Adam Lavecchia and Alisa Tazhitdinova

The debate over whether to increase the tax rate hinges in part on the extent to which a higher tax rate would distort savings and investment decisions and reduce incentives for Canadians to invest. This commentary sheds light on this debate by analyzing the effects of a tax policy change in the mid-1990s that increased the effective capital gains tax rate. They find that the new higher rate on capital gains had no adverse effect on cumulative capital gains realizations.

Recently, there have been a number of calls to change the way capital gains income is taxed in Canada. Proponents argue that higher taxes on capital gains will reverse rising income and wealth inequality, and raise substantial tax revenue for the federal and provincial governments. Opponents counter that capital gains taxes are inefficient because they reduce incentives for Canadians to save and invest, and they distort investment portfolio decisions. Ultimately, which side is correct depends on the responsiveness of tax filers to capital gains tax rate changes. Unfortunately, there is relatively little Canadian evidence surrounding the real-world impacts of increasing capital gains taxes.[1]

In this commentary, we discuss the findings from our new research on the estimated impact of the 1994 reform that dramatically increased the tax rate on capital gains income for most Canadians. In February 1994, the then-Liberal government of Prime Minister Jean Chrétien and Minister of Finance Paul Martin cancelled the $100,000 lifetime capital gains exemption[2] (hereafter, the LCGE), as part of an effort to reduce a spiraling federal budget deficit.

We find that over a five-year period, the removal of the LCGE had no cumulative adverse effect on capital gains realizations. The policy implications are that a capital gains tax rate increase should be expected to raise significant revenue over time and create minimal economic distortion with respect to individuals’ lifetime level of capital gains realizations.

Initially introduced in 1985 by the previous Conservative government of Brian Mulroney, the LCGE allowed tax filers to receive up to $100,000 in capital gains income tax-free. The LCGE thus mimicked the qualified farm and small business lifetime exemptions that remain in effect to this day ($883,384 in 2020), but was applicable to other sources of gains. The LCGE has not been reinstated.

The cancellation of the LCGE represented a large increase to the effective marginal tax rate on capital gains income for most Canadians. To illustrate the magnitude of this reform, consider the impact of the cancellation for tax filers with $40,000 in taxable income in 1994 who had not used any of their $100,000 LCGE space in previous years.[3] For these tax filers, this reform increased the federal effective marginal tax rate on realized capital gains income from zero to 19.5 per cent.[4] Further, the removal of the exemption would have increased their lifetime federal tax liability by up to $19,500.[5] Tax filers with the same income who used $50,000 of their LCGE space prior to the reform would have seen their lifetime federal tax liability increase by up to $9,750. Adding provincial surtaxes to these amounts meant that the total (federal plus provincial) lifetime tax liability increase was even higher. In contrast, tax filers who exhausted their $100,000 LCGE space by 1994 were not impacted by the cancellation.

As part of the cancellation of the LCGE in the 1994 budget, the federal government allowed tax filers to take advantage of remaining exemption space through a one-time adjustment. In particular, individuals with unused exemption space were able to crystalize unrealized capital gains when preparing their 1994 tax return. Specifically, individuals could crystalize their capital gains by increasing the cost base of their assets up to their unused LCGE space in February 1994. Provided that tax filers were aware of this provision, this represented an essentially costless way to bring forward capital gains income to 1994.

The 1994 change provides a unique opportunity to understand how Canadian tax filers respond to capital gains taxes. The cancellation of the LCGE stands out both in terms of its magnitude and permanence. The large tax increase created by the LCGE cancellation should have incentivized affected Canadians to think long and hard about their capital gains decisions. In turn, these decisions allow us to learn about long-term consequences of capital gains tax increases.

Our study estimates both the immediate and long-term impact of the cancellation of the LCGE on capital gains realizations in the six years following the removal of the LCGE. To do so, we compare the evolution of the realized capital gains of tax filers whose effective marginal tax rates increased because of the cancellation to the capital gains of a comparison group, i.e. tax filers who had exhausted their $100,000 exemption space by 1994. In other words, we compare the behaviour of individuals who faced a significant increase in their effective capital gains tax rate starting in 1994 to similar individuals who experienced no increase at all.

Our approach is similar in spirit to the clinical trials used by pharmaceutical companies that compare the health outcomes of individuals who receive a new treatment or vaccine to a “control” group whose members do not. In pharmaceutical trials, the control or placebo group provides researchers with a credible estimate of the changes in health which naturally occur over time that are unrelated to the receipt of the new treatment. Importantly, we are able to verify that tax filers in our comparison group are similar in age, income and other demographic characteristics to tax filers in the affected groups.[6] For example, the annual incomes of both groups evolve similarly over 1990-99, the period around the cancellation of the LCGE on which we focus. This is reassuring because it decreases the likelihood that any observed differences between the realized capital gains of the affected and unaffected groups are due to anything other than the change in tax rates that the affected group faced.

