Tammy Schirle and Mikal Skuterud

The Canada Recovery Benefit may become an important source of support for self-employed individuals during the COVID-19 pandemic, particularly among those without employees. One important obstacle to the policy’s success is that the self-employed are a heterogeneous group that is not easily characterized, with workflows that do not fit neatly into weekly benefit periods. Efforts to develop well-targeted post-pandemic support for the self-employed require better data to understand their workflows, incomes, and behavioural responses to adjustments in policy parameters.

On September 27, Canadians who lost work due to COVID-19 and who have not yet regained employment will transition from the Canada Emergency Response Benefit (CERB) to a new suite of pandemic recovery programs. Most people who relied on CERB will move to a simplified Employment Insurance (EI) program that will provide a minimum of $400 per week, for at least 26 weeks.

Those not eligible for EI can expect to turn to the new Canada Recovery Benefit (CRB). The CRB will offer $400 per week for up to 26 weeks with eligibility criteria similar to CERB—requiring a person to have earned at least $5,000 in 2019 or 2020. Individuals are also expected to be available and looking for work. The new CRB benefits are subject to clawbacks, with benefits being reduced by 50 cents for every dollar earned over $38,000 in 2020.

The largest group relying on the CRB will likely be self-employed workers (who may not be eligible for EI), especially self-employed Canadians with no employees. (Small business owners with paid help are likely to benefit more from other programs.)

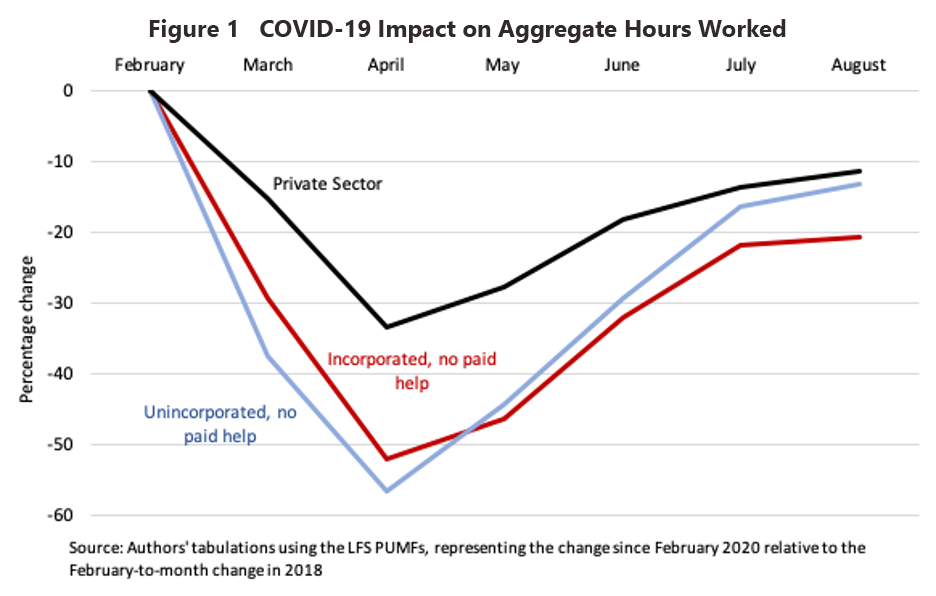

Data from the Labour Force Survey (LFS) make clear that individuals who reported their main job—that is, the job in which they worked the most hours during the survey reference week—as self-employment without paid help (representing 11% of the Canadian workforce in February 2020) were hit harder by the initial shutdowns in March than were paid employees in either the private or public sector, or the self-employed with paid help. As shown in figure 1, between February and April 2020, aggregate hours worked fell by 57% among self-employed individuals who were unincorporated, and 52% among the incorporated. In comparison, aggregate hours worked by paid employees in the private sector fell by 33% and by 17% in the public sector.

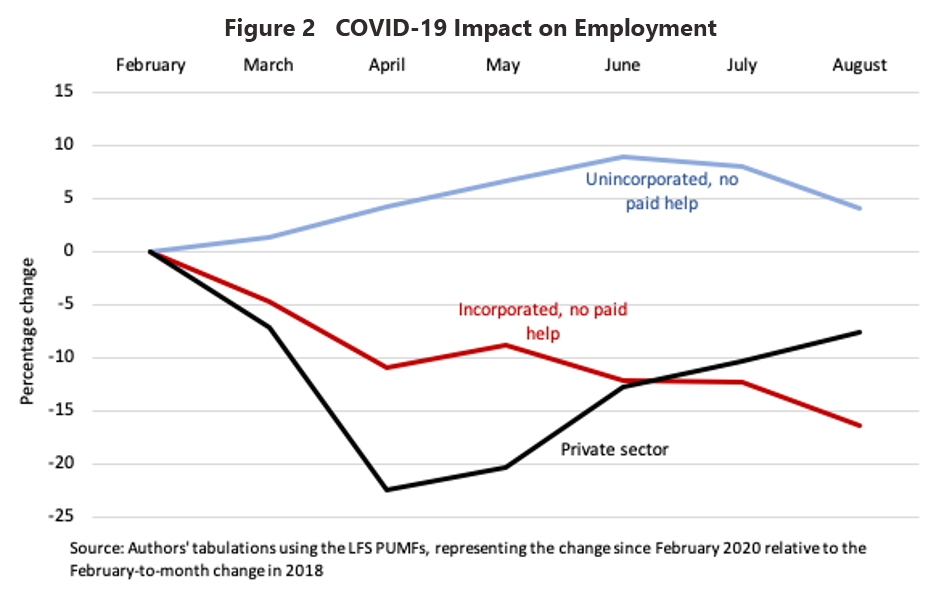

But the starkest difference between paid employees and the self-employed is the rate at which individuals lost employment in March and April and subsequently returned to work. Employment levels in the private sector fell by 23% between February and April, while incorporated self-employed individuals (without paid help) saw employment fall by only 11%. (Despite having few hours of work available, self-employed individuals were more likely than paid employees in the private sector to remain employed in April.) However, while paid employees saw significant recovery in employment levels during the summer months, the employment of incorporated self-employed workers has continued to fall. Unincorporated self-employment, on the other hand, has seen a modest overall increase in employment since February, which appears to reflect the combination of a large push out of jobs during the initial COVID-19 shutdowns in March and April and a larger pull into self-employment as a source of survival jobs while paid employment prospects are scarce. These trends are illustrated in figure 2.

