. In Canada, quoted prices are usually tax-exclusive, making sales tax rates highly salient to consumers, and producer prices less likely to rise when tax rates fall.

[2] Crossley, Low, and Sleeman (2014) examine the 2.5 percentage point reduction implemented in the UK in 2008 and find substantial effects on consumer prices and retail sales.

[3] I thank my students Armun Ghafari, Sara Koruthu, and Chelsea Mitchell for suggesting the focus on Saskatchewan.

[4] I use consumer price data by commodity month, and province from Statistics Canada Table 18-10-0004, and I estimate provincial sales tax rates using data in Table 36-10-0432. I code a commodity group as taxable if at least 80% of expenditure in the category is subject to tax. For Saskatchewan in 2007 this included Household equipment, furniture and textiles, personal care articles, Clothing and footwear, Purchase and leasing of motor vehicles and parts, Communications, and Tobacco products.

[5] The synthetic control method is surveyed in Abadie (2020). I set the pre-reform period to January 2001 through Mar 2006, when the sales tax cut was first announced. I choose the weights on control provinces to match the average value of prices of untaxed commodities and of Statistics Canada’s monthly index of provincial economic activity from Table 36-10-0633, as well as the level of taxed commodity prices in March 2002 and March 2006. The estimate puts weight on prices in Newfoundland and Labrador, Nova Scotia, and New Brunswick.

[6] I detrend the retail sales series by removing average month-to-month variation nationally. I use the same predictors as in Figure 1, plus the logarithm of monthly average earnings and monthly total employment, to capture income effects on consumer demand. The method places weight on Nova Scotia, Quebec, Ontario and Manitoba in constructing the synthetic control unit.