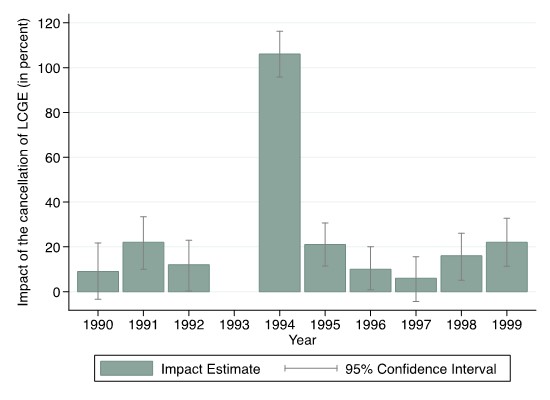

Figure 1 displays the main results of our study. Each bar in the figure represents the percentage difference in the realized capital gains between tax filers in one of our affected groups and the comparison group. The annual percentage changes are benchmarked against the 1993 difference, whose bar is zero (by construction). Importantly, our estimates control for differences in individual characteristics that might affect capital gains realizations such as age, marital status and postal code/location .[7]

Figure 1 reveals two main results. The first is that the average realized capital gains of tax filers affected by the cancellation of the LCGE increased by approximately 105 per cent from 1993 to 1994, compared to the control group. This suggests that tax filers in the affected group took advantage of the one-time opportunity to crystalize their capital gains in 1994. This isn’t surprising, given that tax filers did not have to sell their assets to crystalize their unrealized gains. By crystalizing unrealized capital gains up to their remaining LCGE space, tax filers in the affected groups were able to save thousands of dollars in future capital gains income taxes.

Figure 1 How Do Capital Gains Change after LCGE Cancellation?

Our second and most important main result is that the cancellation of the LCGE did not lead to lower capital gains realizations in the five-year period after 1994. This is seen in Figure 1 where none of the bars from 1995-99 are below zero. Compared to unaffected tax filers, Figure 1 shows that the realized capital gains of individuals in the affected group increased by between five per cent and 25 per cent from 1995-99 (relative to the 1993 baseline). Figure 1 also shows how the realized capital gains of the affected group evolved, compared to the control group, in the years leading up to 1994. The lack of any obvious time trend in the bars for 1990-92 suggests that our findings are not driven by pre-reform differences between the affected group and the comparison group. Put simply, our results suggest that the higher effective marginal tax rates after 1994 did not have an adverse effect on capital gains realizations over the subsequent five-year period.

While possibly surprising at first blush, our finding that the higher effective tax rates on capital income did not lower realizations has a firm grounding in economic theory. Like any other tax, the unexpected cancellation of the LCGE created two offsetting economic forces. On the one hand, increasing the effective marginal tax rate on capital gains income reduced the incentive to realize capital gains. On the other hand, the cancellation of the LCGE reduced the expected lifetime wealth of tax filers by increasing their future tax liabilities, encouraging them to save more. To see why this is the case, consider a tax filer with $40,000 in taxable income who reported $30,000 in realized capital gains in the years leading up to the cancellation of the LCGE. Suppose also that this tax filer expected to eventually use $80,000 in LCGE space. The cancellation of the LCGE reduced the expected lifetime wealth of this tax filer by at least 0.195 x ($80,000 – $30,000) = $9,750. All else equal, this decrease in lifetime wealth would have motivated savers to increase their asset accumulation over time, and therefore capital gains income, to offset the decline in future purchasing power.

There are a number of lessons that current policy-makers can take from this historical episode as future reforms to capital gains taxes are considered. One lesson is that short-run evaluations to changes in tax policy may dramatically overstate the costs to future capital gains tax increases. On its own, the spike we observe for the affected groups in 1994 suggests that capital gains realizations are very responsive to changes in tax rates. If such immediate response is representative of the long-run response we might observe today, then any capital gains tax increases would yield little revenue and would have adverse impacts on economic efficiency. However, our results show that even large short-run responses to capital gains tax increases might not be representative – and even be of opposite direction – from any long-run responses. Since the policy decisions should be based on long-run responses, our results caution against over-inferring from small and short-lived tax changes.

A related lesson is that the real economic responses to capital gains taxes, such as reductions in savings and risk-taking on the part of individual tax filers, are likely to be substantially smaller than responses due to the re-timing of capital gains or tax avoidance. The fact that capital gains realizations did not decline after 1995 suggests that capital gains income is not very responsive to permanent changes in tax rates, and that raising capital gains taxes is likely to result in large tax revenue gains over time.

[1] While evidence from the United States (e.g. Agersnap and Zidar (2020)) and other countries is helpful, evidence from Canada is more informative to policy debates in this country because of differences between the way Canada and other countries tax capital gains and other types of investment income.

[2] Realized capital gains from the sale of primary residences have always been exempt from taxation in Canada.

[3] The 1994 average income of a typical tax filer affected by the cancellation of the LCGE was $40,000. Adjusting for inflation, $40,000 in taxable income in 1994 is equivalent to $63,685 in 2020.

[4] The effective marginal tax rate of 19.5 per cent incorporates the inclusion rate of 75 per cent on realized capital gains income that was in place from 1990 until 1999.

[5] The $19,500 lifetime tax liability increase assumes that tax filers expected to eventually receive $100,000 or more in capital gains income. For tax filers who expected to receive less than $100,000 in capital gains, the lifetime federal tax liability increase was lower. More generally, if tax filers had not used any of their LCGE space by 1994 but expected to eventually receive capital gains income of $CG, the cancellation of the LCGE increased their federal lifetime tax liability by 0.195 x $CG.

[6] See Online Appendix Figure E.1 in our paper. Note that the affected and comparison groups in our study are defined based on realized capital gains reported from 1985-1993, the years in which the LCGE was in place. We show that collectively, our affected and comparison groups account for at least one-quarter of capital gains income reported in Canada during the 1990-99 period.

[7] The estimates presented in Figure 1 are for tax filers who claimed between $33,000 and $67,000 of their LCGE space by 1993. In our study, we consider various groups of individuals, but our key findings are similar across groups.