Can we say anything about what types of self-employed workers are most likely to rely on the CRB for support? We used the LFS to identify self-employed individuals (in their main jobs) who were either jobless or working less than half their usual hours in July and August. The groups most affected by COVID-19 shutdowns appear to be self-employed women and younger individuals (age 25-34), although some near-retirees (age 55-59) were also disproportionately affected. Generally speaking, self-employed workers have higher average educational attainment than workers in the private sector, but there is no clear correlation between education level and impact of COVID-19 on employment: high school and post-secondary graduates (including graduates of trade schools) appear to have been more adversely affected than university graduates and those with less than a high school degree. Sales and service occupations were also more affected, but so were self-employed workers in management occupations and in health care and social services. Overall, the data suggest that the population of self-employed individuals who are most likely to be CRB applicants is a highly heterogenous group.

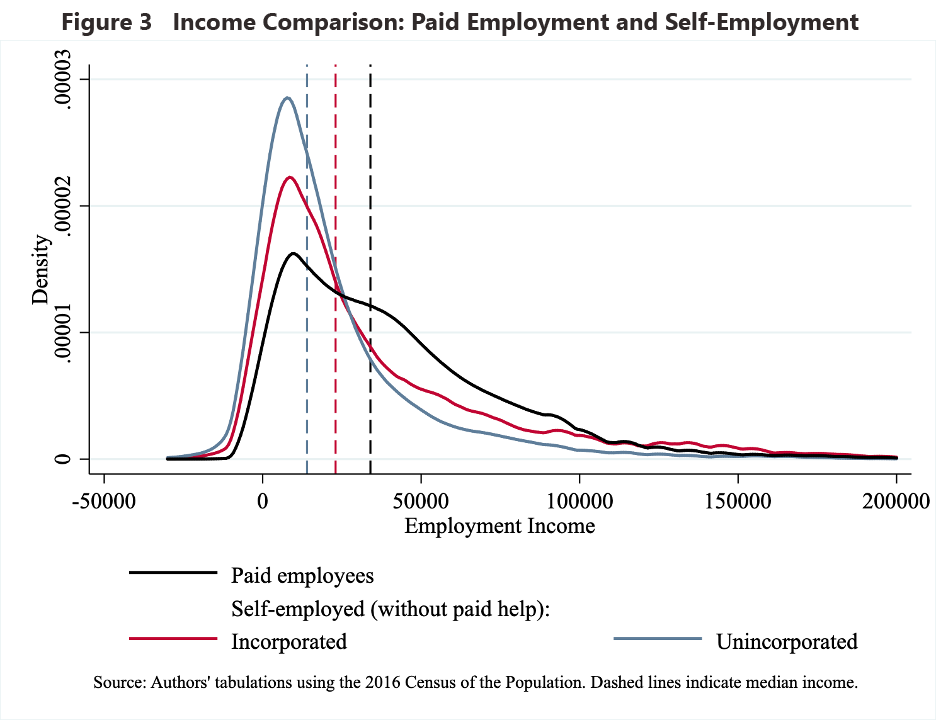

This type of heterogeneity makes it challenging to develop a one-size-fits-all policy that simultaneously meets recipients’ financial needs and encourages efforts to restore business profitability. To get a sense of the incomes potentially replaced by the CRB, we looked at a sample of self-employed individuals (without paid help) working in the service sector drawn from the 2016 Census of the Population. Relative to paid employees, whose median employment earnings in 2015 were $34,000, the incomes of self-employed individuals tend to be low. Among self-employed workers without paid help, the median annual earnings for the incorporated were $23,000 and only $14,000 for the unincorporated. See figure 3. The census data suggest that 19 percent of the unincorporated self-employed in the service sector (without paid help) would not be eligible for CRB benefits because their past earnings do not meeting the $5,000 threshold.

When we further consider the workflow of self-employed individuals, challenges in defining policy parameters arise. Unlike paid employees, for whom a weekly pay period is relatively easy to define, the work hours of the self-employed, the timing of their invoices, and the payment of those invoices do not easily fit within weekly benefit reporting periods. While it is sensible to use annual employment income to determine whether self-employed individuals are eligible (either for the lower $5,000 eligibility threshold or for the upper $38,000 clawback threshold), ensuring that support payments are reaching those with the greatest need (and not those with the best tax accountants) will present implementation challenges.

Looking ahead, there appears to be a broad desire to improve the EI system to better cover self-employed workers, especially those who hold multiple jobs to supplement their self-employment income. While the data are far from ideal, they do illuminate clear economic vulnerabilities within this population. However, the data do not reveal the extent to which this diverse group holds discretion over their hours of work, including through shifting time between multiple jobs, which in some cases include part-time jobs in paid employment. In addition, standard income reference periods used to capture the earnings of paid employees are problematic in capturing the variable incomes of self-employed workers. Better data are required before long-term policy can move forward in designing robust support programs for this segment of the Canadian workforce.